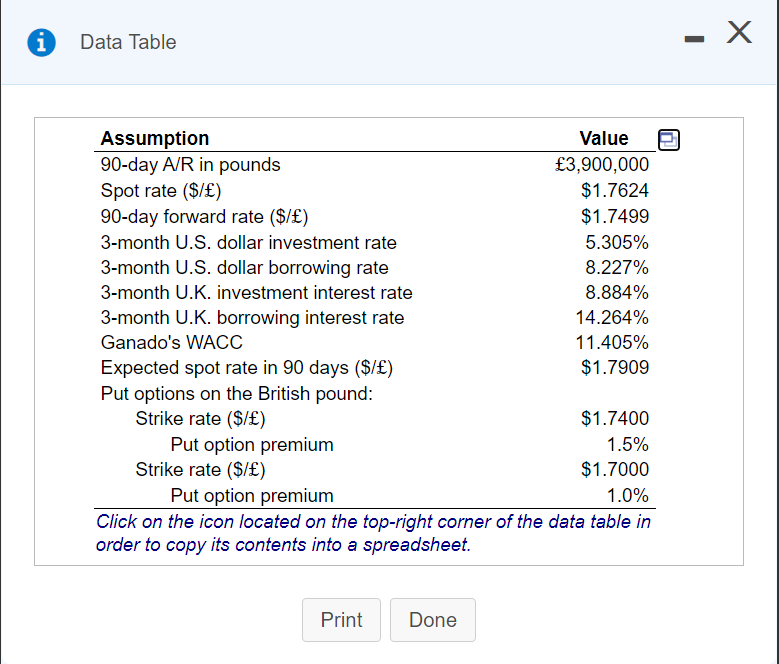

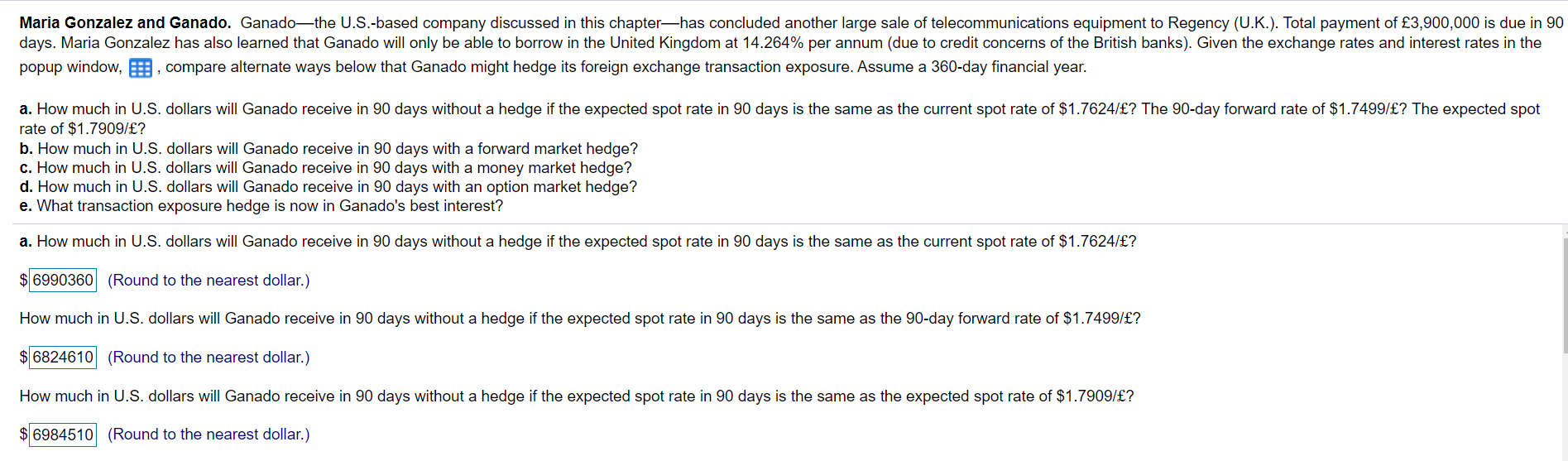

i Data Table x Assumption Value 90-day A/R in pounds 3,900,000 Spot rate ($/) $1.7624 90-day forward rate ($/) $1.7499 3-month U.S. dollar investment rate 5.305% 3-month U.S. dollar borrowing rate 8.227% 3-month U.K. investment interest rate 8.884% 3-month U.K. borrowing interest rate 14.264% Ganado's WACC 11.405% Expected spot rate in 90 days ($/) $1.7909 Put options on the British pound: Strike rate ($/) $1.7400 Put option premium 1.5% Strike rate ($/) $1.7000 Put option premium 1.0% Click on the icon located on the top-right corner of the data table in order to copy its contents into a spreadsheet. Print Done Maria Gonzalez and Ganado. Ganadothe U.S.-based company discussed in this chapter-has concluded another large sale of telecommunications equipment to Regency (U.K.). Total payment of 3,900,000 is due in 90 days. Maria Gonzalez has also learned that Ganado will only be able to borrow in the United Kingdom at 14.264% per annum (due to credit concerns of the British banks). Given the exchange rates and interest rates in the popup window, E, compare alternate ways below that Ganado might hedge its foreign exchange transaction exposure. Assume a 360-day financial year. 90 days is the same as the current spot rate of $1.7624/? The 90-day forward rate of $1.7499/? The expected spot a. How much in U.S. dollars will Ganado receive in days without a hedge if the expected spot rate rate of $1.7909/? b. How much in U.S. dollars will Ganado receive in days with a forward market hedge? c. How much in U.S. dollars will Ganado receive in 90 days with a money market hedge? d. How much in U.S. dollars will Ganado receive in days with an option market hedge? e. What transaction exposure hedge is now in Ganado's best interest? a. How much in U.S. dollars will Ganado receive in 90 days without a hedge if the expected spot rate 90 days is the same as the current spot rate of $1.7624/? $ 6990360 (Round to the nearest dollar.) How much in U.S. dollars will Ganado receive in 90 days without a hedge if the expected spot rate in 90 days is the same as the 90-day forward rate of $1.7499/? $ 6824610 (Round to the nearest dollar.) How much in U.S. dollars will Ganado receive in 90 days without a hedge if the expected spot rate in 90 days is the same as the expected spot rate of $1.7909/? 6984510 (Round to the nearest dollar.) b. How much in U.S. dollars will Ganado receive in 90 days with a forward market hedge? $ (Round to the nearest dollar.) c. How much in U.S. dollars will Ganado receive in 90 days with a money market hedge? (Round to the nearest dollar.) d. How much in U.S. dollars will Ganado receive in 90 days if Ganado covers the transaction exposure with the $1.7400/ put option and the pound depreciates below $1.7400/ in 90 days? (Round to the nearest dollar.) How much in U.S. dollars will Ganado receive in 90 days if Ganado covers the transaction exposure with the $1.7000/ put option and the pound depreciates below $1.7000/ in 90 days? $ (Round to the nearest dollar.) e. What transaction exposure hedge is now in Ganado's best interest? (Select from the drop-down menu.) The guarantees Ganado the greatest dollar value for the accounts receivable when using the cost of capital as the reinvestment rate (carry-forward rate). Enter your answer in each of the answer boxes