Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need help to solve it. Also, I need the answer in excel doc with question you use. thanks Consider an A-rated bond maturing in

I need help to solve it. Also, I need the answer in excel doc with question you use. thanks

Step by Step Solution

There are 3 Steps involved in it

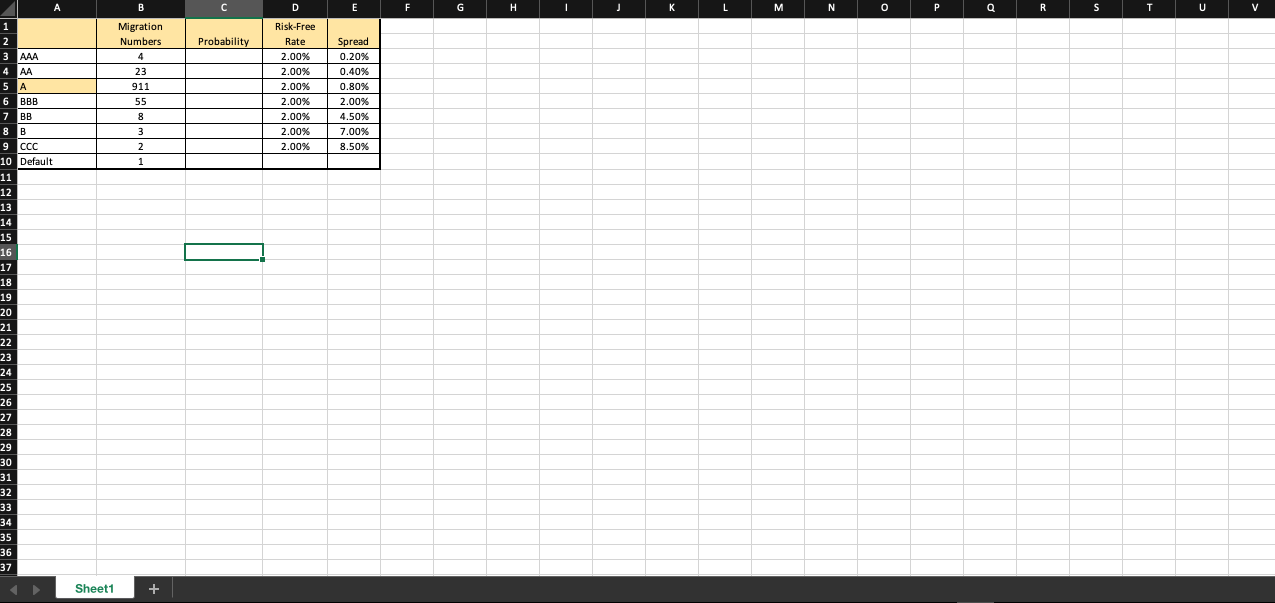

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultimate Guide To Frugal Living Save Money Plan Ahead Pay Off Debt And Live Well

Authors: Daisy Luther

1st Edition

1631586009, 978-1631586002