Question

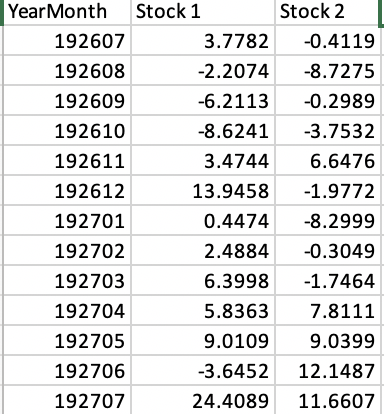

How do you do these problems IN EXCEL given the sample data below? 1. Next you are going to consider a portfolio consisting of a

How do you do these problems IN EXCEL given the sample data below?

1. Next you are going to consider a portfolio consisting of a fraction w1 in stock 1 and w2 = 1-w1 in stock2

Use the results above to calculate the average return and standard deviation of the portfolio when varying w1 between 0 and 4. What is the minimum variance portfolio?

Consider a risk-free rate of 1% and assume that you can invest/borrow at the same rate.

2. Draw the efficient frontier when you can invest/borrow in the risk-free rate in addition to the two stocks above.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

For Investing And Earning In The Digital Currency Market Simple Bitcoin

Authors: Marco Cavicchi ,Easy E-Book

1st Edition

979-8395459732