Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need help with the steps to fo this with vba as well as the solutions so I'll know I did it right. Thanks Experiment

I need help with the steps to fo this with vba as well as the solutions so I'll know I did it right. Thanks

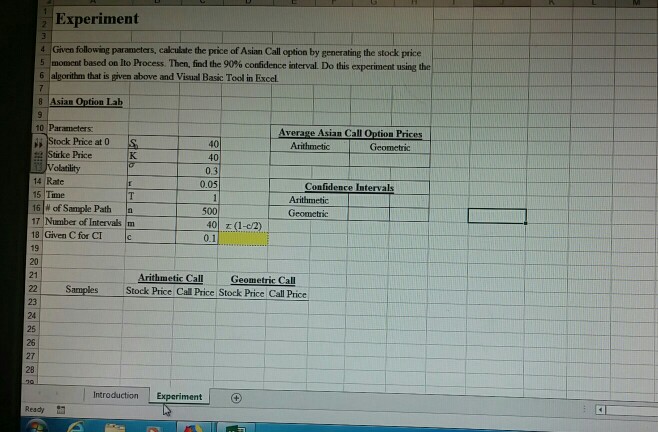

Experiment 4 Given following parameters, calculate the price of Asian Call option by generating the stock price 6 algorithm that is given above and Visual Basic Tool in Excel. 8 Asian Option Lab 0 Parameters Stirke Price based on Ito process Then, find the 90% confidence interval Do this experiment using the Stock Price at 0 40 40 Geometrio Volatility 14 Rate 15 Time 0.3 0.05 Confidence Intervals Arithmetic 16 W of Sample Patha 17 Number of Intervals 500 40 (1-c/2) 18 Given C for CIc01 19 20 21 Arithmetic Call 22 Samples Stock Price Call Price Stock Price Call Price Geometric Call 23 24 25 26 27 28 IntroductionExperiment Ready Experiment 4 Given following parameters, calculate the price of Asian Call option by generating the stock price 6 algorithm that is given above and Visual Basic Tool in Excel. 8 Asian Option Lab 0 Parameters Stirke Price based on Ito process Then, find the 90% confidence interval Do this experiment using the Stock Price at 0 40 40 Geometrio Volatility 14 Rate 15 Time 0.3 0.05 Confidence Intervals Arithmetic 16 W of Sample Patha 17 Number of Intervals 500 40 (1-c/2) 18 Given C for CIc01 19 20 21 Arithmetic Call 22 Samples Stock Price Call Price Stock Price Call Price Geometric Call 23 24 25 26 27 28 IntroductionExperiment ReadyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Learning PostgreSQL

Authors: Salahaldin Juba, Achim Vannahme, Andrey Volkov

1st Edition

178398919X, 9781783989195