Answered step by step

Verified Expert Solution

Question

1 Approved Answer

i need detail explaination of how to do this homework please. not the answer but detail math explaination on how to get the answer as

i need detail explaination of how to do this homework please. not the answer but detail math explaination on how to get the answer as soon as possible please thank you

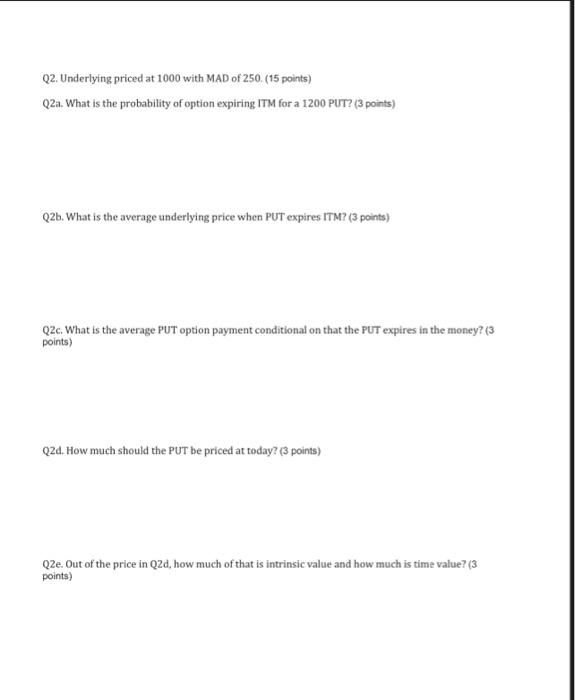

Underlying priced at 1000 with MAD of 250. 1) What is the probability of option expiring ITM for a 1200 PUT?

2)What is the average underlying price when PUT expires ITM?

3)What is the average PUT option payment conditional on that the PUT expires in the money?

4)How much should the PUT be priced at today? 5) Out of the price in Q2d, how much of that is intrinsic value and how much is time value?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Sustainability

Authors: William Sun, Celine Louche, Roland Perez

1st Edition

1780520921, 978-1780520926