Question

I am required to Prepare a Taxation Worksheet on the next page in accordance with AASB 112 with following information. I have attached my attempt

I am required to Prepare a Taxation Worksheet on the next page in accordance with AASB 112 with following information. I have attached my attempt of the taxation worksheet and wondering if it is correct (very unsure about the insurance calculation)

Penguin Ltd began operations on 1 July 2019. One year after operations, the entity presents its first Statement of Comprehensive Income and Statement of Financial Position on 30 June 2020. However, the statements were prepared for internal purposes, but income tax calculations were ignored. Accounting profit before income tax for the year 30 June 2020 of Penguin Ltd amounted to $2,720,000, including the following revenue and expenses.

Revenue:

Sales 11,760,000

Expenses:

Other expenses 198,000

Rent 74,000

Wages and Salaries 720,000

Cost of sales 6,450,000

Administrative expenses 529,200

Doubtful debts 13,000

Long service leave 252,000

Warranty expenses 151,200

Depreciation – Plant & Machinery 201,000

Depreciation – Equipment 232,000

Depreciation expense – Furnitures and Fixtures 50,000

Insurance Expenses 138,600

Entertainment costs 44,000

Accounting profit for the year $2,720,000

Assets and Liabilities as disclosed in the Statement of Financial Position for the year ended 30 June 2017 $ $

Assets

Cash and cash equivalents 102,000

Inventory 502,800

Receivables (net) 378,000

Prepaid insurance 51,900

Plant– cost 2,010,000

Less accumulated depreciation 201,000

1,809,000

Equipment – cost 1,160,000

Less accumulated depreciation 232,000

928, 000

Furnitures and fixture – cost 600,000

Less accumulated depreciation 50,000

550, 000

Land 2,268,000

Total assets 6,589,700

Liabilities

Payables 403,200

Rent 50,000

Provision for warranty expenses 100,800

Loan payable 1,008,000

Provision for long service leave 56,000

Total liabilities 1,650,200

Net assets 4,939,500

Other information:

▪ The Plants & Machinery are depreciated over 10

over 8 years for taxation purposes. The useful life of computers is 4 years for the tax purposes and 5 years for accounting purposes. Therefore, there is a temporary difference between accounting and taxation depreciation for Plant & Machinery, and Equipment.

▪ All administration, wages and other expenses incurred have been paid as at year- end.

▪ Penguin Ltd has some land which cost $1,470,000 and which has been re-valued to its fair value of $2,268,000.

▪ Entertainment expenses and depreciation of furniture and fixtures are not allowed as deductions for income tax.

▪ The amount of $163,800 long service leave expense has been paid.

▪ Insurance was initially prepaid to the amount of $190,500. Actual amounts paid are

allowed as a tax deduction.

▪ Amounts received from sales, including those on credit terms, are taxed at the time

of the sale is made.

▪ Warranty expenses were accrued and, at the year-end, actual payments were made

of $50,400. Deductions for tax purposes are only available when the amounts are

paid and not as they accrued.

▪ The tax rate is 30 per cent.

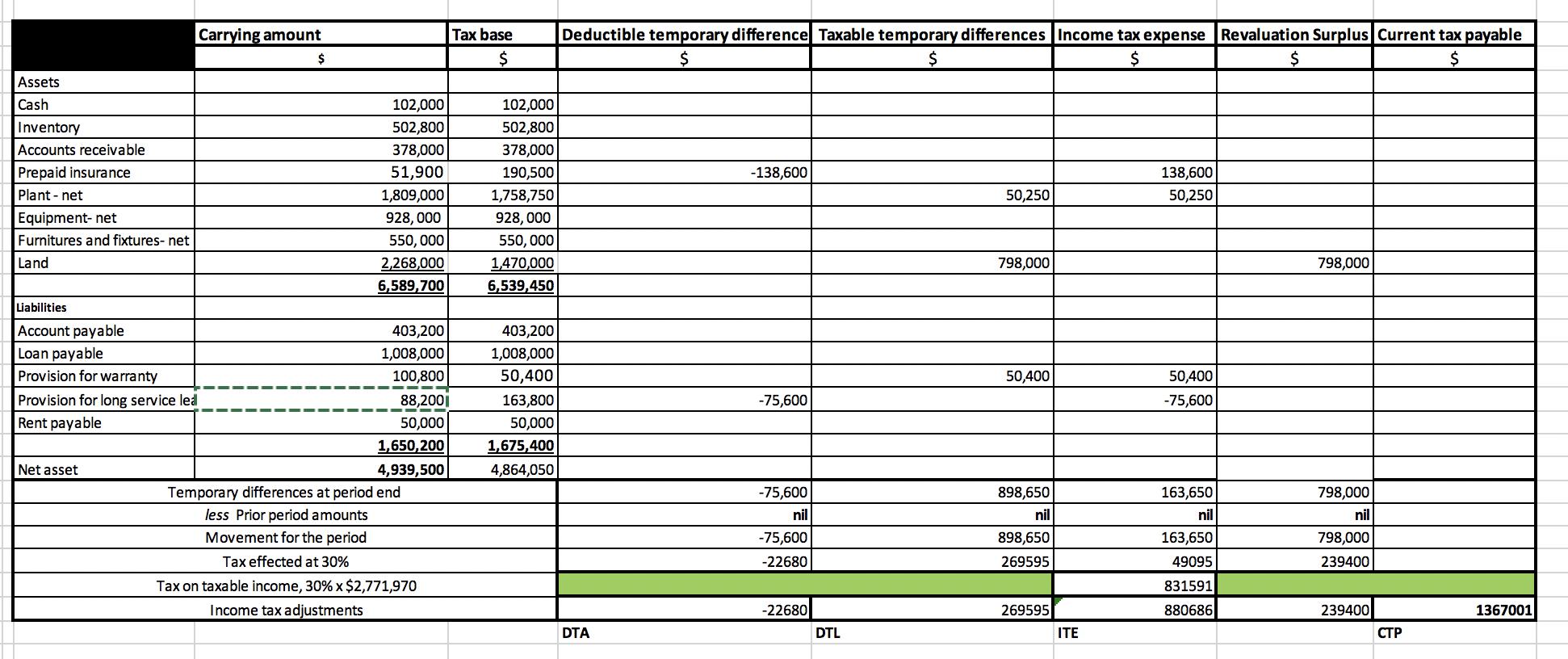

My attempt of taxation worksheet

Carrying amount Tax base Deductible temporary difference Taxable temporary differences Income tax expense Revaluation Surplus Current tax payable $ $ Assets Cash 102,000 102,000 Inventory 502,800 502,800 Accounts receivable 378,000 378,000 Prepaid insurance 51,900 190,500 -138,600 138,600 Plant - net 1,809,000 1,758,750 50,250 50,250 Equipment- net 928, 000 928, 000 Furnitures and fixtures- net 550, 000 550, 000 Land 1,470,000 6,539,450 2,268,000 798,000 798,000 6,589,700 Liabilities Account payable 403,200 403,200 Loan payable 1,008,000 1,008,000 Provision for warranty 100,800 50,400 50,400 50,400 Provision for long service led 88,200 163,800 -75,600 -75,600 Rent payable 50,000 50,000 1,650,200 1,675,400 Net asset 4,939,500 4,864,050 Temporary differences at period end -75,600 898,650 163,650 798,000 less Prior period amounts nil nil nil nil Movement for the period -75,600 898,650 163,650 798,000 Tax effected at 30% -22680 269595 49095 239400 Tax on taxable income, 30% x $2,771,970 831591 Income tax adjustments -22680 269595 880686 239400 1367001 DTA DTL ITE

Step by Step Solution

3.45 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

There are some mistake in formulaand Tax base value Equipment is not correct Correct Answer is given ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics For Business Decision Making And Analysis

Authors: Robert Stine, Dean Foster

2nd Edition

978-0321836519, 321836510, 978-0321890269