Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need a clear explanation Questions 19 and 20 are based on the following scenario: ABC PLC is entering a four-year single name credit default

I need a clear explanation

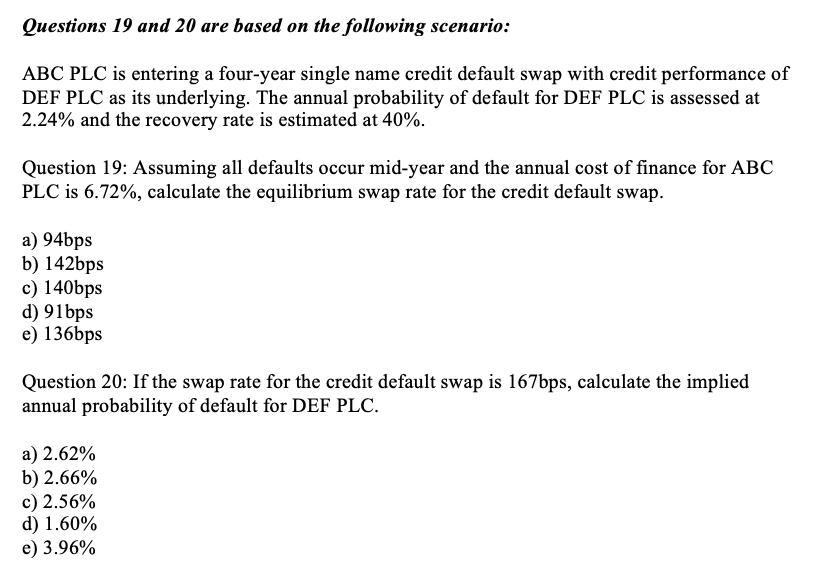

Questions 19 and 20 are based on the following scenario: ABC PLC is entering a four-year single name credit default swap with credit performance of DEF PLC as its underlying. The annual probability of default for DEF PLC is assessed at 2.24% and the recovery rate is estimated at 40%. Question 19: Assuming all defaults occur mid-year and the annual cost of finance for ABC PLC is 6.72%, calculate the equilibrium swap rate for the credit default swap. a) 94bps b) 142bps c) 140bps d) 91bps e) 136bps Question 20: If the swap rate for the credit default swap is 167bps, calculate the implied annual probability of default for DEF PLC. a) 2.62% b) 2.66% c) 2.56% d) 1.60% e) 3.96% Questions 19 and 20 are based on the following scenario: ABC PLC is entering a four-year single name credit default swap with credit performance of DEF PLC as its underlying. The annual probability of default for DEF PLC is assessed at 2.24% and the recovery rate is estimated at 40%. Question 19: Assuming all defaults occur mid-year and the annual cost of finance for ABC PLC is 6.72%, calculate the equilibrium swap rate for the credit default swap. a) 94bps b) 142bps c) 140bps d) 91bps e) 136bps Question 20: If the swap rate for the credit default swap is 167bps, calculate the implied annual probability of default for DEF PLC. a) 2.62% b) 2.66% c) 2.56% d) 1.60% e) 3.96%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options For Volatile Markets Managing Volatility And Protecting Against Catastrophic Risk

Authors: Richard Lehman, Lawrence G. McMillan

2nd Edition

1118022262, 978-1118022269