Answered step by step

Verified Expert Solution

Question

1 Approved Answer

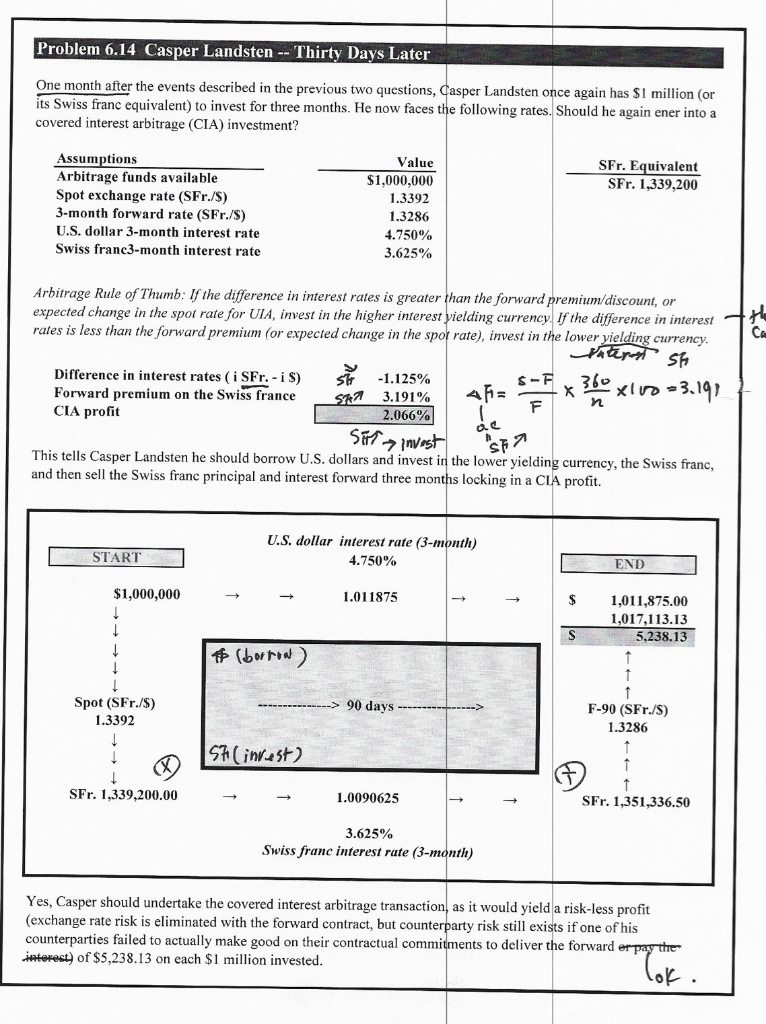

I need explanations Problem 6.14 Casper Landsten -- Thirty Days Later One month after the events described in the previous two questions, Casper Landsten once

I need explanations

Problem 6.14 Casper Landsten -- Thirty Days Later One month after the events described in the previous two questions, Casper Landsten once again has $1 million (or its Swiss franc equivalent) to invest for three months. He now faces the following rates. Should he again ener into a covered interest arbitrage (CIA) investment? SFr. Equivalent SFr. 1,339,200 Assumptions Arbitrage funds available Spot exchange rate (SFr./S) 3-month forward rate (SFr./S) U.S. dollar 3-month interest rate Swiss franc3-month interest rate Value $1,000,000 1.3392 1.3286 4.750% 3.625% Arbitrage Rule of Thumb: If the difference in interest rates is greater than the forward premium/discount, or expected change in the spot rate for UIA, invest in the higher interest yielding currency. If the difference in interest rates is less than the forward premium (or expected change in the spor rate), invest in the lower yielding currency. Interest sh Difference in interest rates ( i SFr. - iS) Forward premium on the Swiss france CIA profit str SRO - 1.125% 3.191% 2.066% 47= SF X 1360x110 -3.192 Sitt invest de "SET This tells Casper Landsten he should borrow U.S. dollars and invest in the lower yielding currency, the Swiss franc, and then sell the Swiss franc principal and interest forward three months locking in a CIA profit. U.S. dollar interest rate (3-month) 4.750% START END $1,000,000 1.011875 $ 1,011,875.00 1,017,113.13 5,238.13 S # (borroa) 1 Spot (SFr./S) 1.3392 90 days F-90 (SFr./S) 1.3286 Shinrest) SFr. 1,339,200.00 1.0090625 1 SFr. 1,351,336.50 3.625% Swiss franc interest rate (3-month) Yes, Casper should undertake the covered interest arbitrage transaction, as it would yield a risk-less profit (exchange rate risk is eliminated with the forward contract, but counterparty risk still exists if one of his counterparties failed to actually make good on their contractual commitments to deliver the forward er pay the interest) of $5,238.13 on each $1 million invested. no one Problem 6.14 Casper Landsten -- Thirty Days Later One month after the events described in the previous two questions, Casper Landsten once again has $1 million (or its Swiss franc equivalent) to invest for three months. He now faces the following rates. Should he again ener into a covered interest arbitrage (CIA) investment? SFr. Equivalent SFr. 1,339,200 Assumptions Arbitrage funds available Spot exchange rate (SFr./S) 3-month forward rate (SFr./S) U.S. dollar 3-month interest rate Swiss franc3-month interest rate Value $1,000,000 1.3392 1.3286 4.750% 3.625% Arbitrage Rule of Thumb: If the difference in interest rates is greater than the forward premium/discount, or expected change in the spot rate for UIA, invest in the higher interest yielding currency. If the difference in interest rates is less than the forward premium (or expected change in the spor rate), invest in the lower yielding currency. Interest sh Difference in interest rates ( i SFr. - iS) Forward premium on the Swiss france CIA profit str SRO - 1.125% 3.191% 2.066% 47= SF X 1360x110 -3.192 Sitt invest de "SET This tells Casper Landsten he should borrow U.S. dollars and invest in the lower yielding currency, the Swiss franc, and then sell the Swiss franc principal and interest forward three months locking in a CIA profit. U.S. dollar interest rate (3-month) 4.750% START END $1,000,000 1.011875 $ 1,011,875.00 1,017,113.13 5,238.13 S # (borroa) 1 Spot (SFr./S) 1.3392 90 days F-90 (SFr./S) 1.3286 Shinrest) SFr. 1,339,200.00 1.0090625 1 SFr. 1,351,336.50 3.625% Swiss franc interest rate (3-month) Yes, Casper should undertake the covered interest arbitrage transaction, as it would yield a risk-less profit (exchange rate risk is eliminated with the forward contract, but counterparty risk still exists if one of his counterparties failed to actually make good on their contractual commitments to deliver the forward er pay the interest) of $5,238.13 on each $1 million invested. no oneStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Industrializing Financial Services With DevOps

Authors: Spyridon Maniotis

1st Edition

1804614343, 978-1804614341