Answered step by step

Verified Expert Solution

Question

1 Approved Answer

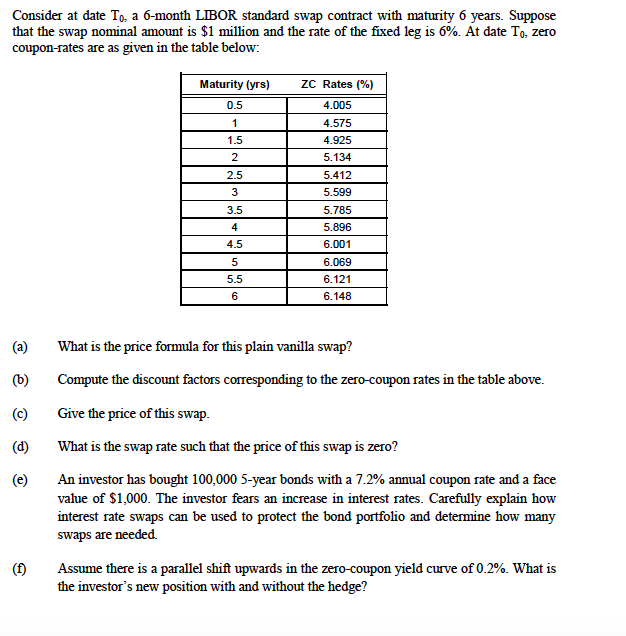

I need help with solving only the last two questions! How should I solve (e) and (f)? Consider at date T_0, a 6-month LIBOR standard

I need help with solving only the last two questions!

How should I solve (e) and (f)?

Consider at date T_0, a 6-month LIBOR standard swap contract with maturity 6 years. Suppose that the swap nominal amount is $1 million and the rate of the fixed leg is 6%. At date T_0, zero coupon-rates are as given in the table below: (a) What is the price formula for this plain vanilla swap? (b) Compute the discount factors corresponding to the zero-coupon rates in the table above. (c) Give the price of this swap. (d) What is the swap rate such that the price of this swap is zero? (e) An investor has bought 100,000 5-year bonds with a 7.2% annual coupon rate and a face value of $1,000. The investor fears an increase in interest rates. Carefully explain how interest rate swaps can be used to protect the bond portfolio and determine how many swaps are needed. (f) Assume there is a parallel shift upwards in the zero-coupon yield curve of 0.2%. What is the investor's new position with and without the hedge

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John C. Hull

11th Edition

013693997X, 9780136939979