Question

I need help answering these questions 1. The need help with finance with the calculate the grants receivable turnover ratio and the average grant collection

I need help answering these questions

1. The need help with finance with the calculate the grants receivable turnover ratio and the average grant collection for the year 2000 to 1999

Grants receivable turnover is equal to the total grant revenue/grants receivable

The average grant collection period is equal to 365 / grants receivable turnover

2. Is there a trend in grants receivable turnover favorable or unfavorable and why?

3. Are the values of the average grant collection period warrant concern over the collection procedures of the grants?

4. How much cash borrowed in 2000?

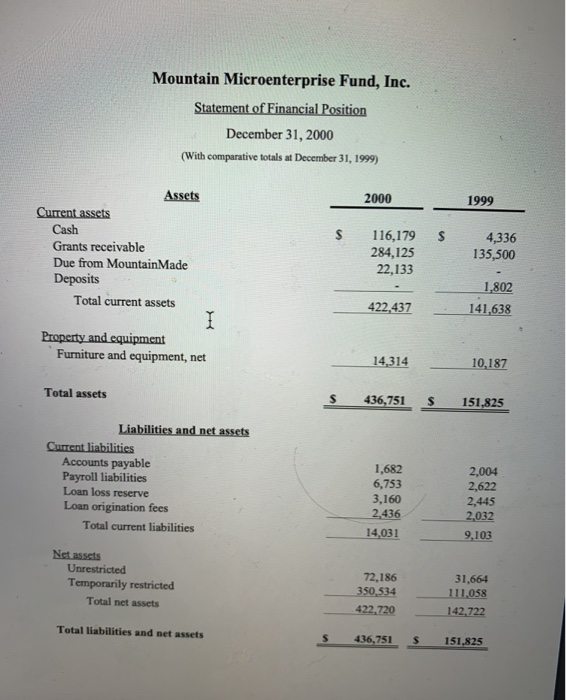

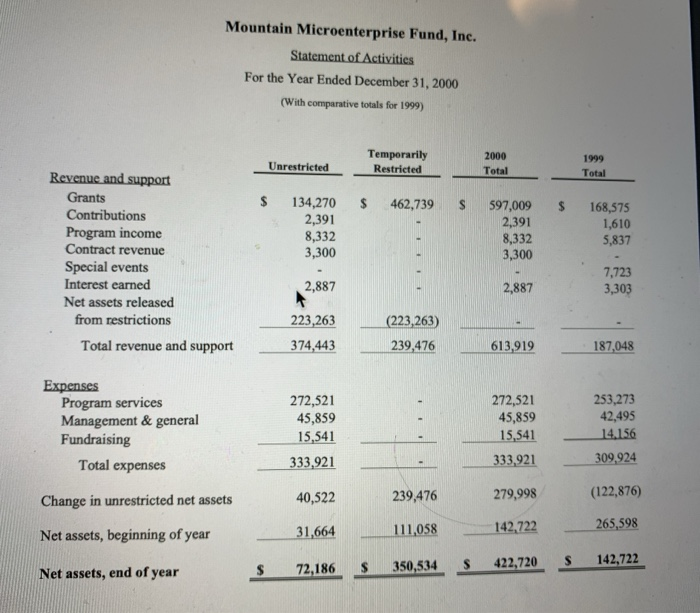

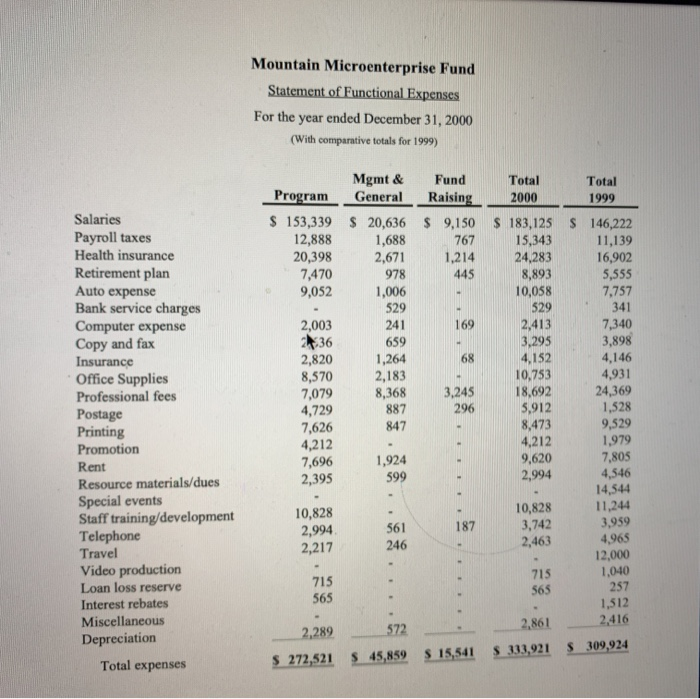

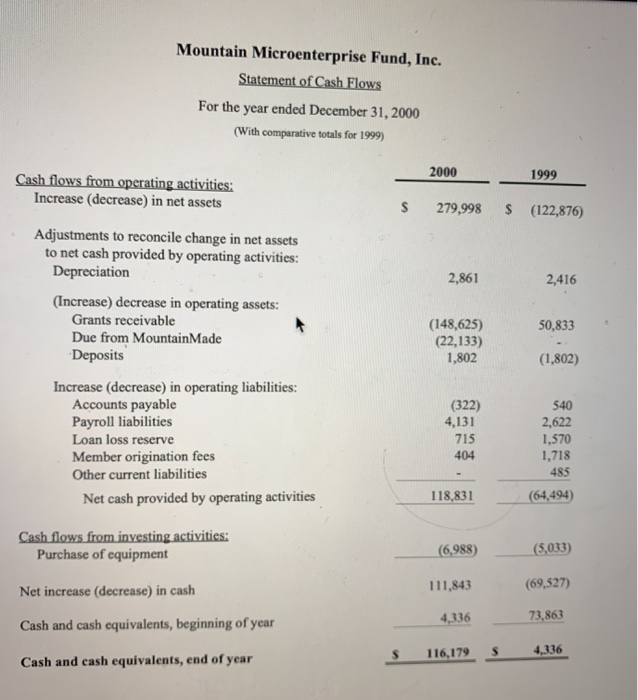

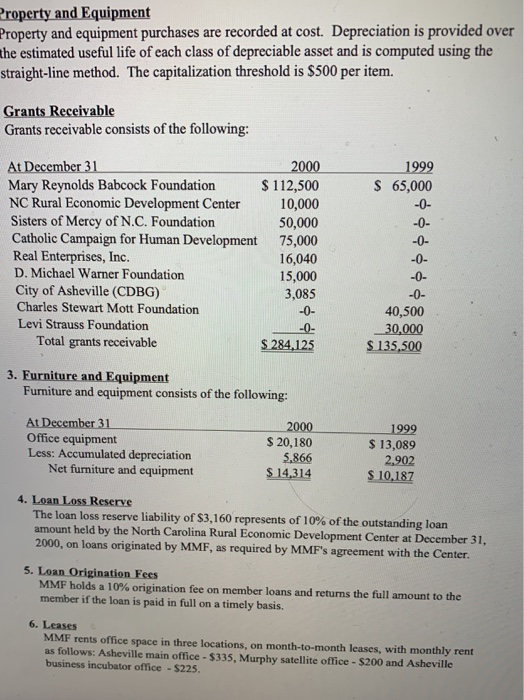

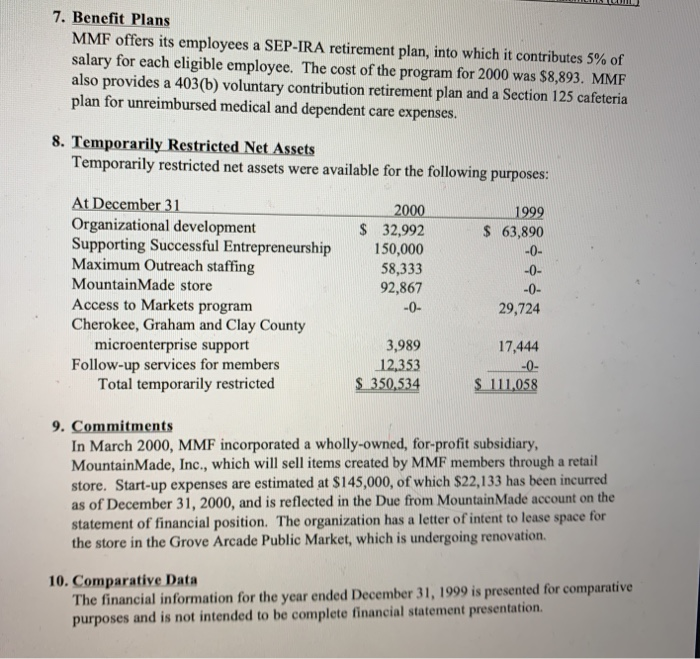

Mountain Microenterprise Fund, Inc. Statement of Financial Position December 31, 2000 (With comparative totals at December 31, 1999) 2000 1999 $ $ Assets Current assets Cash Grants receivable Due from Mountain Made Deposits Total current assets 116,179 284,125 22,133 4,336 135,500 1,802 141,638 422,437 Property and equipment Furniture and equipment, net 14,314 10,187 Total assets 436,751 $ 151,825 Liabilities and net assets Current liabilities Accounts payable Payroll liabilities Loan loss reserve Loan origination fees Total current liabilities 1,682 6,753 3,160 2,436 14,031 2,004 2,622 2,445 2,032 9,103 Net assets Unrestricted Temporarily restricted Total net assets 72,186 350,534 422.720 31,664 111,058 142,722 Total liabilities and net assets 436,751 S 151,825 Mountain Microenterprise Fund, Inc. Statement of Activities For the Year Ended December 31, 2000 (With comparative totals for 1999) Unrestricted Temporarily Restricted 2000 Total 1999 Total $ $ 462,739 S $ 134,270 2,391 8,332 3,300 597,009 2,391 8,332 3,300 168,575 1,610 5,837 Revenue and support Grants Contributions Program income Contract revenue Special events Interest earned Net assets released from restrictions Total revenue and support 2,887 2,887 7,723 3,303 223,263 (223,263) 374,443 239,476 613,919 187,048 Expenses Program services Management & general Fundraising Total expenses 272,521 45,859 15,541 333,921 272,521 45,859 15,541 333.921 253,273 42,495 14.156 309,924 Change in unrestricted net assets 40,522 239,476 (122,876) 279,998 31,664 111,058 142,722 Net assets, beginning of year 265,598 $ Net assets, end of year 72,186 $ 350,534 $ 422,720 S 142,722 Mountain Microenterprise Fund Statement of Functional Expenses For the year ended December 31, 2000 (With comparative totals for 1999) Total 1999 Fund Raising $ 9,150 767 1,214 445 Program $ 153,339 12,888 20,398 7,470 9,052 $ Total 2000 $ 183,125 15,343 24,283 8,893 10,058 Mgmt & General $ 20,636 1,688 2,671 978 1,006 529 241 659 1,264 2,183 8,368 887 847 529 2,003 2:36 2,820 8,570 7,079 146,222 11,139 16,902 5,555 7,757 341 7,340 3,898 4,146 4,931 24,369 1,528 9,529 3,245 2,413 3,295 4,152 10,753 18,692 5,912 8,473 4,212 9,620 Salaries Payroll taxes Health insurance Retirement plan Auto expense Bank service charges Computer expense Copy and fax Insurance Office Supplies Professional fees Postage Printing Promotion Rent Resource materials/dues Special events Staff training/development Telephone Travel Video production Loan loss reserve Interest rebates Miscellaneous Depreciation Total expenses 4,729 1,979 7,626 4,212 7,696 2,395 7,805 1,924 599 2,994 4,546 14,544 10,828 3,742 2,463 11,244 3,959 10,828 2,994 2,217 4,965 12,000 1,040 715 565 715 565 257 2,289 $ 272,521 2,861 S 333,921 1,512 2,416 $ 309,924 $ 45,859 S 15,541 Mountain Microenterprise Fund, Inc. Statement of Cash Flows For the year ended December 31, 2000 (With comparative totals for 1999) 2000 1999 Cash flows from operating activities: Increase (decrease) in net assets $ 279,998 $ (122,876) Adjustments to reconcile change in net assets to net cash provided by operating activities: Depreciation 2,861 2,416 (Increase) decrease in operating assets: Grants receivable Due from MountainMade Deposits 50,833 (148,625) (22,133) 1,802 (1,802) Increase (decrease) in operating liabilities: Accounts payable Payroll liabilities Loan loss reserve Member origination fees Other current liabilities Net cash provided by operating activities (322) 4,131 715 404 540 2,622 1,570 1,718 485 (64,494) 118,831 Cash flows from investing activities: Purchase of equipment (6,988) (5,033) Net increase (decrease) in cash 111,843 (69,527) Cash and cash equivalents, beginning of year 73,863 4,336 116,179 S 4,336 Cash and cash equivalents, end of year Mountain Microenterprise Fund, Ine. Notes to Financial Statements For the Year Ended December 31, 2000 1. Description of Organization and Summary of Significant Accounting Policies Description of the Organization Mountain Microenterprise Fund (MMF) is a nonprofit organization that provides people throughout Western North Carolina with business training, loans, technical assistance and support for starting or expanding a small business. Loans made available to members through MMF's Peer Group Lending Program, are funded by the Microenterprise Loan Program of the North Carolina Rural Economic Development Center. Tax-Exempt Status MMF was established in 1991 as a nonprofit corporation under the laws of the State of North Carolina. It qualifies for exemption from federal income taxes under section 501(c)(3) of the Internal Revenue Code. In addition, it has been classified as a publicly supported organization under Section 509(a)(1). Basis of Accounting and Presentation The accompanying basic financial statements have been prepared on the accrual basis of accounting and in accordance with the principles contained in the American Institute of Certified Public Accountant's Audit and Accounting Guide, Not-For-Profit Organizations and other pronouncements applicable to not-for-profit organizations. Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the period. Actual results could differ from those estimates. Financial Statement Presentation Financial statement presentation follows Statement of Financial Accounting Standards (SFAS) No 117, "Financial Statements of Not-for-Profit Organizations." SFAS No. 117 establishes standards for external financial reporting by not-for-profit organizations and requires that resources be classified for accounting and reporting purposes into three net asset categories according to externally imposed restrictions. Descriptions of the three net asset classes are as follows: Unrestricted Net Assets--Net assets that are not subject to donor-imposed restrictions and that are available for general operating expenses of the organization. Temporarily Restricted Net Assets--Net assets subject to donor-imposed restrictions as to the purpose and/or time of use. Permanently Restricted Net Assets--Net assets subject to donor-imposed restrictions that they be maintained permanently by the organization. The organization currently has no permanently restricted net assets. Cash and Cash Equivalents For purposes of reporting on the statement of cash flows, the organization considers all unrestricted, highly liquid investments purchased with an initial maturity of three months or less to be cash equivalents. Contributions The organization follows SFAS No. 116, Accounting for Contributions Received and Contributions Made." In accordance with SFAS No. 116, contributions received are recorded as unrestricted, temporarily restricted or permanently restricted support depending on the existence and/or nature of any donor restrictions. As restrictions expire, net assets are reclassified to unrestricted net assets and are reported on the statement of activities as Net assets released from restrictions." Grants Receivable A foundation's unconditional promise to make a grant to the organization at some point in the future is recognized as grant revenue and receivable when the grant is awarded. Multi-year grants are recognized in full when awarded to the organization, with amounts restricted to use in future years considered temporarily restricted. (Because grant revenue is generally recognized before the grant-related expenses, multi-year grants may cause large fluctuations in the change in net assets from year to year.) Functional Allocation of Expenses The organization reports its expenses in the functional areas of Program, Management and General and Fund Raising. Expenses that can be identified with a specific area are assigned directly to that area. Other expenses that are common to two or more functions are allocated by management estimate. Income Taxes MMF is a not-for-profit corporation and has been recognized as tax-exempt pursuant to Section 501(C)(3) of the Internal Revenue Code. Accordingly, no provision has been made for income taxes in the financial statements. LUI 7. Benefit Plans MMF offers its employees a SEP-IRA retirement plan, into which it contributes 5% of salary for each eligible employee. The cost of the program for 2000 was $8,893. MMF also provides a 403(b) voluntary contribution retirement plan and a Section 125 cafeteria plan for unreimbursed medical and dependent care expenses. 8. Temporarily Restricted Net Assets Temporarily restricted net assets were available for the following purposes: $ 1999 $ 63,890 At December 31 Organizational development Supporting Successful Entrepreneurship Maximum Outreach staffing MountainMade store Access to Markets program Cherokee, Graham and Clay County microenterprise support Follow-up services for members Total temporarily restricted 2000 32,992 150,000 58,333 92,867 -O- 29,724 17,444 3,989 12,353 $ 350,534 -0- $ 111,058 9. Commitments In March 2000, MMF incorporated a wholly-owned, for-profit subsidiary, Mountain Made, Inc., which will sell items created by MMF members through a retail store. Start-up expenses are estimated at $145,000, of which $22,133 has been incurred as of December 31, 2000, and is reflected in the Due from Mountain Made account on the statement of financial position. The organization has a letter of intent to lease space for the store in the Grove Arcade Public Market, which is undergoing renovation. 10. Comparative Data The financial information for the year ended December 31, 1999 is presented for comparative purposes and is not intended to be complete financial statement presentation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Accounting A User Perspective

Authors: Suadagaran, Shahrokh M, Smith Lawrence Murphy

5th Edition

1531018661, 9781531018665