i have the answer no need to answer it anymore

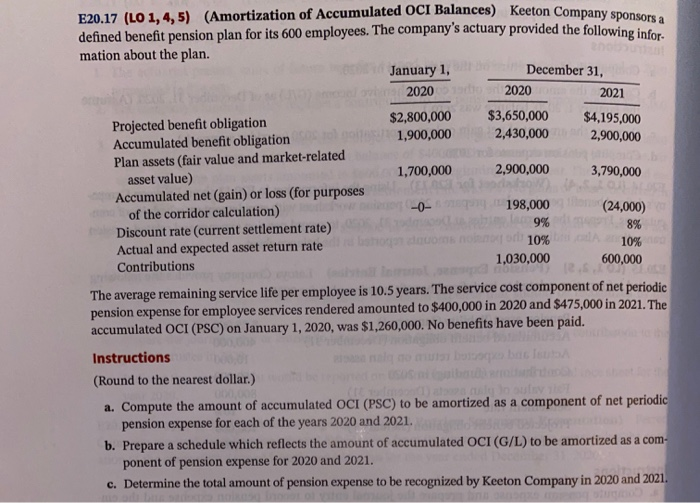

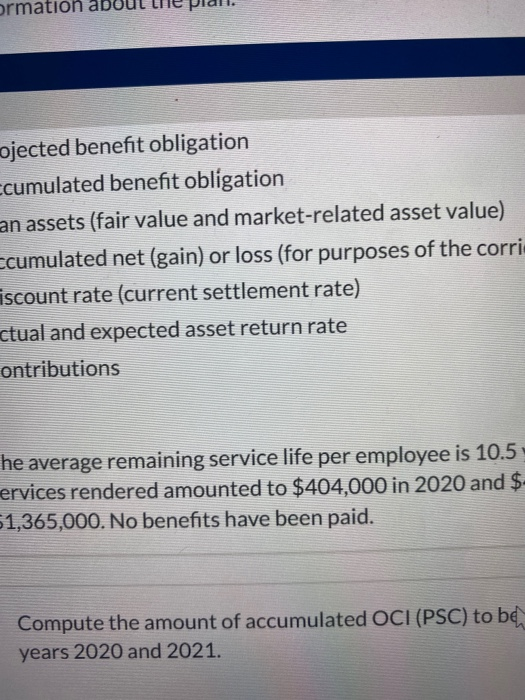

E20.17 (LO 1,4,5) (Amortization of Accumulated OCI Balances) Keeton Company defined benefit pension plan for its 600 employees. The company's actuary provided the following in mation about the plan. January 1, December 31, 2020 2 020 2021 Projected benefit obligation $2,800,000 $3,650,000 $4,195,000 1,900,000 2,430,000 Accumulated benefit obligation 2,900,000 Plan assets (fair value and market-related 1,700,000 2,900,000 asset value) 3,790,000 Accumulated net (gain) or loss (for purposes -0- of the corridor calculation) 9 198,000 (24,000) Discount rate (current settlement rate) on 10% 10% Actual and expected asset return rate Contributions 1,030,000 600,000 8% The average remaining service life per employee is 10.5 years. The service cost component of net periodic pension expense for employee services rendered amounted to $400,000 in 2020 and $475,000 in 2021. The accumulated OCI (PSC) on January 1, 2020, was $1,260,000. No benefits have been paid. Instructions (Round to the nearest dollar.) a. Compute the amount of accumulated OCI (PSC) to be amortized as a component of net periodic pension expense for each of the years 2020 and 2021. b. Prepare a schedule which reflects the amount of accumulated OCI (G/L) to be amortized as a com ponent of pension expense for 2020 and 2021. c. Determine the total amount of pension expense to be recognized by Keeton Company in 2020 and 2021 ormation about lie piall. ojected benefit obligation ccumulated benefit obligation an assets (fair value and market-related asset value) ccumulated net (gain) or loss (for purposes of the corri iscount rate (current settlement rate) ctual and expected asset return rate ontributions he average remaining service life per employee is 10.5 ervices rendered amounted to $404,000 in 2020 and $- 51,365,000. No benefits have been paid. Compute the amount of accumulated OCI (PSC) to be! years 2020 and 2021. E20.17 (LO 1,4,5) (Amortization of Accumulated OCI Balances) Keeton Company defined benefit pension plan for its 600 employees. The company's actuary provided the following in mation about the plan. January 1, December 31, 2020 2 020 2021 Projected benefit obligation $2,800,000 $3,650,000 $4,195,000 1,900,000 2,430,000 Accumulated benefit obligation 2,900,000 Plan assets (fair value and market-related 1,700,000 2,900,000 asset value) 3,790,000 Accumulated net (gain) or loss (for purposes -0- of the corridor calculation) 9 198,000 (24,000) Discount rate (current settlement rate) on 10% 10% Actual and expected asset return rate Contributions 1,030,000 600,000 8% The average remaining service life per employee is 10.5 years. The service cost component of net periodic pension expense for employee services rendered amounted to $400,000 in 2020 and $475,000 in 2021. The accumulated OCI (PSC) on January 1, 2020, was $1,260,000. No benefits have been paid. Instructions (Round to the nearest dollar.) a. Compute the amount of accumulated OCI (PSC) to be amortized as a component of net periodic pension expense for each of the years 2020 and 2021. b. Prepare a schedule which reflects the amount of accumulated OCI (G/L) to be amortized as a com ponent of pension expense for 2020 and 2021. c. Determine the total amount of pension expense to be recognized by Keeton Company in 2020 and 2021 ormation about lie piall. ojected benefit obligation ccumulated benefit obligation an assets (fair value and market-related asset value) ccumulated net (gain) or loss (for purposes of the corri iscount rate (current settlement rate) ctual and expected asset return rate ontributions he average remaining service life per employee is 10.5 ervices rendered amounted to $404,000 in 2020 and $- 51,365,000. No benefits have been paid. Compute the amount of accumulated OCI (PSC) to be! years 2020 and 2021