i just need the cost of goods manufactured budget, ending finished goods inventory budget, and cost of goods sold budget. thank you

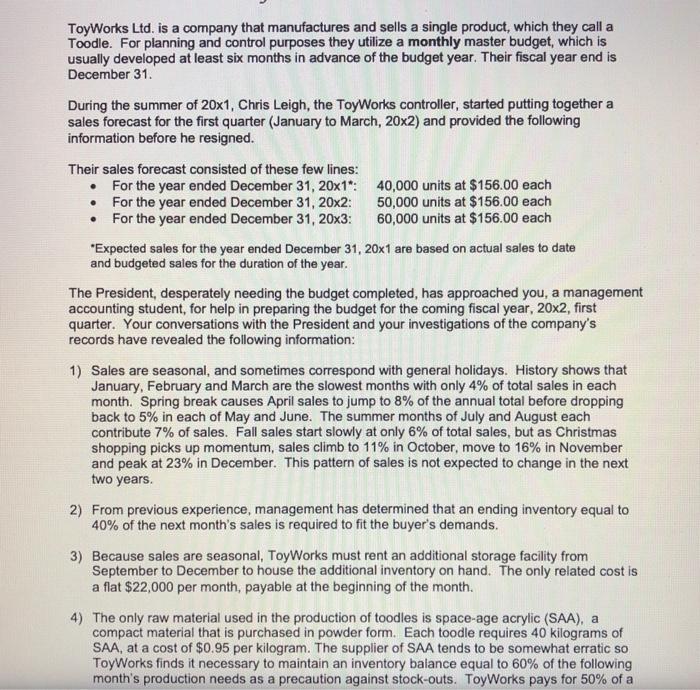

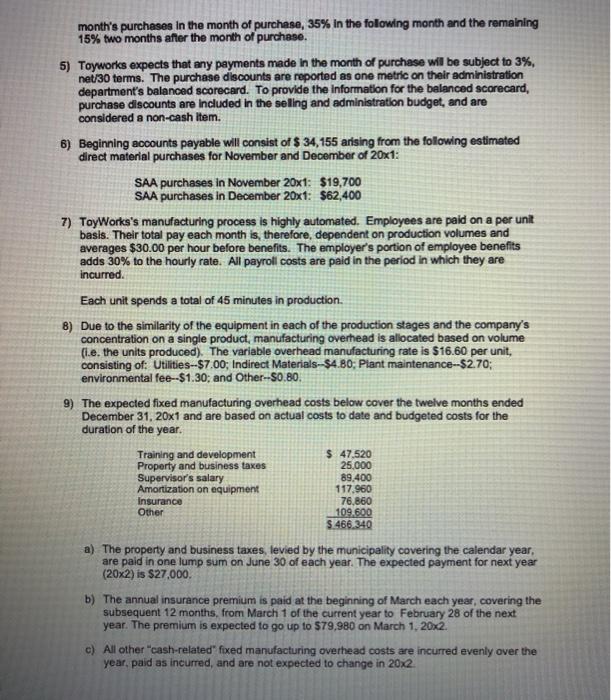

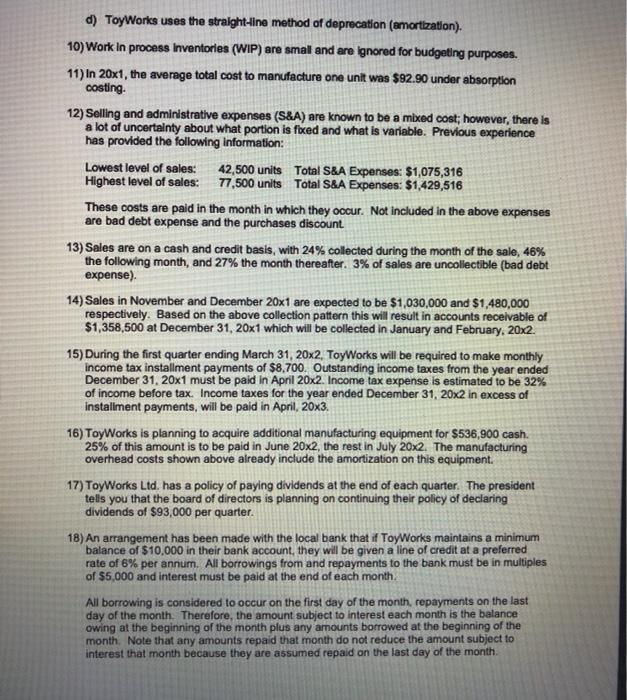

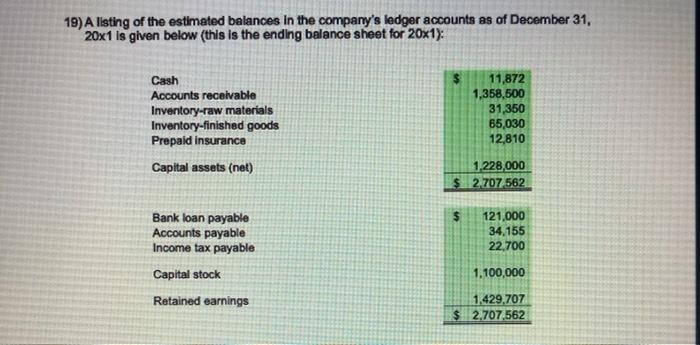

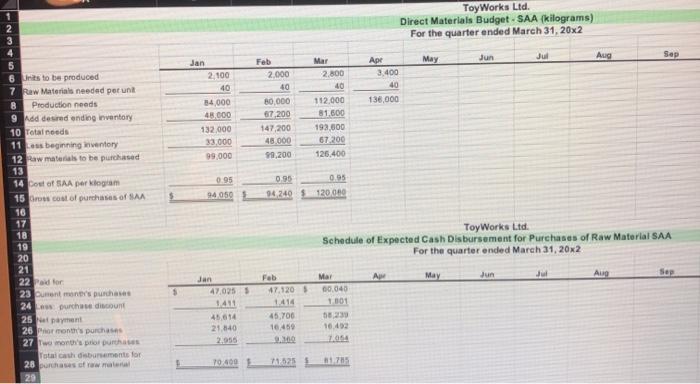

. . ToyWorks Ltd. is a company that manufactures and sells a single product, which they call a Toodle. For planning and control purposes they utilize a monthly master budget, which is usually developed at least six months in advance of the budget year. Their fiscal year end is December 31 During the summer of 20x1, Chris Leigh, the ToyWorks controller, started putting together a sales forecast for the first quarter (January to March, 20x2) and provided the following information before he resigned. Their sales forecast consisted of these few lines: For the year ended December 31, 20x1": 40,000 units at $156.00 each For the year ended December 31, 20x2: 50,000 units at $156.00 each For the year ended December 31, 20x3: 60,000 units at $156.00 each "Expected sales for the year ended December 31, 20x1 are based on actual sales to date and budgeted sales for the duration of the year. The President, desperately needing the budget completed, has approached you, a management accounting student, for help in preparing the budget for the coming fiscal year, 20x2, first quarter. Your conversations with the President and your investigations of the company's records have revealed the following information: 1) Sales are seasonal, and sometimes correspond with general holidays. History shows that January, February and March are the slowest months with only 4% of total sales in each month. Spring break causes April sales to jump to 8% of the annual total before dropping back to 5% in each of May and June. The summer months of July and August each contribute 7% of sales. Fall sales start slowly at only 6% of total sales, but as Christmas shopping picks up momentum, sales climb to 11% in October, move to 16% in November and peak at 23% in December. This pattern of sales is not expected to change in the next two years. 2) From previous experience, management has determined that an ending inventory equal to 40% of the next month's sales is required to fit the buyer's demands. 3) Because sales are seasonal, ToyWorks must rent an additional storage facility from September to December to house the additional inventory on hand. The only related cost is a flat $22,000 per month, payable at the beginning of the month. 4) The only raw material used in the production of toodles is space-age acrylic (SAA), a compact material that is purchased in powder form. Each toodle requires 40 kilograms of SAA, at a cost of $0.95 per kilogram. The supplier of SAA tends to be somewhat erratic so ToyWorks finds it necessary to maintain an inventory balance equal to 60% of the following month's production needs as a precaution against stock-outs. ToyWorks pays for 50% of a month's purchases in the month of purchase, 35% in the folowing month and the remaining 15% two months after the month of purchase. 5) Toyworks expects that any payments made in the month of purchase will be subject to 3%, net/30 terms. The purchase discounts are reported as one metric on their administration department's balanced Scorecard. To provide the information for the balanced Scorecard, purchase discounts are included in the selling and administration budget, and are considered a non-cash item. 6) Beginning accounts payable will consist of $ 34,155 arising from the following estimated direct material purchases for November and December of 20x1: SAA purchases in November 20x1: $19,700 SAA purchases in December 20x1: $62,400 7) ToyWorks's manufacturing process is highly automated. Employees are paid on a per unit basis. Their total pay each month is, therefore, dependent on production volumes and averages $30.00 per hour before benefits. The employer's portion of employee benefits adds 30% to the hourly rate. All payroll costs are paid in the period in which they are incurred. Each unit spends a total of 45 minutes in production. B) Due to the similarity of the equipment in each of the production stages and the company's concentration on a single product, manufacturing overhead is allocated based on volume file. the units produced). The variable overhead manufacturing rate is $16.60 per unit, consisting of: Utilities--$7.00; Indirect Materials--$4.80; Plant maintenance--$2.70; environmental fee--$1.30; and Other--50.80 9) The expected fixed manufacturing overhead costs below cover the twelve months ended December 31, 20x1 and are based on actual costs to date and budgeted costs for the duration of the year. Training and development $ 47,520 Property and business taxes 25,000 Supervisor's salary 89.400 Amortization on equipment 117.960 Insurance 76,860 Other 109.600 $.466.340 a) The property and business taxes, levied by the municipality covering the calendar year, are paid in one lump sum on June 30 of each year. The expected payment for next year (20x2) is $27.000 b) The annual insurance premium is paid at the beginning of March each year, covering the subsequent 12 months, from March 1 of the current year to February 28 of the next year. The premium is expected to go up to $79,980 on March 1, 20x2. c) All other "cash-related fixed manufacturing overhead costs are incurred evenly over the year. paid as incurred, and are not expected to change in 20X2 d) ToyWorks uses the straight-line method of deprecation (amortization). 10) Work in process inventories (WIP) are small and are ignored for budgeting purposes. 11) In 20x1, the average total cost to manufacture one unit was $92.90 under absorption costing. 12) Selling and administrative expenses (S&A) are known to be a mixed cost; however, there is a lot of uncertainty about what portion is foxed and what is variable. Previous experience has provided the following information: Lowest level of sales: 42,500 units Total S&A Expenses: $1,075,316 Highest level of sales: 77,500 units Total S&A Expenses: $1,429,516 These costs are paid in the month in which they occur. Not included in the above expenses are bad debt expense and the purchases discount 13) Sales are on a cash and credit basis, with 24% collected during the month of the sale, 46% the following month, and 27% the month thereafter. 3% of sales are uncollectible (bad debt expense). 14) Sales in November and December 20x1 are expected to be $1,030,000 and $1,480,000 respectively. Based on the above collection pattern this will result in accounts receivable of $1,358,500 at December 31, 20x1 which will be collected in January and February, 20x2. 15) During the first quarter ending March 31, 20x2, ToyWorks will be required to make monthly income tax installment payments of $8,700. Outstanding income taxes from the year ended December 31, 20x1 must be paid in April 20x2. Income tax expense is estimated to be 32% of income before tax. Income taxes for the year ended December 31, 20x2 in excess of installment payments, will be paid in April, 20x3. 16) ToyWorks is planning to acquire additional manufacturing equipment for $536,900 cash. 25% of this amount is to be paid in June 20x2, the rest in July 20x2. The manufacturing overhead costs shown above already include the amortization on this equipment. 17) ToyWorks Ltd. has a policy of paying dividends at the end of each quarter. The president tells you that the board of directors is planning on continuing their policy of declaring dividends of $93,000 per quarter. 18) An arrangement has been made with the local bank that if ToyWorks maintains a minimum balance of $10,000 in their bank account, they will be given a line of credit at a preferred rate of 6% per annum. All borrowings from and repayments to the bank must be in multiples of $5,000 and interest must be paid at the end of each month. All borrowing is considered to occur on the first day of the month, repayments on the last day of the month. Therefore, the amount subject to interest each month is the balance owing at the beginning of the month plus any amounts borrowed at the beginning of the month. Note that any amounts repaid that month do not reduce the amount subject to interest that month because they are assumed repaid on the last day of the month 19) A listing of the estimated balances in the company's ledger accounts as of December 31, 20x1 is given below (this is the ending balance sheet for 20x1); Cash Accounts receivable Inventory-raw materials Inventory-finished goods Prepaid insurance Capital assets (net) 11,872 1,358,500 31,350 65,030 12,810 1,228,000 2.707562 121.000 34.155 22,700 Bank loan payable Accounts payable Income tax payable Capital stock Retained earnings 1,100,000 1.429,707 2.707,562 Cost of Goods Manufactured Budget ignoring WIP inventories Ending Finished Goods Inventory Budget Cost of Goods Sold Budget Selling and Administrative Expense Budget Cash Budget 2. Prepare a budgeted income statement and a budgeted statement of retained earnings for the first quarter ended March 31, 20x2, using the absorption costing. 3. Prepare a budgeted balance sheet as at March 31, 20x2. ToyWorks Ltd. Direct Materials Budget - SAA (kilograms) For the quarter ended March 31, 20x2 May Jun Aug Sep Feb 2.000 40 Apr 3,400 40 136,000 Jan 2.100 40 54.000 48.000 132.000 33.000 99 000 80.000 67 200 147,200 48.000 99,200 Mar 2,800 40 112.000 81.500 192,000 67 200 125.400 0.95 94050 0.95 0.95 96 240 120.000 4 5 6 Units to be produced 7 Raw Materials needed per un 8 Production needs 9 Add desired ending inventory 10 Total needs 11 beginning inventory 12 Raw materials to be purchased 13 14 Dout of SAA per totam 15 os cost of purchases of SA 16 17 18 19 20 21 22d for 23 Dumont mone's purchases 24 purchase discount 25 payment 26 por month's purchases 27two mont's peor purchases Totalcah disbursements for 28 purchases of rawa 29 ToyWorks Ltd Schedule of Expected Cash Disbursement for Purchases of Raw Material SAA For the quarter onded March 31, 20x2 Am May Jun JU Aug Sep Feb 17.120 Jan 47,025 1411 45.614 21.840 Mar 00.000 1 001 5023 16.43 1.064 45.700 16,459 9.100 70,400 11:52 . . ToyWorks Ltd. is a company that manufactures and sells a single product, which they call a Toodle. For planning and control purposes they utilize a monthly master budget, which is usually developed at least six months in advance of the budget year. Their fiscal year end is December 31 During the summer of 20x1, Chris Leigh, the ToyWorks controller, started putting together a sales forecast for the first quarter (January to March, 20x2) and provided the following information before he resigned. Their sales forecast consisted of these few lines: For the year ended December 31, 20x1": 40,000 units at $156.00 each For the year ended December 31, 20x2: 50,000 units at $156.00 each For the year ended December 31, 20x3: 60,000 units at $156.00 each "Expected sales for the year ended December 31, 20x1 are based on actual sales to date and budgeted sales for the duration of the year. The President, desperately needing the budget completed, has approached you, a management accounting student, for help in preparing the budget for the coming fiscal year, 20x2, first quarter. Your conversations with the President and your investigations of the company's records have revealed the following information: 1) Sales are seasonal, and sometimes correspond with general holidays. History shows that January, February and March are the slowest months with only 4% of total sales in each month. Spring break causes April sales to jump to 8% of the annual total before dropping back to 5% in each of May and June. The summer months of July and August each contribute 7% of sales. Fall sales start slowly at only 6% of total sales, but as Christmas shopping picks up momentum, sales climb to 11% in October, move to 16% in November and peak at 23% in December. This pattern of sales is not expected to change in the next two years. 2) From previous experience, management has determined that an ending inventory equal to 40% of the next month's sales is required to fit the buyer's demands. 3) Because sales are seasonal, ToyWorks must rent an additional storage facility from September to December to house the additional inventory on hand. The only related cost is a flat $22,000 per month, payable at the beginning of the month. 4) The only raw material used in the production of toodles is space-age acrylic (SAA), a compact material that is purchased in powder form. Each toodle requires 40 kilograms of SAA, at a cost of $0.95 per kilogram. The supplier of SAA tends to be somewhat erratic so ToyWorks finds it necessary to maintain an inventory balance equal to 60% of the following month's production needs as a precaution against stock-outs. ToyWorks pays for 50% of a month's purchases in the month of purchase, 35% in the folowing month and the remaining 15% two months after the month of purchase. 5) Toyworks expects that any payments made in the month of purchase will be subject to 3%, net/30 terms. The purchase discounts are reported as one metric on their administration department's balanced Scorecard. To provide the information for the balanced Scorecard, purchase discounts are included in the selling and administration budget, and are considered a non-cash item. 6) Beginning accounts payable will consist of $ 34,155 arising from the following estimated direct material purchases for November and December of 20x1: SAA purchases in November 20x1: $19,700 SAA purchases in December 20x1: $62,400 7) ToyWorks's manufacturing process is highly automated. Employees are paid on a per unit basis. Their total pay each month is, therefore, dependent on production volumes and averages $30.00 per hour before benefits. The employer's portion of employee benefits adds 30% to the hourly rate. All payroll costs are paid in the period in which they are incurred. Each unit spends a total of 45 minutes in production. B) Due to the similarity of the equipment in each of the production stages and the company's concentration on a single product, manufacturing overhead is allocated based on volume file. the units produced). The variable overhead manufacturing rate is $16.60 per unit, consisting of: Utilities--$7.00; Indirect Materials--$4.80; Plant maintenance--$2.70; environmental fee--$1.30; and Other--50.80 9) The expected fixed manufacturing overhead costs below cover the twelve months ended December 31, 20x1 and are based on actual costs to date and budgeted costs for the duration of the year. Training and development $ 47,520 Property and business taxes 25,000 Supervisor's salary 89.400 Amortization on equipment 117.960 Insurance 76,860 Other 109.600 $.466.340 a) The property and business taxes, levied by the municipality covering the calendar year, are paid in one lump sum on June 30 of each year. The expected payment for next year (20x2) is $27.000 b) The annual insurance premium is paid at the beginning of March each year, covering the subsequent 12 months, from March 1 of the current year to February 28 of the next year. The premium is expected to go up to $79,980 on March 1, 20x2. c) All other "cash-related fixed manufacturing overhead costs are incurred evenly over the year. paid as incurred, and are not expected to change in 20X2 d) ToyWorks uses the straight-line method of deprecation (amortization). 10) Work in process inventories (WIP) are small and are ignored for budgeting purposes. 11) In 20x1, the average total cost to manufacture one unit was $92.90 under absorption costing. 12) Selling and administrative expenses (S&A) are known to be a mixed cost; however, there is a lot of uncertainty about what portion is foxed and what is variable. Previous experience has provided the following information: Lowest level of sales: 42,500 units Total S&A Expenses: $1,075,316 Highest level of sales: 77,500 units Total S&A Expenses: $1,429,516 These costs are paid in the month in which they occur. Not included in the above expenses are bad debt expense and the purchases discount 13) Sales are on a cash and credit basis, with 24% collected during the month of the sale, 46% the following month, and 27% the month thereafter. 3% of sales are uncollectible (bad debt expense). 14) Sales in November and December 20x1 are expected to be $1,030,000 and $1,480,000 respectively. Based on the above collection pattern this will result in accounts receivable of $1,358,500 at December 31, 20x1 which will be collected in January and February, 20x2. 15) During the first quarter ending March 31, 20x2, ToyWorks will be required to make monthly income tax installment payments of $8,700. Outstanding income taxes from the year ended December 31, 20x1 must be paid in April 20x2. Income tax expense is estimated to be 32% of income before tax. Income taxes for the year ended December 31, 20x2 in excess of installment payments, will be paid in April, 20x3. 16) ToyWorks is planning to acquire additional manufacturing equipment for $536,900 cash. 25% of this amount is to be paid in June 20x2, the rest in July 20x2. The manufacturing overhead costs shown above already include the amortization on this equipment. 17) ToyWorks Ltd. has a policy of paying dividends at the end of each quarter. The president tells you that the board of directors is planning on continuing their policy of declaring dividends of $93,000 per quarter. 18) An arrangement has been made with the local bank that if ToyWorks maintains a minimum balance of $10,000 in their bank account, they will be given a line of credit at a preferred rate of 6% per annum. All borrowings from and repayments to the bank must be in multiples of $5,000 and interest must be paid at the end of each month. All borrowing is considered to occur on the first day of the month, repayments on the last day of the month. Therefore, the amount subject to interest each month is the balance owing at the beginning of the month plus any amounts borrowed at the beginning of the month. Note that any amounts repaid that month do not reduce the amount subject to interest that month because they are assumed repaid on the last day of the month 19) A listing of the estimated balances in the company's ledger accounts as of December 31, 20x1 is given below (this is the ending balance sheet for 20x1); Cash Accounts receivable Inventory-raw materials Inventory-finished goods Prepaid insurance Capital assets (net) 11,872 1,358,500 31,350 65,030 12,810 1,228,000 2.707562 121.000 34.155 22,700 Bank loan payable Accounts payable Income tax payable Capital stock Retained earnings 1,100,000 1.429,707 2.707,562 Cost of Goods Manufactured Budget ignoring WIP inventories Ending Finished Goods Inventory Budget Cost of Goods Sold Budget Selling and Administrative Expense Budget Cash Budget 2. Prepare a budgeted income statement and a budgeted statement of retained earnings for the first quarter ended March 31, 20x2, using the absorption costing. 3. Prepare a budgeted balance sheet as at March 31, 20x2. ToyWorks Ltd. Direct Materials Budget - SAA (kilograms) For the quarter ended March 31, 20x2 May Jun Aug Sep Feb 2.000 40 Apr 3,400 40 136,000 Jan 2.100 40 54.000 48.000 132.000 33.000 99 000 80.000 67 200 147,200 48.000 99,200 Mar 2,800 40 112.000 81.500 192,000 67 200 125.400 0.95 94050 0.95 0.95 96 240 120.000 4 5 6 Units to be produced 7 Raw Materials needed per un 8 Production needs 9 Add desired ending inventory 10 Total needs 11 beginning inventory 12 Raw materials to be purchased 13 14 Dout of SAA per totam 15 os cost of purchases of SA 16 17 18 19 20 21 22d for 23 Dumont mone's purchases 24 purchase discount 25 payment 26 por month's purchases 27two mont's peor purchases Totalcah disbursements for 28 purchases of rawa 29 ToyWorks Ltd Schedule of Expected Cash Disbursement for Purchases of Raw Material SAA For the quarter onded March 31, 20x2 Am May Jun JU Aug Sep Feb 17.120 Jan 47,025 1411 45.614 21.840 Mar 00.000 1 001 5023 16.43 1.064 45.700 16,459 9.100 70,400 11:52