Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I just need answer of Q3. Q1 is just for your help. please answer both parts of Q3 as soon as possible. $865 = My

I just need answer of Q3. Q1 is just for your help. please answer both parts of Q3 as soon as possible.

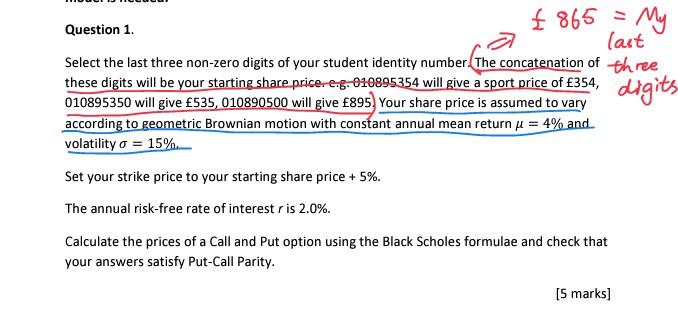

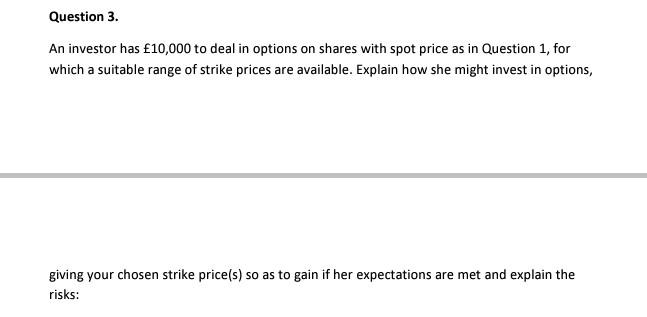

$865 = My Question 1. last Select the last three non-zero digits of your student identity number. The concatenation of three , digits 010895350 will give 535, 010890500 will give 895) Your share price is assumed to vary according to geometric Brownian motion with constant annual mean return u = 4% and volatility o = 15% Set your strike price to your starting share price + 5%. The annual risk-free rate of interest r is 2.0%. Calculate the prices of a Call and Put option using the Black Scholes formulae and check that your answers satisfy Put-Call Parity. [5 marks] Question 3. An investor has 10,000 to deal in options on shares with spot price as in Question 1, for which a suitable range of strike prices are available. Explain how she might invest in options, giving your chosen strike price(s) so as to gain if her expectations are met and explain the risks: d) Receive the risk-free interest rate over a set time period? Note that a combination of derivatives will be needed here. e) For a) and b) compare the investor's ability to make gains and exposure to losses compared with buying and selling shares directly, giving mathematical evidence for your claims. $865 = My Question 1. last Select the last three non-zero digits of your student identity number. The concatenation of three , digits 010895350 will give 535, 010890500 will give 895) Your share price is assumed to vary according to geometric Brownian motion with constant annual mean return u = 4% and volatility o = 15% Set your strike price to your starting share price + 5%. The annual risk-free rate of interest r is 2.0%. Calculate the prices of a Call and Put option using the Black Scholes formulae and check that your answers satisfy Put-Call Parity. [5 marks] Question 3. An investor has 10,000 to deal in options on shares with spot price as in Question 1, for which a suitable range of strike prices are available. Explain how she might invest in options, giving your chosen strike price(s) so as to gain if her expectations are met and explain the risks: d) Receive the risk-free interest rate over a set time period? Note that a combination of derivatives will be needed here. e) For a) and b) compare the investor's ability to make gains and exposure to losses compared with buying and selling shares directly, giving mathematical evidence for your claimsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Social Responsibility Audit A Management Tool For Survival

Authors: John W Humble

1st Edition

0900853522, 978-0900853524