Answered step by step

Verified Expert Solution

Question

1 Approved Answer

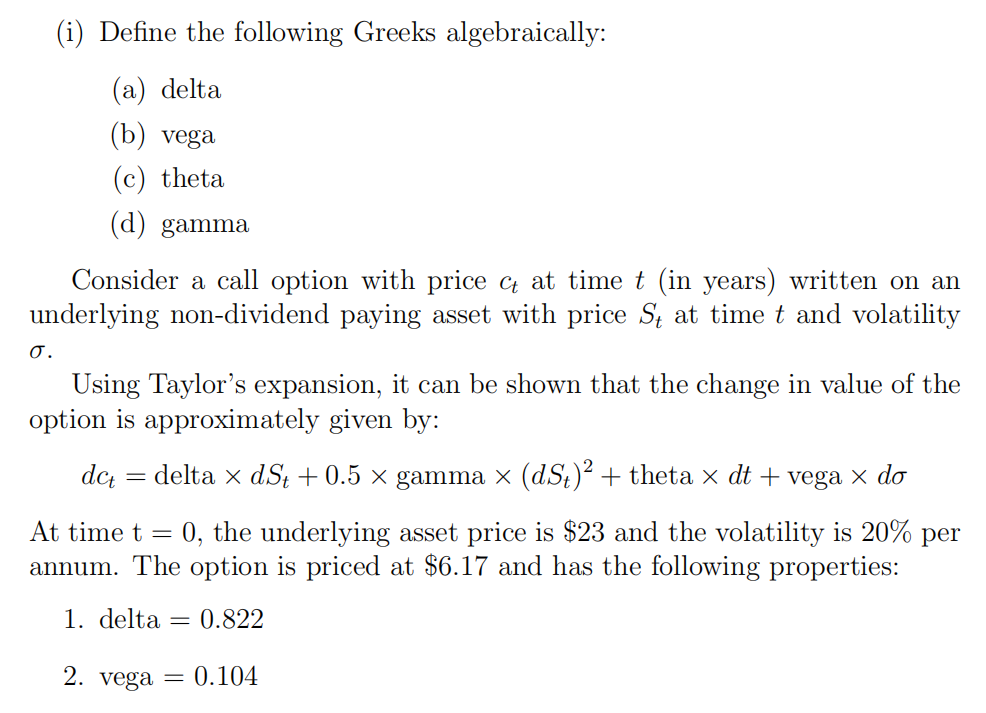

(i) Define the following Greeks algebraically: (a) delta (b) vega (c) theta (d) gamma Consider a call option with price C at time t (in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

MP Auditing And Assurance Services W/ACL Software CD ROM A Systematic Approach

Authors: William Messier Jr, Steven Glover, Douglas Prawitt

9th Edition

1259162346, 978-1259162343