I am currently trying to work through this, but I have had issues with NPV, PI, and IRR in the past and would really appreciate if someone could walk me through this so that I double check myself, as well as get a better grasp on the steps to solve these in general. Thank you!

| Input area: | | | | | |

| | | | | | |

| | | | | | |

| Initial equipment cost | $ 55,000,000 | | | | |

| Equipment in 1 year | $ 30,000,000 | | | | |

| Year 1 depreciation | 3.750% | | | | |

| Year 2 depreciation | 7.219% | | | | |

| Year 3 depreciation | 6.677% | | | | |

| Year 4 depreciation | 6.177% | | | | |

| Year 5 depreciation | 5.713% | | | | |

| | | | | | |

| | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 |

| Sales | $ 18,000,000 | $ 27,000,000 | $ 35,000,000 | $ 39,000,000 | $ 43,000,000 |

| Variable cost | 60% | | | | |

| Fixed cost | $ 3,500,000 | | | | |

| NWC percentage of sales | 8% | | | | |

| Terminal growth rate | 3% | | | | |

| Tax rate | 21% | | | | |

| Required return | 11.000% | | | | |

| | | | | | |

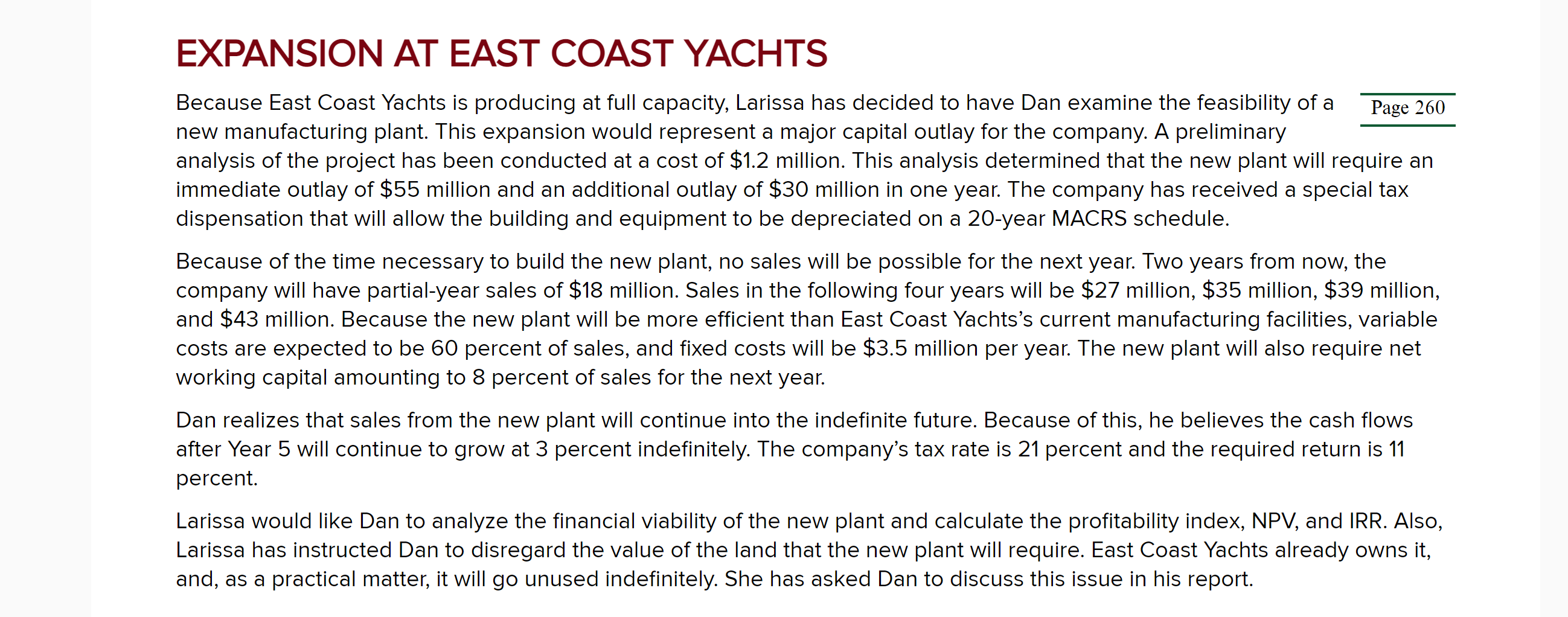

EXPANSION AT EAST COAST YACHTS Because East Coast Yachts is producing at full capacity, Larissa has decided to have Dan examine the feasibility of a Page 260 new manufacturing plant. This expansion would represent a major capital outlay for the company. A preliminary analysis of the project has been conducted at a cost of $1.2 million. This analysis determined that the new plant will require an immediate outlay of $55 million and an additional outlay of $30 million in one year. The company has received a special tax dispensation that will allow the building and equipment to be depreciated on a 20-year MACRS schedule. Because of the time necessary to build the new plant, no sales will be possible for the next year. Two years from now, the company will have partial-year sales of $18 million. Sales in the following four years will be $27 million, $35 million, $39 million, and $43 million. Because the new plant will be more efficient than East Coast Yachts's current manufacturing facilities, variable costs are expected to be 60 percent of sales, and fixed costs will be $3.5 million per year. The new plant will also require net working capital amounting to 8 percent of sales for the next year. Dan realizes that sales from the new plant will continue into the indefinite future. Because of this, he believes the cash flows after Year 5 will continue to grow at 3 percent indefinitely. The company's tax rate is 21 percent and the required return is 11 percent. Larissa would like Dan to analyze the financial viability of the new plant and calculate the profitability index, NPV, and IRR. Also, Larissa has instructed Dan to disregard the value of the land that the new plant will require. East Coast Yachts already owns it, and, as a practical matter, it will go unused indefinitely. She has asked Dan to discuss this issue in his report. EXPANSION AT EAST COAST YACHTS Because East Coast Yachts is producing at full capacity, Larissa has decided to have Dan examine the feasibility of a Page 260 new manufacturing plant. This expansion would represent a major capital outlay for the company. A preliminary analysis of the project has been conducted at a cost of $1.2 million. This analysis determined that the new plant will require an immediate outlay of $55 million and an additional outlay of $30 million in one year. The company has received a special tax dispensation that will allow the building and equipment to be depreciated on a 20-year MACRS schedule. Because of the time necessary to build the new plant, no sales will be possible for the next year. Two years from now, the company will have partial-year sales of $18 million. Sales in the following four years will be $27 million, $35 million, $39 million, and $43 million. Because the new plant will be more efficient than East Coast Yachts's current manufacturing facilities, variable costs are expected to be 60 percent of sales, and fixed costs will be $3.5 million per year. The new plant will also require net working capital amounting to 8 percent of sales for the next year. Dan realizes that sales from the new plant will continue into the indefinite future. Because of this, he believes the cash flows after Year 5 will continue to grow at 3 percent indefinitely. The company's tax rate is 21 percent and the required return is 11 percent. Larissa would like Dan to analyze the financial viability of the new plant and calculate the profitability index, NPV, and IRR. Also, Larissa has instructed Dan to disregard the value of the land that the new plant will require. East Coast Yachts already owns it, and, as a practical matter, it will go unused indefinitely. She has asked Dan to discuss this issue in his report