I need an answer for this question please? Just answer all of the 5 parts A through E please?

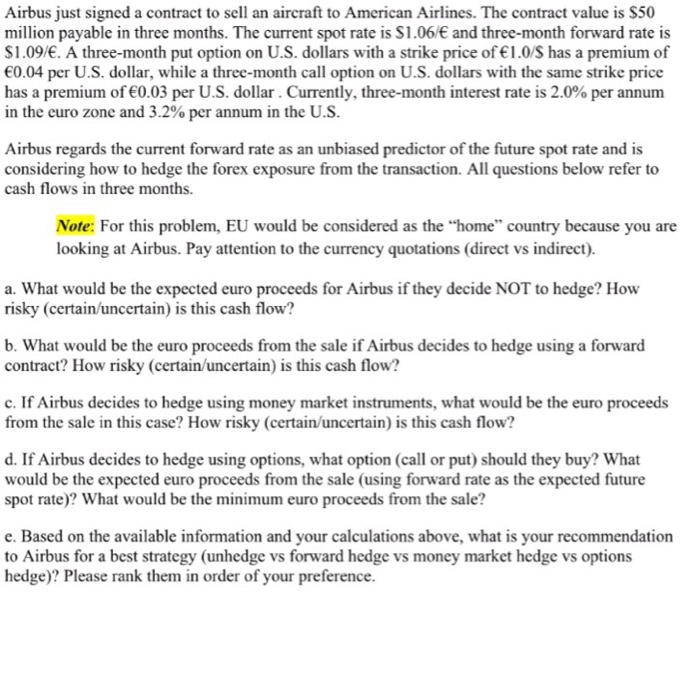

Airbus just signed a contract to sell an aircraft to American Airlines. The contract value is S50 million payable in three months. The current spot rate is S1.06/E and three-month forward rate is S1.09/. A three-month put option on U.S. dollars with a strike price of 1.0/S has a premium of 0.04 per U.S. dollar, while a three-month call option on U.S. dollars with the same strike price has a premium of 0.03 per U.S. dollar. Currently, three-month interest rate is 2.0% per annum in the euro zone and 3.2% per annum in the us Airbus regards the current forward rate as an unbiased predictor of the future spot rate and is considering how to hedge the forex exposure from the transaction. All questions below refer to cash flows in three months. Note: For this problem, EU would be considered as the "home" country because you are looking at Airbus. Pay attention to the currency quotations (direct vs indirect). a. What would be the expected euro proceeds for Airbus if they decide NOT to hedge? How risky (certain/uncertain) is this cash flow? b. What would be the euro proceeds from the sale if Airbus decides to hedge using a forward contract? How risky (certain/uncertain) is this cash flow? c. If Airbus decides to hedge using money market instruments, what would be the euro proceeds from the sale in this case? How risky (certain/uncertain) is this cash flow? d. If Airbus decides to hedge using options, what option (call or put) should they buy? What would be the expected euro proceeds from the sale (using forward rate as the expected future spot rate)? What would be the minimum euro proceeds from the sale? e. Based on the available information and your calculations above, what is your recommendation to Airbus for a best strategy (unhedge vs forward hedge vs money market hedge vs options hedge)? Please rank them in order of your preference Airbus just signed a contract to sell an aircraft to American Airlines. The contract value is S50 million payable in three months. The current spot rate is S1.06/E and three-month forward rate is S1.09/. A three-month put option on U.S. dollars with a strike price of 1.0/S has a premium of 0.04 per U.S. dollar, while a three-month call option on U.S. dollars with the same strike price has a premium of 0.03 per U.S. dollar. Currently, three-month interest rate is 2.0% per annum in the euro zone and 3.2% per annum in the us Airbus regards the current forward rate as an unbiased predictor of the future spot rate and is considering how to hedge the forex exposure from the transaction. All questions below refer to cash flows in three months. Note: For this problem, EU would be considered as the "home" country because you are looking at Airbus. Pay attention to the currency quotations (direct vs indirect). a. What would be the expected euro proceeds for Airbus if they decide NOT to hedge? How risky (certain/uncertain) is this cash flow? b. What would be the euro proceeds from the sale if Airbus decides to hedge using a forward contract? How risky (certain/uncertain) is this cash flow? c. If Airbus decides to hedge using money market instruments, what would be the euro proceeds from the sale in this case? How risky (certain/uncertain) is this cash flow? d. If Airbus decides to hedge using options, what option (call or put) should they buy? What would be the expected euro proceeds from the sale (using forward rate as the expected future spot rate)? What would be the minimum euro proceeds from the sale? e. Based on the available information and your calculations above, what is your recommendation to Airbus for a best strategy (unhedge vs forward hedge vs money market hedge vs options hedge)? Please rank them in order of your preference