Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need 100% correct answer will be upvote (2) Q.88 A risk manager wants to stress a bank's USD 320 million real-estate loan portfolio. Although

I need 100% correct answer will be upvote

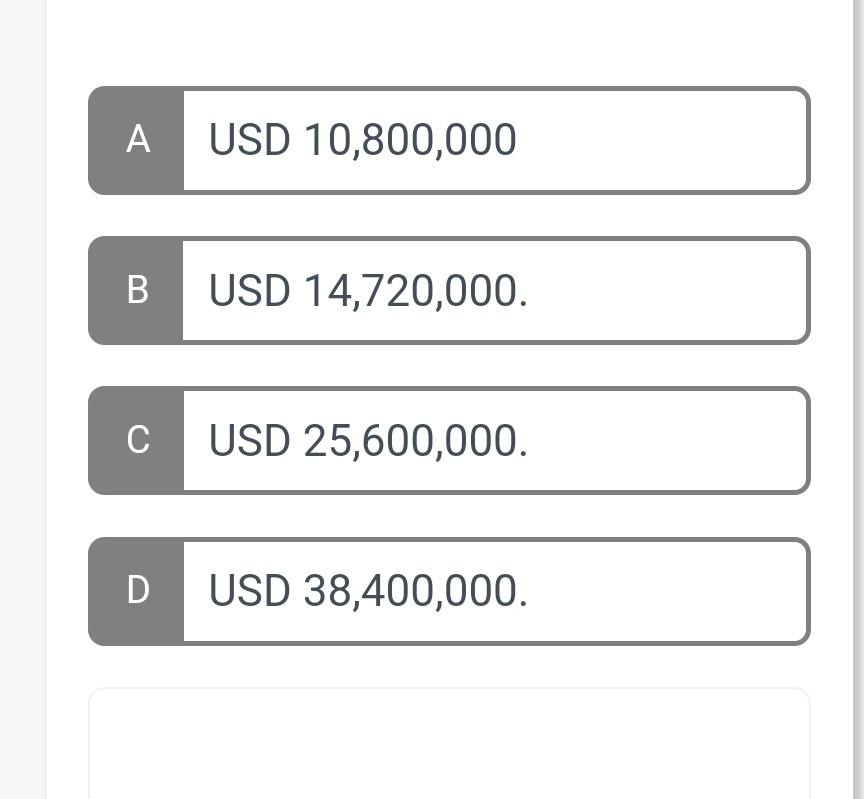

(2) Q.88 A risk manager wants to stress a bank's USD 320 million real-estate loan portfolio. Although at the moment the average probability of default (PD) for the portfolio is pretty high (11.5%), the bank's management doesn't worry about the improvement of the credit quality of the portfolio as the collateral for the loans is a very expensive commercial property that always had high demand. Based on the experience of 2008 , the risk manager assumes a sequence of similar negative economic events that would not only increase the PD to 20% of the portfolio but also drastically decrease recovery rates on the loans to 40%. What is the real-estate portfolio's expected loss in the stressed scenarios? A USD 10,800,000 B USD 14,720,000. C USD 25,600,000. D USD 38,400,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuing A Business

Authors: Shannon P. Pratt, Robert F. Reilly, Robert P. Schweihs

4th Edition

0071356150, 978-0071356152