Answered step by step

Verified Expert Solution

Question

1 Approved Answer

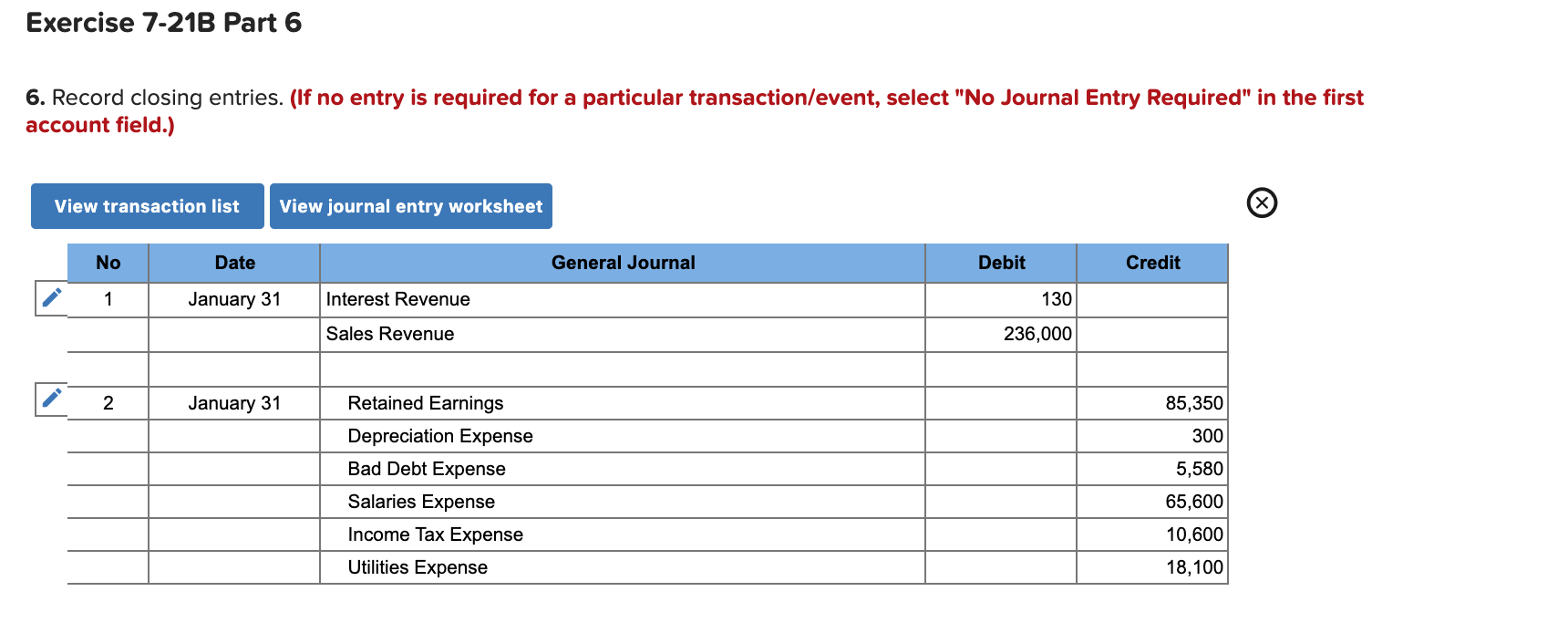

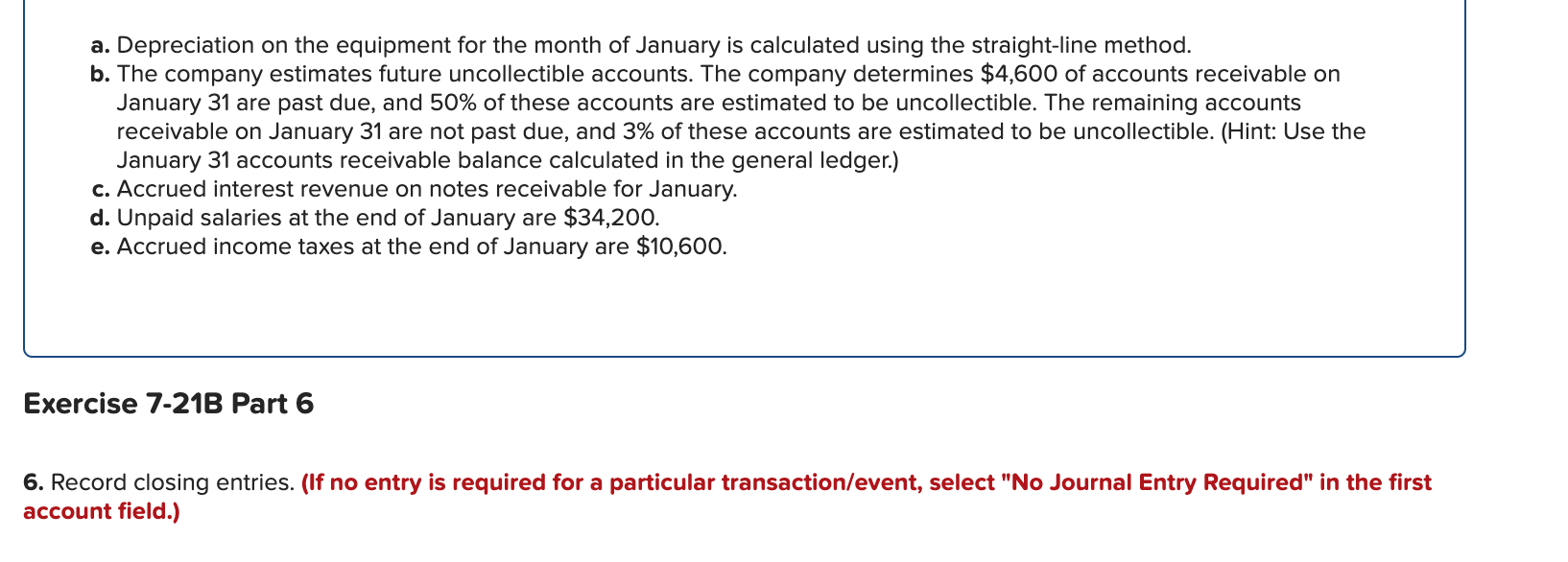

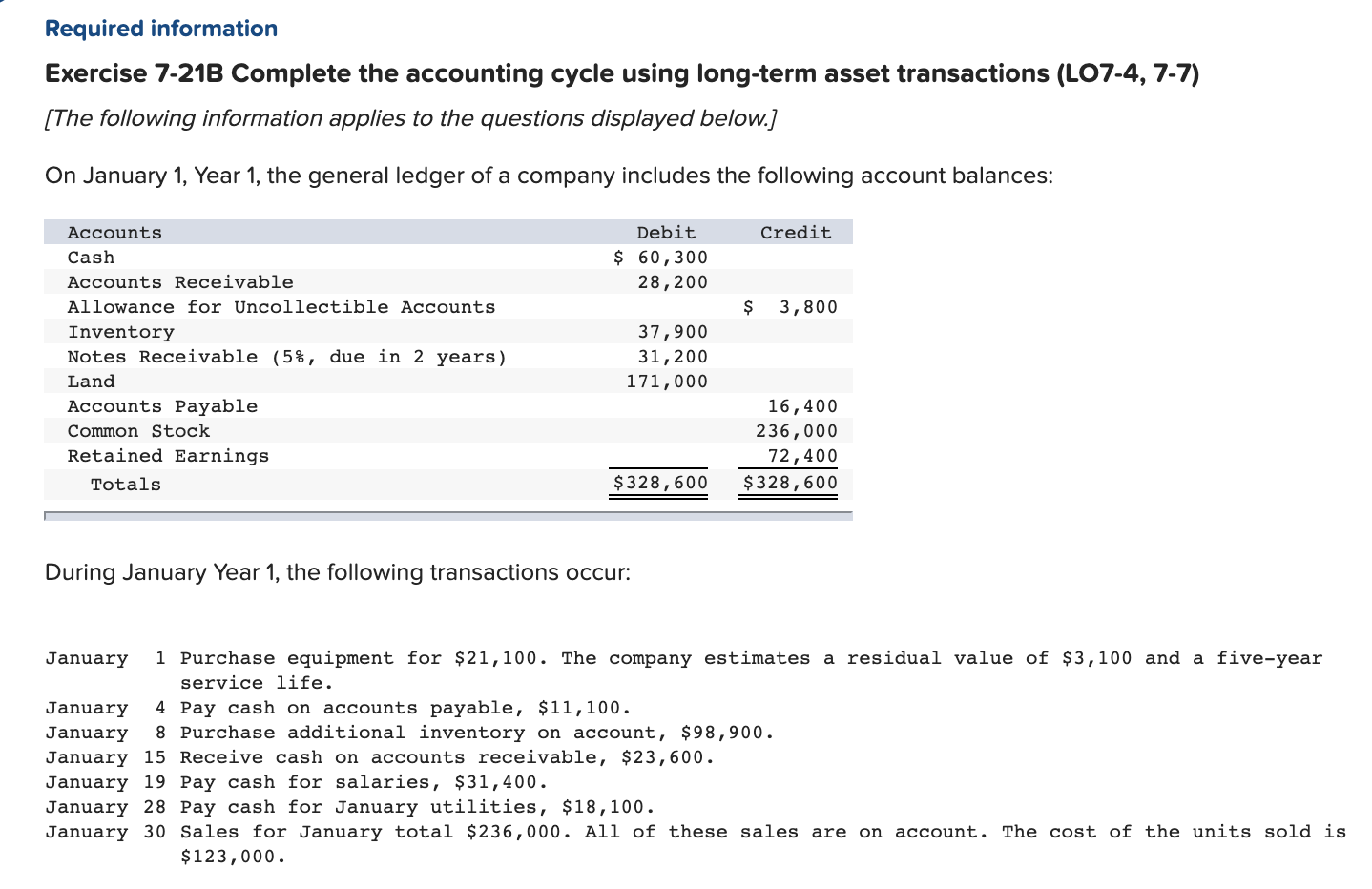

I don't know why the RETAINED EARNING still wrong. Exercise 7-21B Part 6 6. Record closing entries. (If no entry is required for a particular

I don't know why the RETAINED EARNING still wrong.

I don't know why the RETAINED EARNING still wrong.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Computer Auditing Security And Internal Control Manual

Authors: Javier F. Kuong

1st Edition

0131629670, 978-0131629677