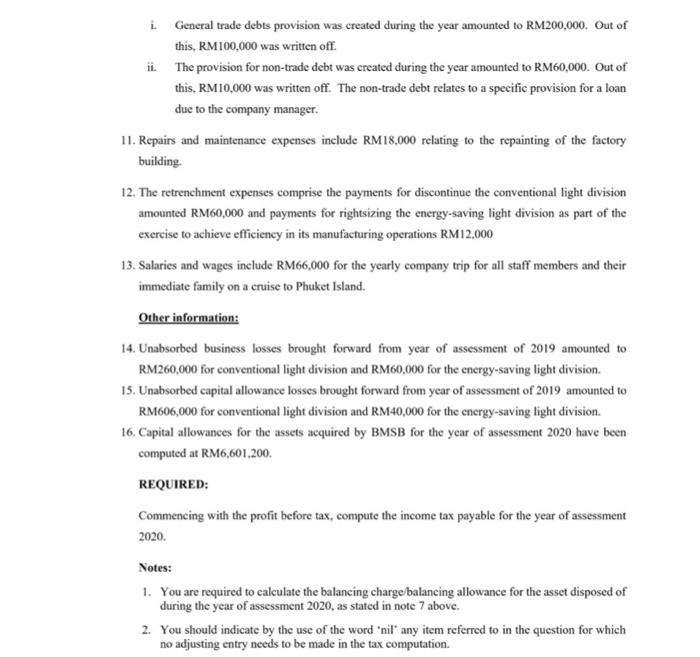

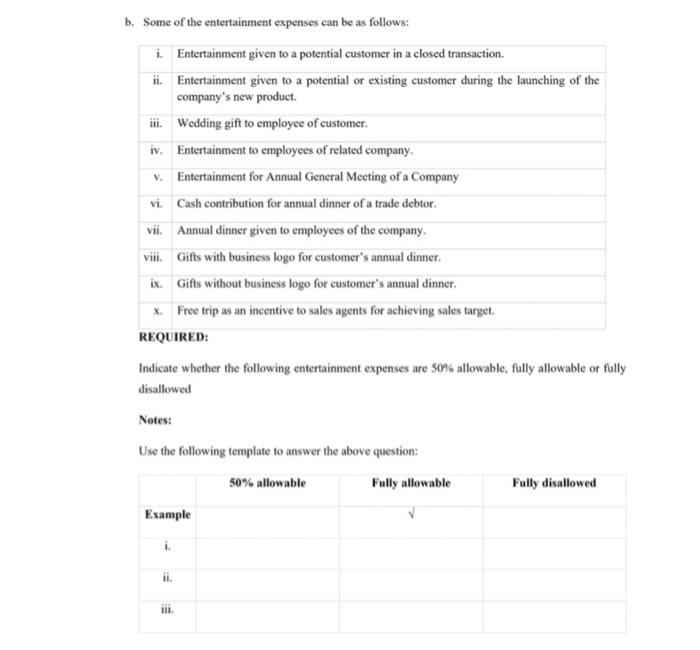

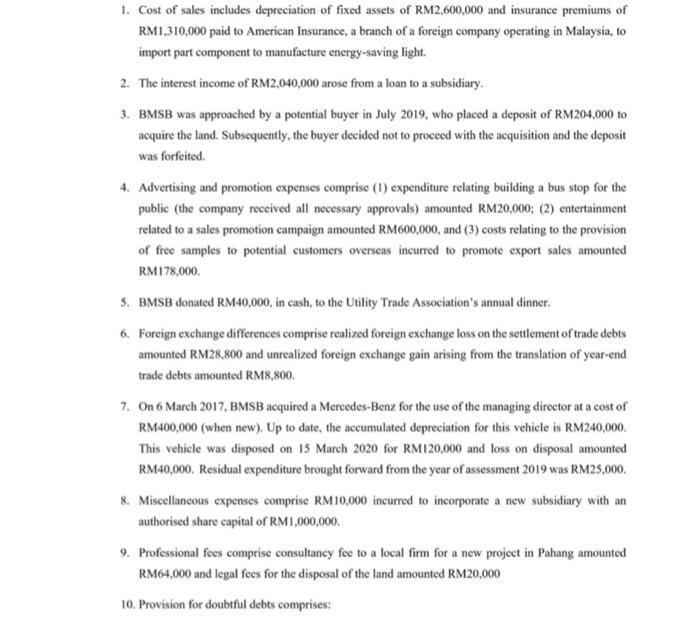

i General trade debts provision was created during the year amounted to RM200,000. Out of this, RM100,000 was written off. ii. The provision for non-trade debt was created during the year amounted to RM60,000. Out of this. RM10,000 was written off. The non-trade debt relates to a specific provision for a loan due to the company manager. 11. Repairs and maintenance expenses include RM18,000 relating to the repainting of the factory building 12. The retrenchment expenses comprise the payments for discontinue the conventional light division amounted RM60,000 and payments for rightsizing the energy-saving light division as part of the exercise to achieve efficiency in its manufacturing operations RM12,000 13. Salaries and wages include RM66,000 for the yearly company trip for all staff members and their immediate family on a cruise to Phuket Island. Other information: 14. Unabsorbed business losses brought forward from year of assessment of 2019 amounted to RM260,000 for conventional light division and RM60,000 for the energy-saving light division. 15. Unabsorbed capital allowance losses brought forward from year of assessment of 2019 amounted to RM606,000 for conventional light division and RM40,000 for the energy-saving light division. 16. Capital allowances for the assets acquired by BMSB for the year of assessment 2020 have been computed at RM6,601.200. REQUIRED: Commencing with the profit before tax, compute the income tax payable for the year of assessment 2020, Notes: 1. You are required to calculate the balancing charge balancing allowance for the asset disposed of during the year of assessment 2020, as stated in note 7 above. 2. You should indicate by the use of the word 'nil" any item referred to in the question for which no adjusting entry needs to be made in the tax computation. b. Some of the entertainment expenses can be as follows: i. Entertainment given to a potential customer in a closed transaction. ii. Entertainment given to a potential or existing customer during the launching of the company's new product. iii. Wedding gift to employee of customer. iv. Entertainment to employees of related company. V. Entertainment for Annual General Meeting of a Company vi Cash contribution for annual dinner of a trade debtor. vii. Annual dinner given to employees of the company. viii. Gifts with business logo for customer's annual dinner ix. Gifts without business logo for customer's annual dinner. * Free trip as an incentive to sales agents for achieving sales target. REQUIRED: Indicate whether the following entertainment expenses are 50% allowable, fully allowable or fully disallowed Notes: Use the following template to answer the above question: 50% allowable Fully allowable Fully disallowed Example il ili 1. Cost of sales includes depreciation of fixed assets of RM2,600,000 and insurance premiums of RM1,310,000 paid to American Insurance, a branch of a foreign company operating in Malaysia, to import part component to manufacture energy-saving light. 2. The interest income of RM2,040,000 arose from a loan to a subsidiary 3. BMSB was approached by a potential buyer in July 2019, who placed a deposit of RM204,000 to acquire the land. Subsequently, the buyer decided not to proceed with the acquisition and the deposit was forfeited. 4. Advertising and promotion expenses comprise (1) expenditure relating building a bus stop for the public (the company received all necessary approvals) amounted RM20,000; (2) entertainment related to a sales promotion campaign amounted RM600,000, and (3) costs relating to the provision of free samples to potential customers overseas incurred to promote export sales amounted RM 178,000 5. BMSB donated RM40,000, in cash, to the Utility Trade Association's annual dinner. 6. Foreign exchange differences comprise realized foreign exchange loss on the settlement of trade debts amounted RM28.800 and unrealized foreign exchange gain arising from the translation of year-end trade debts amounted RM8,800. 7. On 6 March 2017, BMSB acquired a Mercedes-Benz for the use of the managing director at a cost of RM400.000 (when new). Up to date, the accumulated depreciation for this vehicle is RM240,000. This vehicle was disposed on 15 March 2020 for RM120,000 and loss on disposal amounted RM40,000. Residual expenditure brought forward from the year of assessment 2019 was RM25,000. 8. Miscellancous expenses comprise RM10,000 incurred to incorporate a new subsidiary with an authorised share capital of RM 1,000,000 9. Professional fees comprise consultancy fee to a local firm for a new project in Pahang amounted RM64.000 and legal fees for the disposal of the land amounted RM20.000 10. Provision for doubtful debts comprises: i General trade debts provision was created during the year amounted to RM200,000. Out of this, RM100,000 was written off. ii. The provision for non-trade debt was created during the year amounted to RM60,000. Out of this. RM10,000 was written off. The non-trade debt relates to a specific provision for a loan due to the company manager. 11. Repairs and maintenance expenses include RM18,000 relating to the repainting of the factory building 12. The retrenchment expenses comprise the payments for discontinue the conventional light division amounted RM60,000 and payments for rightsizing the energy-saving light division as part of the exercise to achieve efficiency in its manufacturing operations RM12,000 13. Salaries and wages include RM66,000 for the yearly company trip for all staff members and their immediate family on a cruise to Phuket Island. Other information: 14. Unabsorbed business losses brought forward from year of assessment of 2019 amounted to RM260,000 for conventional light division and RM60,000 for the energy-saving light division. 15. Unabsorbed capital allowance losses brought forward from year of assessment of 2019 amounted to RM606,000 for conventional light division and RM40,000 for the energy-saving light division. 16. Capital allowances for the assets acquired by BMSB for the year of assessment 2020 have been computed at RM6,601.200. REQUIRED: Commencing with the profit before tax, compute the income tax payable for the year of assessment 2020, Notes: 1. You are required to calculate the balancing charge balancing allowance for the asset disposed of during the year of assessment 2020, as stated in note 7 above. 2. You should indicate by the use of the word 'nil" any item referred to in the question for which no adjusting entry needs to be made in the tax computation. b. Some of the entertainment expenses can be as follows: i. Entertainment given to a potential customer in a closed transaction. ii. Entertainment given to a potential or existing customer during the launching of the company's new product. iii. Wedding gift to employee of customer. iv. Entertainment to employees of related company. V. Entertainment for Annual General Meeting of a Company vi Cash contribution for annual dinner of a trade debtor. vii. Annual dinner given to employees of the company. viii. Gifts with business logo for customer's annual dinner ix. Gifts without business logo for customer's annual dinner. * Free trip as an incentive to sales agents for achieving sales target. REQUIRED: Indicate whether the following entertainment expenses are 50% allowable, fully allowable or fully disallowed Notes: Use the following template to answer the above question: 50% allowable Fully allowable Fully disallowed Example il ili 1. Cost of sales includes depreciation of fixed assets of RM2,600,000 and insurance premiums of RM1,310,000 paid to American Insurance, a branch of a foreign company operating in Malaysia, to import part component to manufacture energy-saving light. 2. The interest income of RM2,040,000 arose from a loan to a subsidiary 3. BMSB was approached by a potential buyer in July 2019, who placed a deposit of RM204,000 to acquire the land. Subsequently, the buyer decided not to proceed with the acquisition and the deposit was forfeited. 4. Advertising and promotion expenses comprise (1) expenditure relating building a bus stop for the public (the company received all necessary approvals) amounted RM20,000; (2) entertainment related to a sales promotion campaign amounted RM600,000, and (3) costs relating to the provision of free samples to potential customers overseas incurred to promote export sales amounted RM 178,000 5. BMSB donated RM40,000, in cash, to the Utility Trade Association's annual dinner. 6. Foreign exchange differences comprise realized foreign exchange loss on the settlement of trade debts amounted RM28.800 and unrealized foreign exchange gain arising from the translation of year-end trade debts amounted RM8,800. 7. On 6 March 2017, BMSB acquired a Mercedes-Benz for the use of the managing director at a cost of RM400.000 (when new). Up to date, the accumulated depreciation for this vehicle is RM240,000. This vehicle was disposed on 15 March 2020 for RM120,000 and loss on disposal amounted RM40,000. Residual expenditure brought forward from the year of assessment 2019 was RM25,000. 8. Miscellancous expenses comprise RM10,000 incurred to incorporate a new subsidiary with an authorised share capital of RM 1,000,000 9. Professional fees comprise consultancy fee to a local firm for a new project in Pahang amounted RM64.000 and legal fees for the disposal of the land amounted RM20.000 10. Provision for doubtful debts comprises