Question

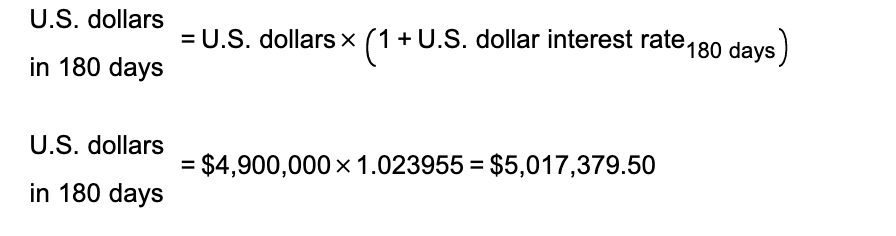

I don't know how they got the 1.023955. Can someone clarify please? Please refer to the info below: $4,900,000Kamada: CIA Japan (A).Takeshi Kamada, a foreign

I don't know how they got the 1.023955. Can someone clarify please? Please refer to the info below:

$4,900,000Kamada: CIA Japan (A).Takeshi Kamada, a foreign exchange trader at Credit Suisse (Tokyo), is exploring covered interest arbitrage possibilities. He wants to invest

or its yen equivalent, in a covered interest arbitrage between U.S. dollars and Japanese yen. He faced the following exchange rate and interest rate quotes. Is CIA profit possible? If so, how?

| Arbitrage funds available | $ | 4,900,000 | |

| Spot rate (/$) | 118.48 | ||

| 180-day forward rate (/$) | 117.74 | ||

| 180-day U.S. dollar interest rate | 4.791 | % | |

| 180-day Japanese yen interest rate | 3.393 | % |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Airline Finance

Authors: Peter S. Morrell

4th Edition

1351959743, 978-1351959742