Question

I have the answer key for this question, but I specifically need explanations for the following, please look at the question and provide a detailed

I have the answer key for this question, but I specifically need explanations for the following, please look at the question and provide a detailed explanation. Thanks.

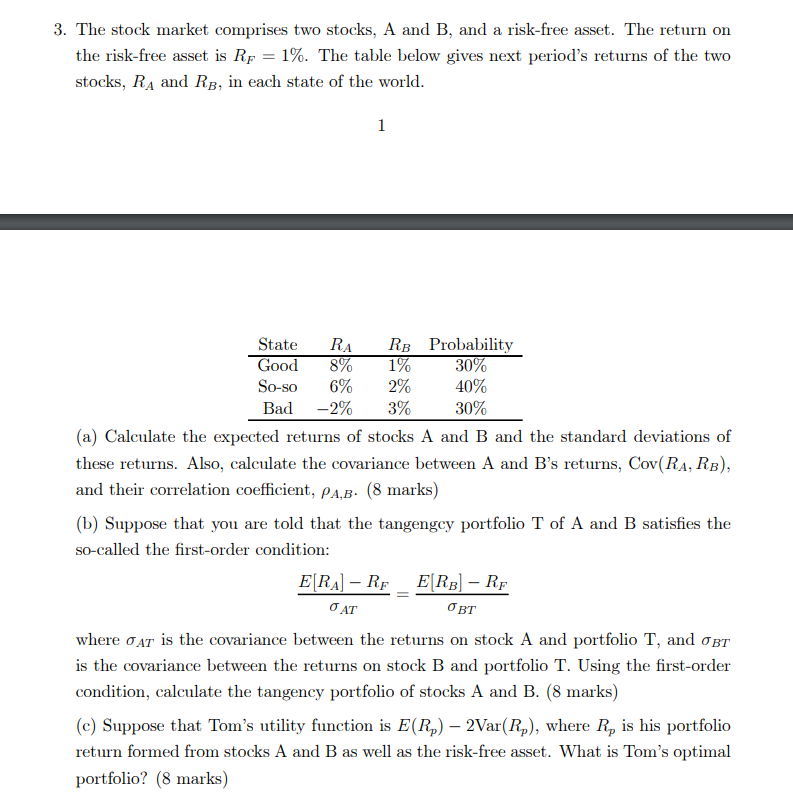

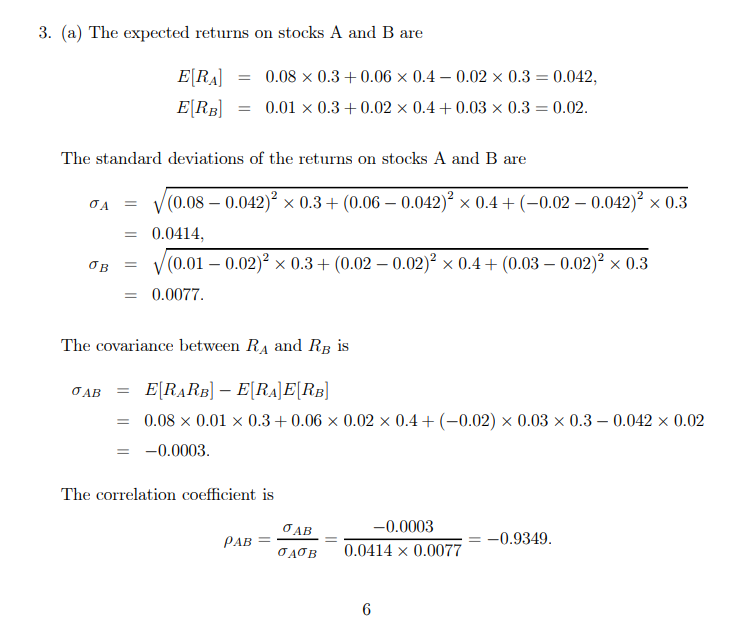

1. From part B, why is the covariance between the stock A (or stock B) with the tangency portfolio found using the covariance between stocks A and B times the weight of B (or A)?

2. From part C, please explain the denominator in the formula for the weight for the riskless asset. What is a? Why is a = 2?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Health Care Finance Basic Tools For Nonfinancial Managers

Authors: Judith J. Baker, R.W. Baker

3rd Edition

076377894X, 978-0763778941