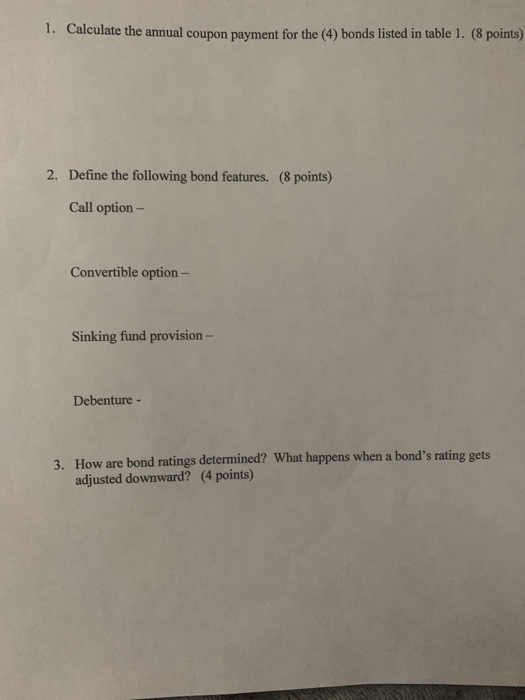

HW 10 Bond Analysis and Valuation Corporate Bonds-They Are More Complex Than You Think Jill Dougherty was hired as an investment analyst by A.M. Smith Inc. for the Cincinnati, Ohio office based on her sound academic credentials, which included an MBA from a top ranking university and a CFA designation. At the time of her recruitment she was told that one of her responsibilities would be to conduct educational seminars for current and prospective clients. A.M. Smith Inc., a prestigious investment services firm, with branches in 30 major metropolitan areas, had achieved most of its success due to its excellent client relations and focus on client support. The firm ranked among the very best in terms of the number of successful equity underwriting deals undertaken. Recently, a large utility company had hired it as the leading investment banker for a major corporate bond issue. Since most of its retail customers were more familiar with stock investments, John Sullivan, the branch manager at the Cincinnati office, Case 10 Corporate Bonds-They are More Complex Than You Think asked Jill to prepare and present a seminar outlining the various implications of fixed income investments. "About 60 % of our investors are in the 55+ age group, Jill, so we should not have much trouble convincing them of the benefits of investing in bonds" remarked John. "However, they may need clarifications regarding various terms and concepts associated with fixed income investing. Your job is to convince them of the relative safety and income potential of corporate bonds" said John. In preparation for the seminar, Jill called up a few of her best clients and queried them regarding their awareness of the risk and return potential associated with corporate bond investments. She realized that apart from a good knowledge about the current level and stability of interest rates and inflation, most customers were not very familiar about the finer aspects of bond investing. Bond features like callability, convertibility, sinking fund provision, bond ratings, debentures, interest rate risk, etc. were not well understood by most of the clients she interviewed. Most of them seemed awfully interested in knowing more about the opportunities offered by bond investing and Jill knew that she would have a good turnout at the seminar. She decided to refer back to her Finance textbook and dig out some definitions and examples that she could use in her PowerPoint presentation. She downloaded curent data for outstanding bonds of various maturities, ratings, and coupon rates (see Table 1) and started preparing her slides. Table 1 Corporate Bond Information Quoted Years until Sinking Call Coupon Face Value Rate Fund Period maturity Rating Price Issuer $703.1 Yes ABC Energy ABC Energy TransPower 5% AAA 3 Years $1,000 $208.3 0 % AAA 20 Yes NA $1,000 $1092.0 5 Years AA 20 Yes $1,000 10% $1206.4 30 No 5 Years 11% AA Telco Utlities $1,000 20 1. Calculate the annual coupon payment for the (4) bonds listed in table 1. (8 points) Define the following bond features. (8 points) 2. Call option - Convertible option - Sinking fund provision- Debenture - 3. How are bond ratings determined? What happens when a bond's rating gets adjusted downward? (4 points) Page 2 4. Explain why some bonds sell for a premium while others sell for discount? (4 points) 5. Calculate the current yield for the (4) bonds listed in table 1. (10 points) 6. What does the term "yield to maturity" mean? Calculate the "yield to maturity" for the (4) bonds listed in table 1 if the coupon is paid annually. (10 points) 7. Identify and describe (2) main risks associated with corporate bonds. (6 points)