Answered step by step

Verified Expert Solution

Question

1 Approved Answer

how to do in excel for Approximate modified duration and approximate duration c . On your sheet labelled 'Part c ' do the following. Consider

how to do in excel for Approximate modified duration and approximate duration

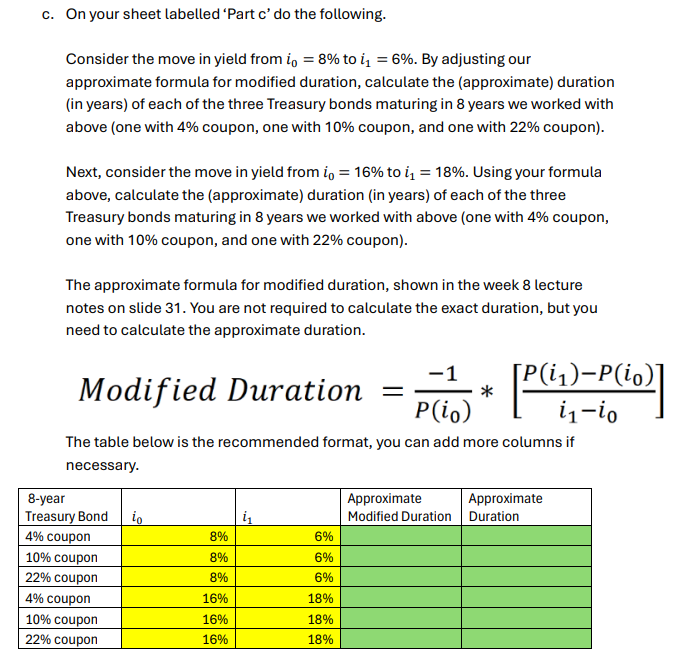

c On your sheet labelled 'Part c do the following.

Consider the move in yield from to By adjusting our

approximate formula for modified duration, calculate the approximate duration

in years of each of the three Treasury bonds maturing in years we worked with

above one with coupon, one with coupon, and one with coupon

Next, consider the move in yield from to Using your formula

above, calculate the approximate duration in years of each of the three

Treasury bonds maturing in years we worked with above one with coupon,

one with coupon, and one with coupon

The approximate formula for modified duration, shown in the week lecture

notes on slide You are not required to calculate the exact duration, but you

need to calculate the approximate duration.

Modified Duration

The table below is the recommended format, you can add more columns if

necessary.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

Concise 6th Edition

324664559, 978-0324664553