Answered step by step

Verified Expert Solution

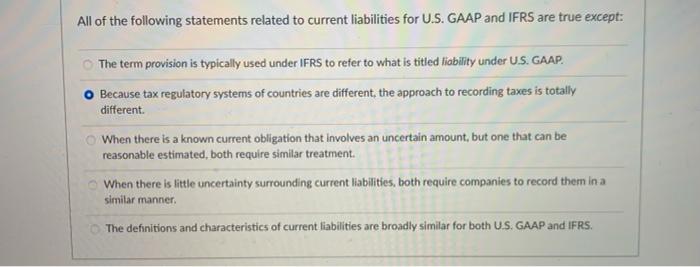

Question

1 Approved Answer

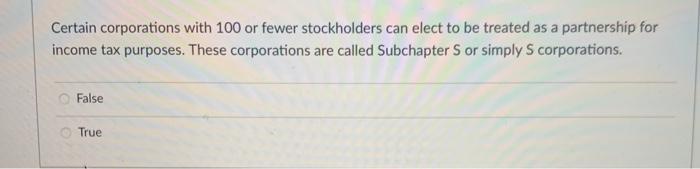

I am not sure about my answers. can you check and explain ? Certain corporations with 100 or fewer stockholders can elect to be treated

I am not sure about my answers. can you check and explain ?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

CyRM Mastering The Management Of Cybersecurity Internal Audit And IT Audit

Authors: David X Martin

1st Edition

0367757850, 978-0367757854