Answered step by step

Verified Expert Solution

Question

1 Approved Answer

How to solve these Question No. 1 a) Briefly explain difference in direct and indirect taxes and different kind of such taxes prevailing in Pakistan.

How to solve these

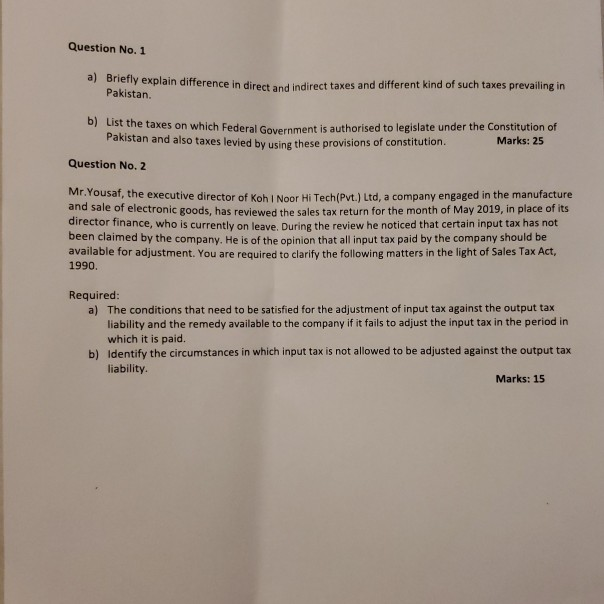

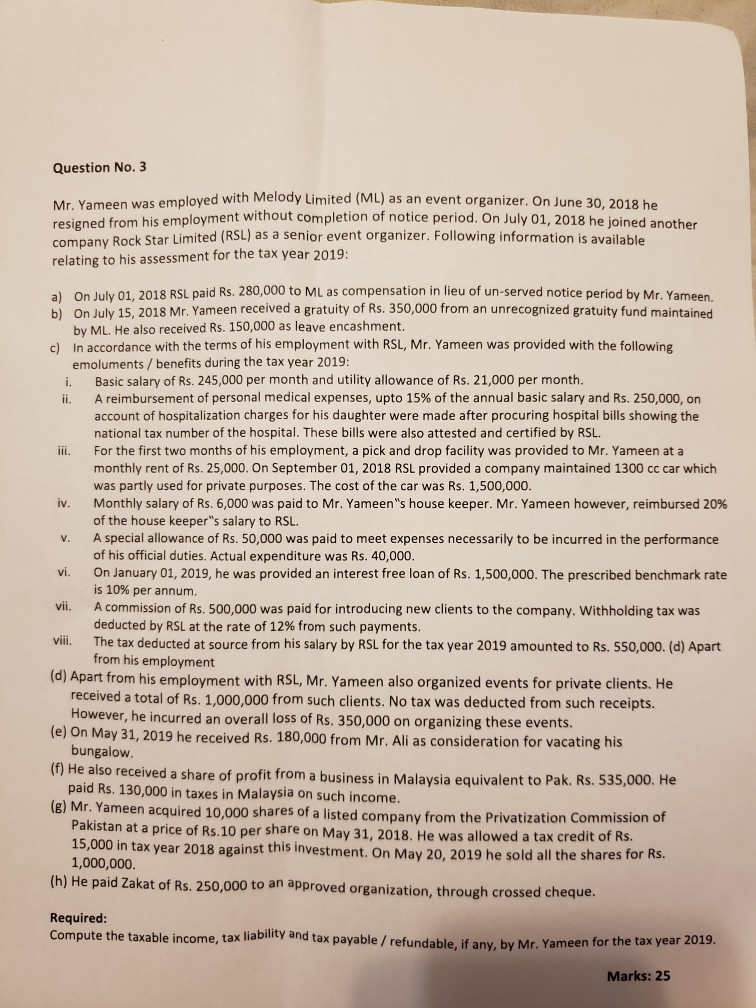

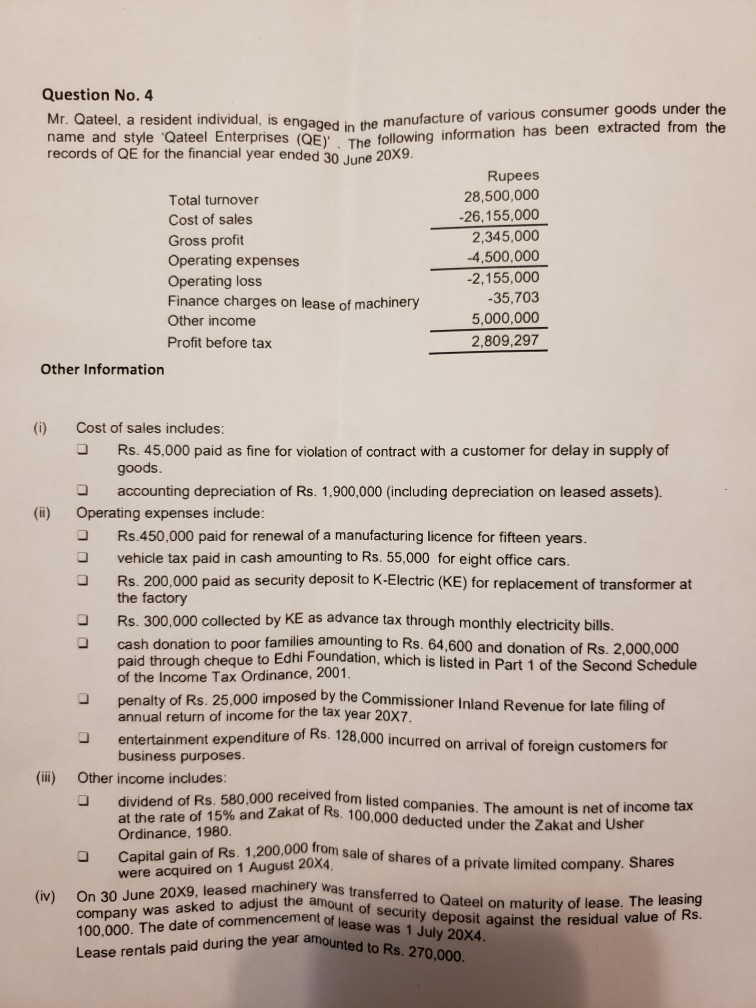

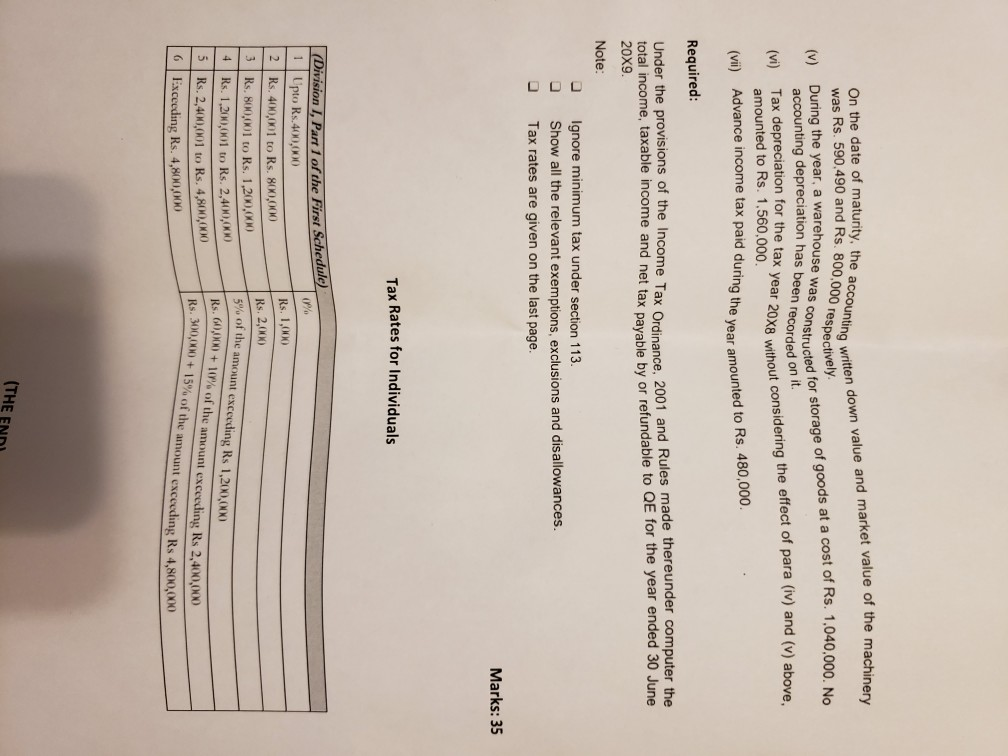

Question No. 1 a) Briefly explain difference in direct and indirect taxes and different kind of such taxes prevailing in Pakistan. b) List the taxes on which Federal Government is authorised to legislate under the Constitution of Pakistan and also taxes levied by using these provisions of consti Marks: 25 Question No. 2 Mr.Yousaf, the executive director of Koh I Noor Hi Tech(Pvt.) Ltd, a company engaged in the manufacture and sale of electronic goods, has reviewed the sales tax return for the month of May 2019, in place of its director finance, who is currently on leave. During the review he noticed that certain input tax has not been claimed by the company. He is of the opinion that all input tax paid by the company should be available for adjustment. You are required to clarify the following matters in the light of Sales Tax Act, 1990. Required The conditions that need to be satisfied for the adjustment of input tax against the output tax liability and the remedy available to the company if it fails to adjust the input tax in the period in which it is paid. Identify the circumstances in which input tax is not allowed to be adjusted against the output tax liability. a) b) Marks: 15 Question No. 3 Mr. Yameen was employed with Melody Limited (ML) as an event organizer. On June 30, 2018 he resigned from his employment without completion of notice period. On July 01, 2018 he joined another company Rock Star Limited (RSL) as a senior event organizer. Following information is available relating to his assessment for the tax year 2019 a) On July 01, 2018 RSL paid Rs. 280,000 to ML as compensation in lieu of un-served notice period by Mr. Yameen. b) On July 15, 2018 Mr. Yameen received a gratuity of Rs. 350,000 from an unrecognized gratuity fund maintained by ML. He also received Rs. 150,000 as leave encashment In accordance with the terms of his employment with RSL, Mr. Yameen was provided with the following emoluments/ benefits during the tax year 2019 i. c) Basic salary of Rs. 245,000 per month and utility allowance of Rs. 21,000 per month A reimbursement of personal medical expenses, upto 15% of the annual basic salary and Rs. 250,000, on account of hospitalization charges for his daughter were made after procuring hospital bills showing the national tax number of the hospital. These bills were also attested and certified by RSL ii. For the first two months of his employment, a pick and drop facility was provided to Mr. Yameen at a monthly rent of Rs. 25,000. On September 01, 2018 RSL provided a company maintained 1300 cc car which was partly used for private purposes. The cost of the car was Rs. 1,500,000 Monthly salary of Rs. 6,000 was paid to Mr. Yameen"s house keeper. Mr. Yameen however, reimbursed 20% of the house keeper"s salary to RSL. iv. V. A special allowance of Rs. 50,000 was paid to meet expenses necessarily to be incurred in the performance of his official duties. Actual expenditure was Rs. 40,000 On January 01, 2019, he was provided an interest free loan of Rs. 1,500,000. The prescribed benchmark rate is 10% per annum vii. A commission of Rs. 500,000 was paid for introducing new clients to the company. Withholding tax was vii. The tax deducted at source from his salary by RSL for the tax year 2019 amounted to Rs. 550,000. (d) Apart (d) Apart from his employment with RSL, Mr. Yameen also organized events for private clients. He deducted by RSL at the rate of 12% from such payments from his employment (e) On May 31, 2019 he received Rs. 180,000 from Mr. Ali as consideration for vacating his (f) H (e) Mr. Yameen acquired 10,000 s received a total of Rs. 1,000,000 from such clients. No tax was deducted from such receipts. However, he incurred an overall loss of Rs. 350,000 on organizing these events bungalow e also received a share of profit from a business in Malaysia equivalent to Pak. Rs. 535,000. He paid Rs. 130,000 in taxes in Malaysia on such income hares of a listed company from the Privatization Commission of stan at a price of Rs.10 per share on May 31, 2018. He was allowed a tax credit of Rs. 15,000 in tax year 2018 against this invest 1,000,000. ment. On May 20, 2019 he sold all the shares for Rs (h) He paid Zakat of Rs. 250,000 to an approved organization, through crossed cheque Required Compute the taxable income, tax liability and tax payable / refundable, if any, by Mr. Yameen for the tax year 2019 Marks: 25 Question No. 4 is engaged in the manufacture of various consumer goods under the name and style Oateel Enterprises (QE The following information has been records of QE for the financial year ended 30 June 20X9. Total turnover Cost of sales Gross profit Operating expenses Operating loss Finance charges on lease of machinery Other income Profit before tax Rupees 28,500,000 26,155,000 2,345,000 -4,500,000 2,155,000 35,703 5,000,000 2,809,297 Other Information (i) Cost of sales includes Rs. 45.000 paid as fine for violation of contract with a customer for delay in supply of goods accounting depreciation of Rs. 1,900,000 (including depreciation on leased assets). (i) Operating expenses include: O Rs.450,000 paid for renewal of a manufacturing licence for fifteen years. O vehicle tax paid in cash amounting to Rs. 55,000 for eight office cars. O Rs. 200,000 paid as security deposit to K-Electric (KE) for replacement of transformer at the factory Rs. 300,000 collected by KE as advance tax through monthly electricity bills. O cash donation to poor families amounting to Rs. 64,600 and donation of Rs. 2,000,000 paid through cheque to Edhi Foundatio of the Income Tax Ordinance, 2001 n, which is listed in Part 1 of the Second Schedule 25,000 imposed by the Commissioner Inland Revenue for late filing of enditure of Rs. 128,000 incurred on arrival of foreign customers for annual return of income for the tax business purposes. dividend of Rs. 580,000 received from li year 20X7 (i) Other income includes: sted companies. The amount is net of income tax at the rate of 15% and Zakat o Rs 100,000 deducted under the Zakat and Usher Ordinance, 1980. ,0 trom sale of shares of a private limited company, Shares share were acquired on 1 August 20X4, machinery was transferred to Qateel on maturity of le ust the amount of security deposit against the res was 1 July 20X4. te (iv) On 30 June 20X9, leased company was asked to adjust the 100,000. The date of commencement of lea lease. The leasing Lease rentals paid during the year amounted Io machinery . No ax year 20x8 without considering the effect of para (iv) and (v) above, On the date of maturity, the accounting written d down value and market value of the m was Rs. 590.490 and Rs. 800,000 accounting depreciation has been recorded on it amounted to Rs. 1,560,000 respectively (v) During preciation has bwas constructed for storage of goods at a cost of Rs. 1,040,000 nce income tax paid during the year amoun Required Under the provisions of the Income Tax Ordinance, 2001 and Rules made total income, taxable income a 20x9 thereunder computer the fundable to QE for the year ended 30 June nd net tax payable by or re Note Ignore minimum tax under section 113. show all the relevant exemptions, exclusions and disallowances. Tax rates are given on the last page. Marks: 35 Tax Rates for Individuals Part 1 of the First Schedule 0%, Rs. 1,000 Rs. 2,000 5% of the amount exceeding Rs 1,2X,000 Rs. 60-xx, + 10% of the amount exceding Rs 2,400,000 Upto Rs.400,000 2 Rs. 400,001 to Rs. 800,000 Rs. 800,001 to Rs. 1,200,000 4 Rs. 1,200,001 to Rs. 2,400,000 5 Rs. 2,400,001 to Rs. 6 Exceeding Rs. 4,800,000 4.800,(X)() --TRs. 30(,(xx) + 1 5% of the amount exceding Rs 4,80,(00 THE END Question No. 1 a) Briefly explain difference in direct and indirect taxes and different kind of such taxes prevailing in Pakistan. b) List the taxes on which Federal Government is authorised to legislate under the Constitution of Pakistan and also taxes levied by using these provisions of consti Marks: 25 Question No. 2 Mr.Yousaf, the executive director of Koh I Noor Hi Tech(Pvt.) Ltd, a company engaged in the manufacture and sale of electronic goods, has reviewed the sales tax return for the month of May 2019, in place of its director finance, who is currently on leave. During the review he noticed that certain input tax has not been claimed by the company. He is of the opinion that all input tax paid by the company should be available for adjustment. You are required to clarify the following matters in the light of Sales Tax Act, 1990. Required The conditions that need to be satisfied for the adjustment of input tax against the output tax liability and the remedy available to the company if it fails to adjust the input tax in the period in which it is paid. Identify the circumstances in which input tax is not allowed to be adjusted against the output tax liability. a) b) Marks: 15 Question No. 3 Mr. Yameen was employed with Melody Limited (ML) as an event organizer. On June 30, 2018 he resigned from his employment without completion of notice period. On July 01, 2018 he joined another company Rock Star Limited (RSL) as a senior event organizer. Following information is available relating to his assessment for the tax year 2019 a) On July 01, 2018 RSL paid Rs. 280,000 to ML as compensation in lieu of un-served notice period by Mr. Yameen. b) On July 15, 2018 Mr. Yameen received a gratuity of Rs. 350,000 from an unrecognized gratuity fund maintained by ML. He also received Rs. 150,000 as leave encashment In accordance with the terms of his employment with RSL, Mr. Yameen was provided with the following emoluments/ benefits during the tax year 2019 i. c) Basic salary of Rs. 245,000 per month and utility allowance of Rs. 21,000 per month A reimbursement of personal medical expenses, upto 15% of the annual basic salary and Rs. 250,000, on account of hospitalization charges for his daughter were made after procuring hospital bills showing the national tax number of the hospital. These bills were also attested and certified by RSL ii. For the first two months of his employment, a pick and drop facility was provided to Mr. Yameen at a monthly rent of Rs. 25,000. On September 01, 2018 RSL provided a company maintained 1300 cc car which was partly used for private purposes. The cost of the car was Rs. 1,500,000 Monthly salary of Rs. 6,000 was paid to Mr. Yameen"s house keeper. Mr. Yameen however, reimbursed 20% of the house keeper"s salary to RSL. iv. V. A special allowance of Rs. 50,000 was paid to meet expenses necessarily to be incurred in the performance of his official duties. Actual expenditure was Rs. 40,000 On January 01, 2019, he was provided an interest free loan of Rs. 1,500,000. The prescribed benchmark rate is 10% per annum vii. A commission of Rs. 500,000 was paid for introducing new clients to the company. Withholding tax was vii. The tax deducted at source from his salary by RSL for the tax year 2019 amounted to Rs. 550,000. (d) Apart (d) Apart from his employment with RSL, Mr. Yameen also organized events for private clients. He deducted by RSL at the rate of 12% from such payments from his employment (e) On May 31, 2019 he received Rs. 180,000 from Mr. Ali as consideration for vacating his (f) H (e) Mr. Yameen acquired 10,000 s received a total of Rs. 1,000,000 from such clients. No tax was deducted from such receipts. However, he incurred an overall loss of Rs. 350,000 on organizing these events bungalow e also received a share of profit from a business in Malaysia equivalent to Pak. Rs. 535,000. He paid Rs. 130,000 in taxes in Malaysia on such income hares of a listed company from the Privatization Commission of stan at a price of Rs.10 per share on May 31, 2018. He was allowed a tax credit of Rs. 15,000 in tax year 2018 against this invest 1,000,000. ment. On May 20, 2019 he sold all the shares for Rs (h) He paid Zakat of Rs. 250,000 to an approved organization, through crossed cheque Required Compute the taxable income, tax liability and tax payable / refundable, if any, by Mr. Yameen for the tax year 2019 Marks: 25 Question No. 4 is engaged in the manufacture of various consumer goods under the name and style Oateel Enterprises (QE The following information has been records of QE for the financial year ended 30 June 20X9. Total turnover Cost of sales Gross profit Operating expenses Operating loss Finance charges on lease of machinery Other income Profit before tax Rupees 28,500,000 26,155,000 2,345,000 -4,500,000 2,155,000 35,703 5,000,000 2,809,297 Other Information (i) Cost of sales includes Rs. 45.000 paid as fine for violation of contract with a customer for delay in supply of goods accounting depreciation of Rs. 1,900,000 (including depreciation on leased assets). (i) Operating expenses include: O Rs.450,000 paid for renewal of a manufacturing licence for fifteen years. O vehicle tax paid in cash amounting to Rs. 55,000 for eight office cars. O Rs. 200,000 paid as security deposit to K-Electric (KE) for replacement of transformer at the factory Rs. 300,000 collected by KE as advance tax through monthly electricity bills. O cash donation to poor families amounting to Rs. 64,600 and donation of Rs. 2,000,000 paid through cheque to Edhi Foundatio of the Income Tax Ordinance, 2001 n, which is listed in Part 1 of the Second Schedule 25,000 imposed by the Commissioner Inland Revenue for late filing of enditure of Rs. 128,000 incurred on arrival of foreign customers for annual return of income for the tax business purposes. dividend of Rs. 580,000 received from li year 20X7 (i) Other income includes: sted companies. The amount is net of income tax at the rate of 15% and Zakat o Rs 100,000 deducted under the Zakat and Usher Ordinance, 1980. ,0 trom sale of shares of a private limited company, Shares share were acquired on 1 August 20X4, machinery was transferred to Qateel on maturity of le ust the amount of security deposit against the res was 1 July 20X4. te (iv) On 30 June 20X9, leased company was asked to adjust the 100,000. The date of commencement of lea lease. The leasing Lease rentals paid during the year amounted Io machinery . No ax year 20x8 without considering the effect of para (iv) and (v) above, On the date of maturity, the accounting written d down value and market value of the m was Rs. 590.490 and Rs. 800,000 accounting depreciation has been recorded on it amounted to Rs. 1,560,000 respectively (v) During preciation has bwas constructed for storage of goods at a cost of Rs. 1,040,000 nce income tax paid during the year amoun Required Under the provisions of the Income Tax Ordinance, 2001 and Rules made total income, taxable income a 20x9 thereunder computer the fundable to QE for the year ended 30 June nd net tax payable by or re Note Ignore minimum tax under section 113. show all the relevant exemptions, exclusions and disallowances. Tax rates are given on the last page. Marks: 35 Tax Rates for Individuals Part 1 of the First Schedule 0%, Rs. 1,000 Rs. 2,000 5% of the amount exceeding Rs 1,2X,000 Rs. 60-xx, + 10% of the amount exceding Rs 2,400,000 Upto Rs.400,000 2 Rs. 400,001 to Rs. 800,000 Rs. 800,001 to Rs. 1,200,000 4 Rs. 1,200,001 to Rs. 2,400,000 5 Rs. 2,400,001 to Rs. 6 Exceeding Rs. 4,800,000 4.800,(X)() --TRs. 30(,(xx) + 1 5% of the amount exceding Rs 4,80,(00 THE END

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Information Systems

Authors: Steven M. Bragg

2nd Edition

164221079X, 9781642210798