I know the answer isn't B. Please help and explain, thank you!

I know the answer isn't B. Please help and explain, thank you!

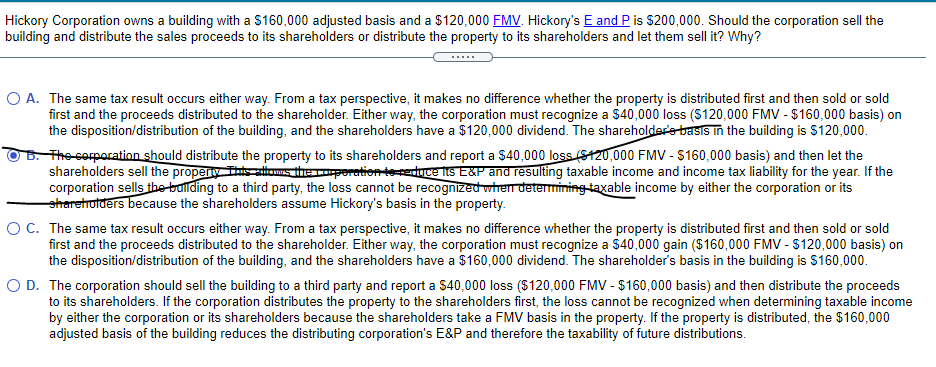

Hickory Corporation owns a building with a $160,000 adjusted basis and a $120,000 FMV. Hickory's E and P is $200,000. Should the corporation sell the building and distribute the sales proceeds to its shareholders or distribute the property to its shareholders and let them sell it? Why? O A. The same tax result occurs either way. From a tax perspective, it makes no difference whether the property is distributed first and then sold or sold first and the proceeds distributed to the shareholder. Either way, the corporation must recognize a $40,000 loss ($120,000 FMV - $160,000 basis) on the disposition/distribution of the building, and the shareholders have a $120,000 dividend. The shareholders basis in the building is $120,000. The corporation should distribute the property to its shareholders and report a $40,000 loss ($120,000 FMV - $160,000 basis) and then let the shareholders sell the property Tits attoms the corporation teseduce its E&P and resulting taxable income and income tax liability for the year. If the corporation sells the bouilding to a third party, the loss cannot be recognized when determining taxable income by either the corporation or its sherretrolders because the shareholders assume Hickory's basis in the property. O C. The same tax result occurs either way. From a tax perspective, it makes no difference whether the property is distributed first and then sold or sold first and the proceeds distributed to the shareholder. Either way, the corporation must recognize a $40,000 gain ($160,000 FMV - $120,000 basis) on the disposition/distribution of the building, and the shareholders have a $160,000 dividend. The shareholder's basis in the building is $160,000. OD. The corporation should sell the building to a third party and report a $40,000 loss ($120,000 FMV - $160,000 basis) and then distribute the proceeds to its shareholders. If the corporation distributes the property to the shareholders first, the loss cannot be recognized when determining taxable income by either the corporation or its shareholders because the shareholders take a FMV basis in the property. If the property is distributed, the $160,000 adjusted basis of the building reduces the distributing corporation's E&P and therefore the taxability of future distributions. Hickory Corporation owns a building with a $160,000 adjusted basis and a $120,000 FMV. Hickory's E and P is $200,000. Should the corporation sell the building and distribute the sales proceeds to its shareholders or distribute the property to its shareholders and let them sell it? Why? O A. The same tax result occurs either way. From a tax perspective, it makes no difference whether the property is distributed first and then sold or sold first and the proceeds distributed to the shareholder. Either way, the corporation must recognize a $40,000 loss ($120,000 FMV - $160,000 basis) on the disposition/distribution of the building, and the shareholders have a $120,000 dividend. The shareholders basis in the building is $120,000. The corporation should distribute the property to its shareholders and report a $40,000 loss ($120,000 FMV - $160,000 basis) and then let the shareholders sell the property Tits attoms the corporation teseduce its E&P and resulting taxable income and income tax liability for the year. If the corporation sells the bouilding to a third party, the loss cannot be recognized when determining taxable income by either the corporation or its sherretrolders because the shareholders assume Hickory's basis in the property. O C. The same tax result occurs either way. From a tax perspective, it makes no difference whether the property is distributed first and then sold or sold first and the proceeds distributed to the shareholder. Either way, the corporation must recognize a $40,000 gain ($160,000 FMV - $120,000 basis) on the disposition/distribution of the building, and the shareholders have a $160,000 dividend. The shareholder's basis in the building is $160,000. OD. The corporation should sell the building to a third party and report a $40,000 loss ($120,000 FMV - $160,000 basis) and then distribute the proceeds to its shareholders. If the corporation distributes the property to the shareholders first, the loss cannot be recognized when determining taxable income by either the corporation or its shareholders because the shareholders take a FMV basis in the property. If the property is distributed, the $160,000 adjusted basis of the building reduces the distributing corporation's E&P and therefore the taxability of future distributions