I already submitted the template for this project on 4/23. please refer to that template.

Now I am posting 5 questions consecutively. those all 5 question are combined 1 project but i am posting separately so you could answer all of 5 questions at your own choice. These all 5 questions will be solved in same template which I submitted on 4/23.

My UIN's last 2 digits are 28. so please solve all these 5 questions with 28. All the extra info which is not given in these 5 questions can be collected from that same template. I am just explaining few here.

In cell E1 of template you see the market price - $99.75. That's the price for the bond we observe in the market and OAS tells us how much extra spread we are earning when taking into account that the bond is callable. You use volatility to calibrate the one-step forward rates such that they are consistent with the zero coupon bond prices given in cells B-E row 6. Time horizon is 4 years (project is 7 years).

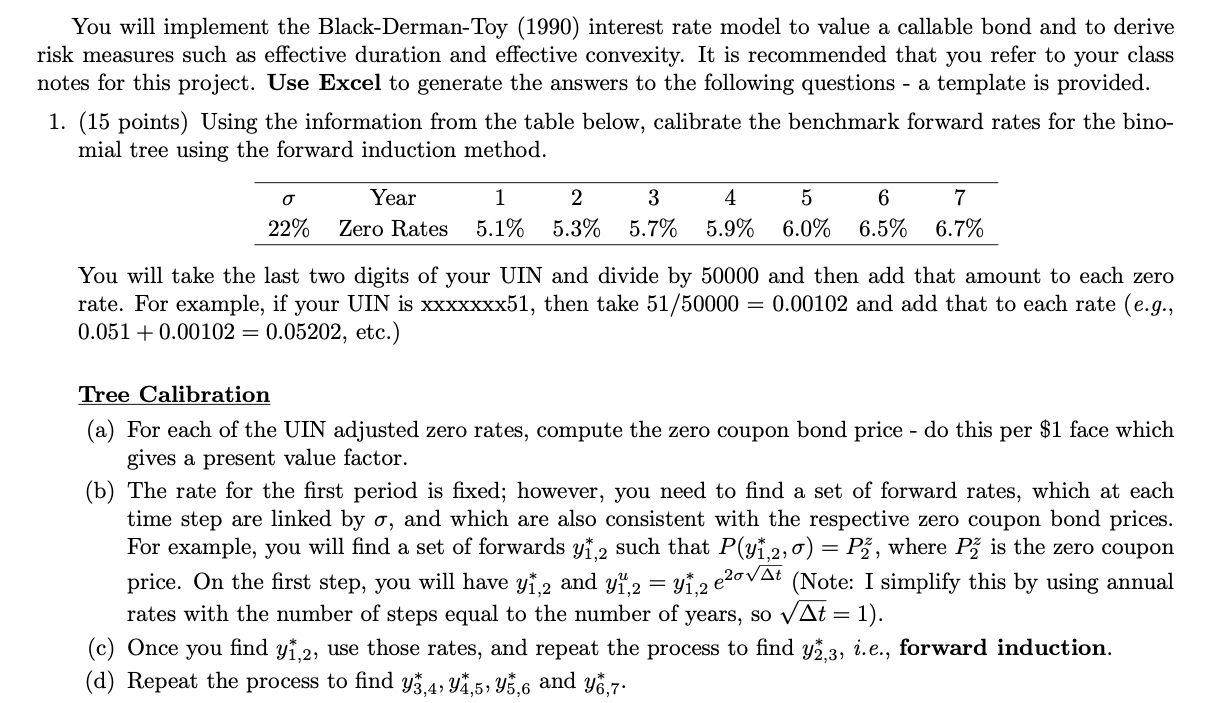

You will implement the Black-Derman-Toy (1990) interest rate model to value a callable bond and to derive risk measures such as effective duration and effective convexity. It is recommended that you refer to your class notes for this project. Use Excel to generate the answers to the following questions - a template is provided. 1. (15 points) Using the information from the table below, calibrate the benchmark forward rates for the bino- mial tree using the forward induction method. Year Zero Rates 1 5.1% 2 5.3% 3 5.7% 4 5.9% 5 6.0% 6 6.5% 7 6.7% 22% You will take the last two digits of your UIN and divide by 50000 and then add that amount to each zero rate. For example, if your UIN is XXXXXxx51, then take 51/50000 = 0.00102 and add that to each rate (e.g., 0.051 +0.00102 = 0.05202, etc.) Tree Calibration (a) For each of the UIN adjusted zero rates, compute the zero coupon bond price - do this per $1 face which gives a present value factor. (b) The rate for the first period is fixed; however, you need to find a set of forward rates, which at each time step are linked by o, and which are also consistent with the respective zero coupon bond prices. For example, you will find a set of forwards yt2 such that P(412,0) = P2, where Pz is the zero coupon price. On the first step, you will have yi,2 and y1,2 = y1,2 e20vAt (Note: I simplify this by using annual rates with the number of steps equal to the number of years, so vAt = 1). (c) Once you find y1,2, use those rates, and repeat the process to find y2,3, i.e., forward induction. (d) Repeat the process to find y3,4,Y1,5, 45,6 and 46,7. You will implement the Black-Derman-Toy (1990) interest rate model to value a callable bond and to derive risk measures such as effective duration and effective convexity. It is recommended that you refer to your class notes for this project. Use Excel to generate the answers to the following questions - a template is provided. 1. (15 points) Using the information from the table below, calibrate the benchmark forward rates for the bino- mial tree using the forward induction method. Year Zero Rates 1 5.1% 2 5.3% 3 5.7% 4 5.9% 5 6.0% 6 6.5% 7 6.7% 22% You will take the last two digits of your UIN and divide by 50000 and then add that amount to each zero rate. For example, if your UIN is XXXXXxx51, then take 51/50000 = 0.00102 and add that to each rate (e.g., 0.051 +0.00102 = 0.05202, etc.) Tree Calibration (a) For each of the UIN adjusted zero rates, compute the zero coupon bond price - do this per $1 face which gives a present value factor. (b) The rate for the first period is fixed; however, you need to find a set of forward rates, which at each time step are linked by o, and which are also consistent with the respective zero coupon bond prices. For example, you will find a set of forwards yt2 such that P(412,0) = P2, where Pz is the zero coupon price. On the first step, you will have yi,2 and y1,2 = y1,2 e20vAt (Note: I simplify this by using annual rates with the number of steps equal to the number of years, so vAt = 1). (c) Once you find y1,2, use those rates, and repeat the process to find y2,3, i.e., forward induction. (d) Repeat the process to find y3,4,Y1,5, 45,6 and 46,7