Question

I need help with the following question. I have computed the calculations to determine that x1 = 52.5, x2 = -5, and x3 = 27.5.

I need help with the following question. I have computed the calculations to determine that x1 = 52.5, x2 = -5, and x3 = 27.5. I have pasted my work below. What I can't figure out is how to rescale these weights so they equal 1. Can anyone show me how to rescale?

0.002 x1 + 0.001 x2 + 0x3 = 15% - 5%

0.001 x1 + 0.002 x2 + 0.001 x3 = 12% - 5%

0.000 x1 + 0.001 x2 + 0.002 x3 = 10% - 5%

-----------------------------------------------------

0.002 x1 + 0.001 x2 + x3 = 15% - 5%

0.002 x1 + 0.001 x2 = 10%

x1 + x2/2 = 50

x1 = 50 - x2/2

-------------------------------------------------

0.000 x1 + 0.001 x2 + 0.002 x3 = 10% - 5%

0.001 x2 + 0.002 x3 = 5%

x2/2 + x3 = 25

x3 = 25 - x2/2

-------------------------------------------------------------

0.001 x1 + 0.002 x2 + 0.001 x3 = 12% - 5%

0.001 (50 - x2/2) + 0.002 x2 + 0.001 (25 - x2/2) = 7%

(50 - x2/2) + 2 x2 + (25 - x2/2) = 7%/0.001

(100 - x2)/2 + 2 x2 + (50 - x2)/2 = 70

100 - x2 + 4x2 + 50 - x2 = 140

2 x2 = 140 - 150

x2 = -5

--------------------------------

x1 = 50 - x2/2

x1 = 50 - (-5)/2

x1 = 52.5

---------------------------------

x3 = 25 - x2/2

x3 = 25 - (-5)/2

x3 = 27.5

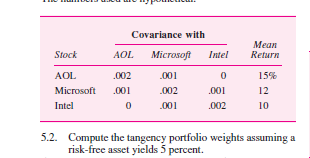

Covariance with Stock AOL Microsoft Intel Mean Return 15% AOL Microsoft Intel .002 .001 0 .001 .002 .001 0 .001 .002 12 10 5.2. Compute the tangency portfolio weights assuming a risk-free asset yields 5 percentStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles And Applications

Authors: Dr. S. Kr. Paul, Prof. Chandrani Paul

1st Edition

1647251664, 9781647251666