Question

I am done with 10, help me with 11 please In problem 10 above, assume that the standard deviation of security As return is 2%

I am done with 10, help me with 11 please

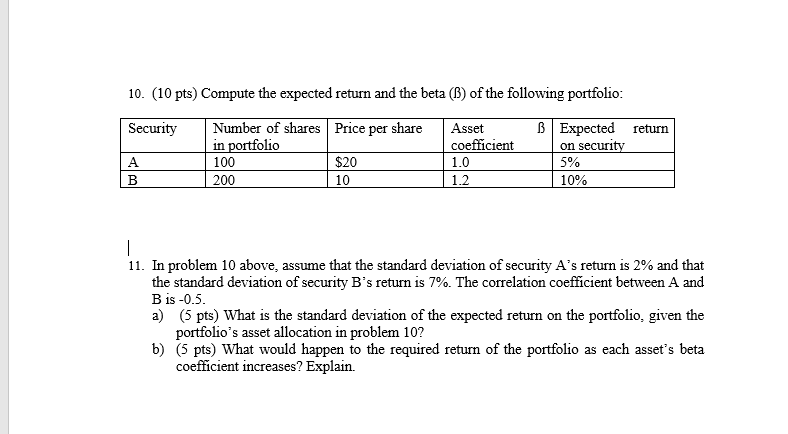

In problem 10 above, assume that the standard deviation of security As return is 2% and that the standard deviation of security Bs return is 7%. The correlation coefficient between A and B is -0.5. a) (5 pts) What is the standard deviation of the expected return on the portfolio, given the portfolios asset allocation in problem 10? b) (5 pts) What would happen to the required return of the portfolio as each assets beta coefficient increases? Explain.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Managers

Authors: Harvard Business School Press

1st Edition

1578518768, 978-1578518760