Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need an approach to answer question 3 (5-day VaR). I do not understand the difference between a 5-day VaR and and a normal VaR.

I need an approach to answer question 3 (5-day VaR). I do not understand the difference between a 5-day VaR and and a normal VaR. Could you please help me out?

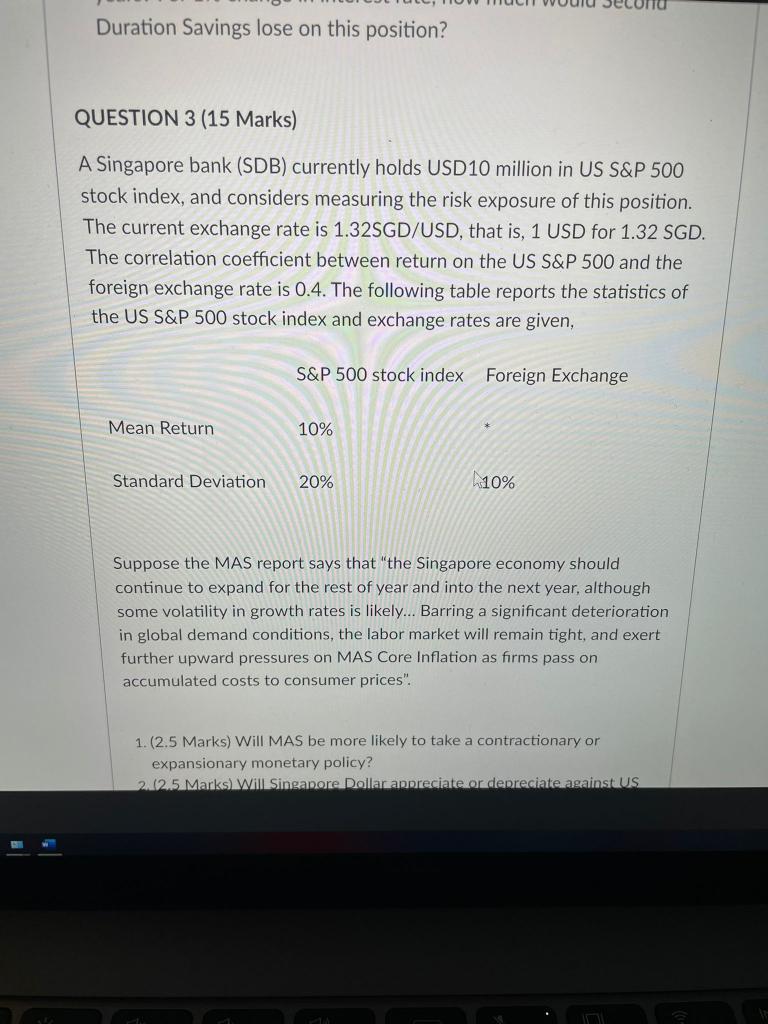

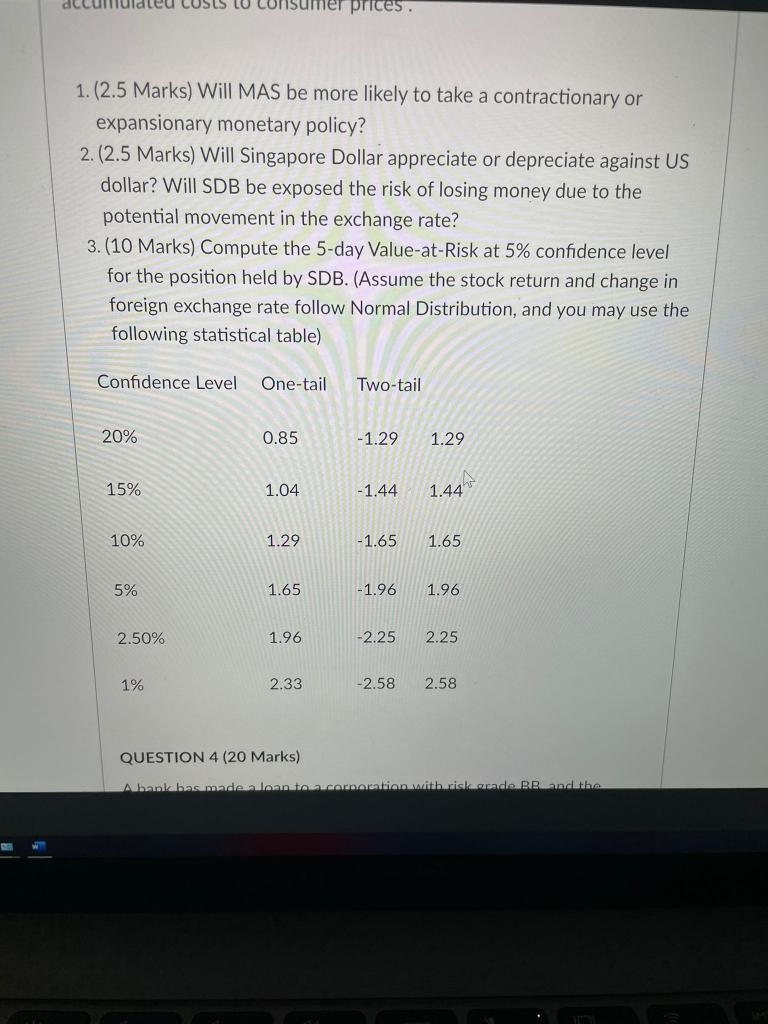

Duration Savings lose on this position? QUESTION 3 (15 Marks) A Singapore bank (SDB) currently holds USD10 million in US S&P 500 stock index, and considers measuring the risk exposure of this position. The current exchange rate is 1.32SGD/USD, that is, 1 USD for 1.32 SGD. The correlation coefficient between return on the US S&P 500 and the foreign exchange rate is 0.4. The following table reports the statistics of the US S&P 500 stock index and exchange rates are given, S&P 500 stock index Foreign Exchange Mean Return 10% Standard Deviation 20% h10% Suppose the MAS report says that "the Singapore economy should continue to expand for the rest of year and into the next year, although some volatility in growth rates is likely... Barring a significant deterioration in global demand conditions, the labor market will remain tight, and exert further upward pressures on MAS Core Inflation as firms pass on accumulated costs to consumer prices". 1.(2.5 Marks) Will MAS be more likely to take a contractionary or expansionary monetary policy? 225 Marks) Will Singapore Dollar appreciate or depreciate against US dce prices. 1. (2.5 Marks) Will MAS be more likely to take a contractionary or expansionary monetary policy? 2. (2.5 Marks) Will Singapore Dollar appreciate or depreciate against US dollar? Will SDB be exposed the risk of losing money due to the potential movement in the exchange rate? 3.(10 Marks) Compute the 5-day Value-at-Risk at 5% confidence level for the position held by SDB.(Assume the stock return and change in foreign exchange rate follow Normal Distribution, and you may use the following statistical table) Confidence Level One-tail Two-tail 20% 0.85 -1.29 1.29 15% 1.04 -1.44 1.44 10% 1.29 -1.65 1.65 5% 1.65 -1.96 1.96 2.50% 1.96 -2.25 2.25 1% 2.33 -2.58 2.58 QUESTION 4 (20 Marks) Albank bas made a loan ton corporation with riskande. RendithaStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Managerial Accounting

Authors: Carl S. Warren, Jefferson P. Jones, William B. Tayler

15th Edition

1337902667, 9781337902663