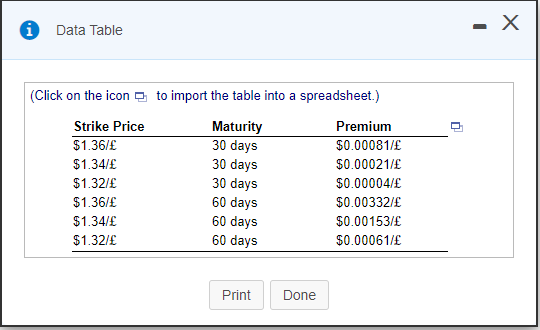

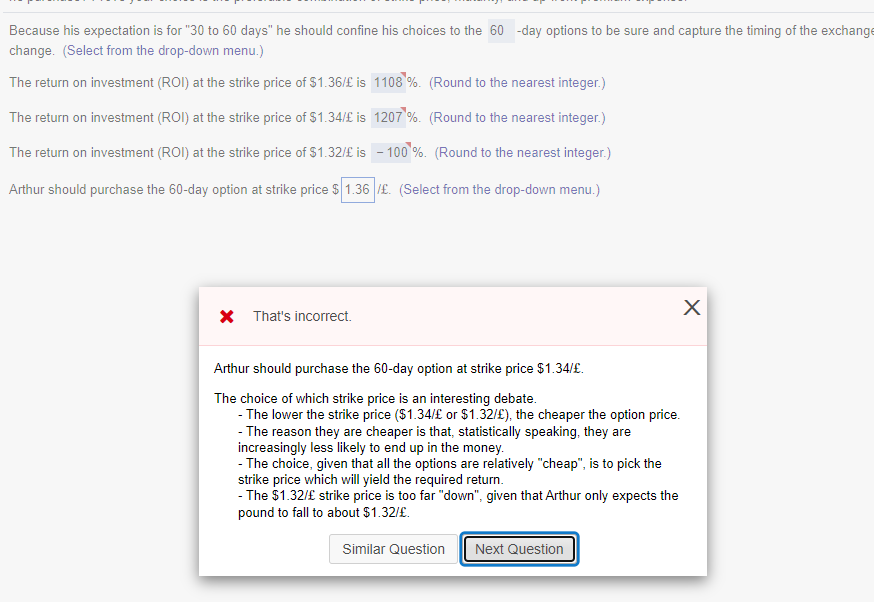

i Data Table 30 days (Click on the icon 2 to import the table into a spreadsheet.) Strike Price Maturity Premium $1.36/ $0.00081/ $1.34/ 30 days $0.00021/ $1.32/ 30 days $0.00004/ $1.36/ 60 days $0.00332/ $1.34/ 60 days $0.00153/ $1.32/ 60 days $0.00061/ Print Done Baker Street. Arthur Doyle is a currency trader for Baker Street, a private investment house in London. Baker Street's clients are a collection of wealthy private investors who, with a minimum stake of 220,000 each, wish to speculate on the movement of currencies. The investors expect annual returns in excess of 25%. Although officed in London, all accounts and expectations are based in U.S. dollars. Arthur is convinced that the British pound will slide significantlypossibly to $1.3200/in the coming 30 to 60 days. The current spot rate is $1.4263/. Arthur wishes to buy a put on pounds which will yield the 25% return expected by his investors. Which of the following put options, would you recommend he purchase? Prove your choice is the preferable combination of strike price, maturity, and up-front premium expense. Because his expectation is for "30 to 60 days" he should confine his choices to the 60-day options to be sure and capture the timing of the exchange rate change. (Select from the drop-down menu.) The return on investment (ROI) at the strike price of $1.36/ is%. (Round to the nearest integer.) Because his expectation is for "30 to 60 days" he should confine his choices to the 60-day options to be sure and capture the timing of the exchange change. (Select from the drop-down menu.) The return on investment (ROI) at the strike price of $1.36/ is 1108% (Round to the nearest integer.) The return on investment (ROI) at the strike price of $1.34/ is 1207 %. (Round to the nearest integer.) The return on investment (ROI) at the strike price of $1.32/ is - 100%. (Round to the nearest integer.) Arthur should purchase the 60-day option at strike price $ 1.36 /. (Select from the drop-down menu.) X That's incorrect. Arthur should purchase the 60-day option at strike price $1.34/. The choice of which strike price is an interesting debate. - The lower the strike price ($1.34/ or $1.32/), the cheaper the option price. - The reason they are cheaper is that, statistically speaking, they are increasingly less likely to end up in the money. - The choice, given that all the options are relatively "cheap", is to pick the strike price which will yield the required return. - The $1.32/ strike price is too far "down", given that Arthur only expects the pound to fall to about $1.32/. Similar Question Next Question i Data Table 30 days (Click on the icon 2 to import the table into a spreadsheet.) Strike Price Maturity Premium $1.36/ $0.00081/ $1.34/ 30 days $0.00021/ $1.32/ 30 days $0.00004/ $1.36/ 60 days $0.00332/ $1.34/ 60 days $0.00153/ $1.32/ 60 days $0.00061/ Print Done Baker Street. Arthur Doyle is a currency trader for Baker Street, a private investment house in London. Baker Street's clients are a collection of wealthy private investors who, with a minimum stake of 220,000 each, wish to speculate on the movement of currencies. The investors expect annual returns in excess of 25%. Although officed in London, all accounts and expectations are based in U.S. dollars. Arthur is convinced that the British pound will slide significantlypossibly to $1.3200/in the coming 30 to 60 days. The current spot rate is $1.4263/. Arthur wishes to buy a put on pounds which will yield the 25% return expected by his investors. Which of the following put options, would you recommend he purchase? Prove your choice is the preferable combination of strike price, maturity, and up-front premium expense. Because his expectation is for "30 to 60 days" he should confine his choices to the 60-day options to be sure and capture the timing of the exchange rate change. (Select from the drop-down menu.) The return on investment (ROI) at the strike price of $1.36/ is%. (Round to the nearest integer.) Because his expectation is for "30 to 60 days" he should confine his choices to the 60-day options to be sure and capture the timing of the exchange change. (Select from the drop-down menu.) The return on investment (ROI) at the strike price of $1.36/ is 1108% (Round to the nearest integer.) The return on investment (ROI) at the strike price of $1.34/ is 1207 %. (Round to the nearest integer.) The return on investment (ROI) at the strike price of $1.32/ is - 100%. (Round to the nearest integer.) Arthur should purchase the 60-day option at strike price $ 1.36 /. (Select from the drop-down menu.) X That's incorrect. Arthur should purchase the 60-day option at strike price $1.34/. The choice of which strike price is an interesting debate. - The lower the strike price ($1.34/ or $1.32/), the cheaper the option price. - The reason they are cheaper is that, statistically speaking, they are increasingly less likely to end up in the money. - The choice, given that all the options are relatively "cheap", is to pick the strike price which will yield the required return. - The $1.32/ strike price is too far "down", given that Arthur only expects the pound to fall to about $1.32/. Similar Question Next