I need solutions and I would like it to be organize as possible

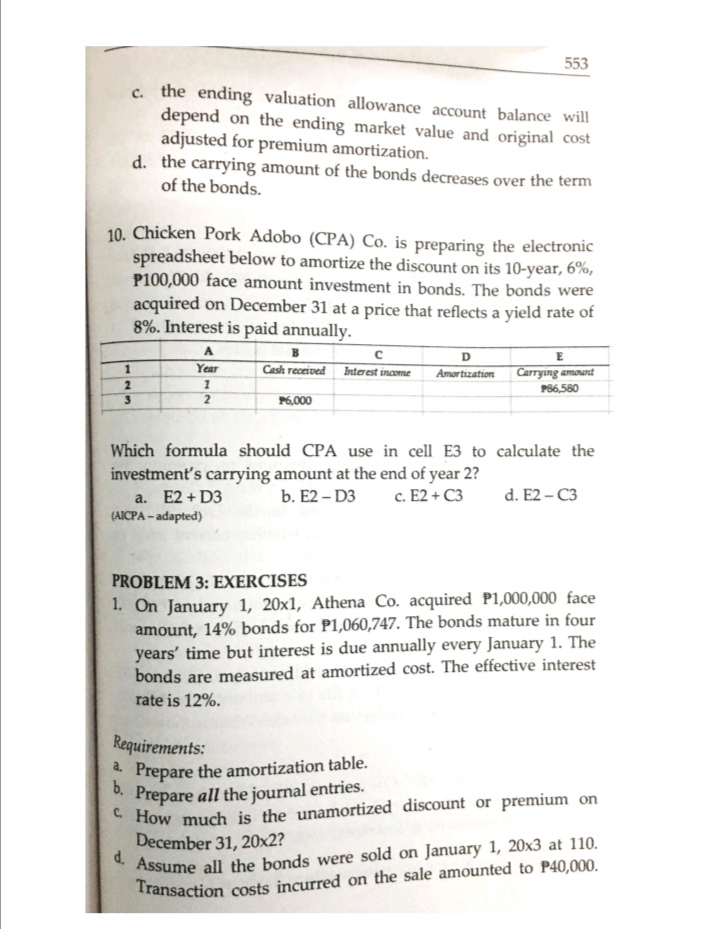

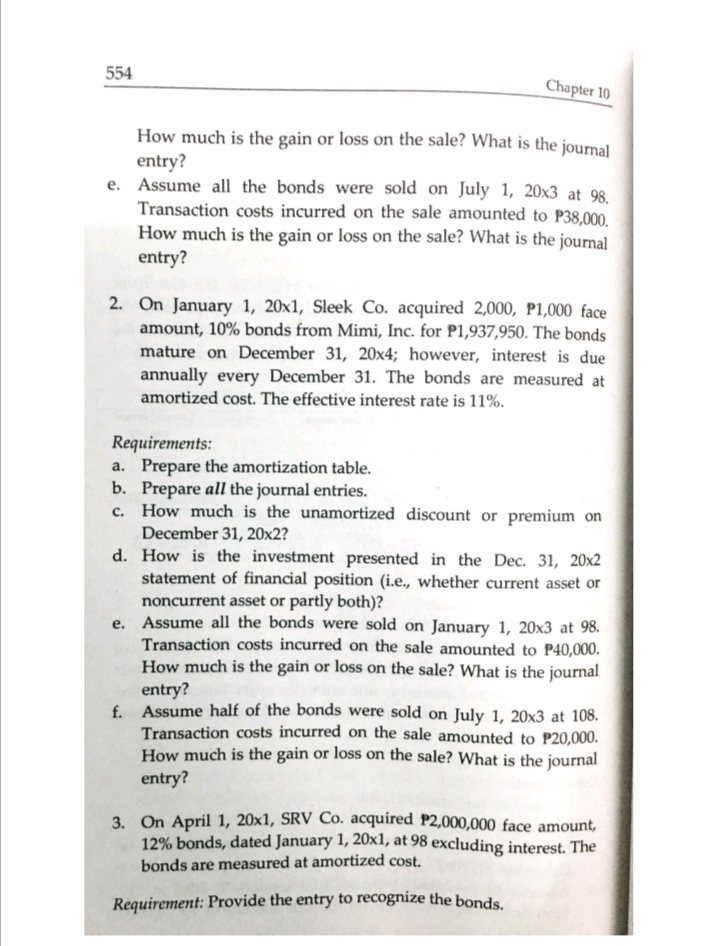

Basic Derivatives 687 to make Cougar's interest payment in 2003 and Cougar likewise agrees to make Aggie's interest payment in 2003. The two companies agree to make settlement payments, for the difference only, on December 31, 2003. 13. If the interest rate on January 1, 2003 is 8 percent, what will be Cougar's settlement payment to/from Aggie? a. $5,000 payment c. $10,000 payment b. $5,000 receipt d. $10,000 receipt (Adapted) 14. If the interest rate on January 1, 2003, is 12 percent, what will be Cougar's settlement payment to/from Aggie? a. $5,000 payment c. $10,000 payment b. $5,000 receipt d. $10,000 receipt (Adapted) 15. If the interest rate on December 31, 2002 is 12 percent, what amount will Cougar report as the fair value of the interest rate swap at December 31, 2002? a. $0 b. $8,929 c. $10,000 d. $500,000 (Adapted)550 Chapter 10 PROBLEMS PROBLEM 1: TRUE OR FALSE 1. According to PFRS 9, amortized cost financial assets are initially measured at fair value. 2. Investments in ordinary shares can be classified as financial assets measured at amortized cost. 3. Subsequent changes in the fair value of a financial asset measured at amortized cost are normally ignored. 4. Investments in preference shares with mandatory redemption can be classified as financial assets measured at amortized cost. 5. Entity A acquired bonds with face amount of PIM for P976,231. The effective interest rate on the bonds must be lower than the stated rate. 6. The amortized cost of an investment in term bonds that is acquired at a discount decreases each year. 7. Whether an investment in debt securities is measured at amortized cost or FVOCI, the total effect of the investment in profit or loss would be the same. 8. Entity B acquired bonds at a discount and classified them as FVOCI. The amount of interest income for the period would be higher if the bonds were classified as amortized cost asset. 9. Discount or premium amortization is unnecessary if investments in bonds are measured at FVOCI. 10. Entity C acquired bonds and classified them as FVOCI. Subsequently, the bonds were sold at P100. The bonds were reported at a fair value of P90 in the latest annual financial statements. The bonds have an amortized cost of P80 as at the date of sale. Entity C would probably recognize a gain of P20 in profit or loss at the date of sale.ACTIVITY 1 PROBLEM 2: MULTIPLE CHOICE - THEORY 1. According to PFRS 9, the amortized cost of a financial instrument is calculated using a. the effective interest method. b. the straight line method. c. (a) or (b) d. Choice (a); however, the straight line method can be used in some circumstances. 2 The amortization of a discount on an investment in bonds measured at amortized cost a. increases the carrying amount of the investment. b. is the excess of interest income over interest received or receivable. c. is recorded directly to the investment account. d. all of these 3. Which of the following statements is correct for an investment in term bonds that was acquired at a premium? a. The amortized cost of the bonds increases annually. b. The current and noncurrent portions of the bonds as of the reporting date are reported separately. c. The interest income recognized each year is higher than the amount of interest received/receivable. d. The effective interest rate is lower than the stated rate of the bonds. The rate used in computing for interest receivable on debt instruments measured at amortized cost is the a. nominal rate. c. yield rate. b. effective interest rate. d. celeb rate. 5. The transaction costs of acquiring an investment measured at amortized cost are a. included in the initial measurement of the investment and amortized to profit or loss using the effective interest method. b. initially deferred and recognized in profit or loss only when the asset is derecognized or becomes impaired.552 Chapter 10 C. initially deferred and recognized directly in equity when the asset is derecognized or becomes impaired. d. expensed immediately on acquisition date. 6. An entity acquired 10-year bonds at a premium. The investment is measured at amortized cost. Seven years after the acquisition, the entity sold 90% of the bonds at a discount. Which of the following is true? a. Gain is realized on the sale. b. The remaining 10% should be reclassified out of the amortized cost measurement category. c. Loss is realized on the sale d. band c 7. There are no payments made during the life of this type of bond; both the principal and interest (computed on a compounded basis) are payable only at maturity date. a. zero coupon or strip bonds b. no sufficient funds bonds c. junk bond d. retractable bond 8. Jackhammer Co. calculates the interest income on an investment in debt securities using the effective interest method but reports the investment at fair value. Jackhammer Co.'s investment must have been classified as a. amortized cost asset. b. FVPL asset. c. FVOCI asset. d. fair value asset. 9. An entity purchased bonds at a premium. The bonds are measured at amortized cost. Assume the fair value of the bonds is volatile. Therefore, a. less cash interest is received each year than interest revenue. b. the ending valuation allowance account balance will depend on the ending market value and original cost.553 c. the ending valuation allowance account balance will depend on the ending market value and original cost adjusted for premium amortization. d. the carrying amount of the bonds decreases over the term of the bonds. 10. Chicken Pork Adobo (CPA) Co. is preparing the electronic spreadsheet below to amortize the discount on its 10-year, 6%, P100,000 face amount investment in bonds. The bonds were acquired on December 31 at a price that reflects a yield rate of 8%. Interest is paid annually. A C E Year Cash received Interest income Amortization Carrying amount P86,580 P6,000 Which formula should CPA use in cell E3 to calculate the investment's carrying amount at the end of year 2? a. E2 + D3 b. E2 - D3 c. E2 + C3 d. E2 - C3 (AICPA - adapted) PROBLEM 3: EXERCISES 1. On January 1, 20x1, Athena Co. acquired P1,000,000 face amount, 14% bonds for P1,060,747. The bonds mature in four years' time but interest is due annually every January 1. The bonds are measured at amortized cost. The effective interest rate is 12%. Requirements: a. Prepare the amortization table. b. Prepare all the journal entries. How much is the unamortized discount or premium on December 31, 20x2? . Assume all the bonds were sold on January 1, 20x3 at 110. Transaction costs incurred on the sale amounted to P40,000.554 Chapter 10 How much is the gain or loss on the sale? What is the journal entry? e. Assume all the bonds were sold on July 1, 20x3 at 98. Transaction costs incurred on the sale amounted to P38,000. How much is the gain or loss on the sale? What is the journal entry? 2. On January 1, 20x1, Sleek Co. acquired 2,000, P1,000 face amount, 10% bonds from Mimi, Inc. for P1,937,950. The bonds mature on December 31, 20x4; however, interest is due annually every December 31. The bonds are measured at amortized cost. The effective interest rate is 11%. Requirements: a. Prepare the amortization table. b. Prepare all the journal entries. c. How much is the unamortized discount or premium on December 31, 20x2? d. How is the investment presented in the Dec. 31, 20x2 statement of financial position (i.e., whether current asset or noncurrent asset or partly both)? e. Assume all the bonds were sold on January 1, 20x3 at 98. Transaction costs incurred on the sale amounted to P40,000. How much is the gain or loss on the sale? What is the journal entry? f. Assume half of the bonds were sold on July 1, 20x3 at 108. Transaction costs incurred on the sale amounted to P20,000. How much is the gain or loss on the sale? What is the journal entry? 3. On April 1, 20x1, SRV Co. acquired P2,000,000 face amount, 12% bonds, dated January 1, 20x1, at 98 excluding interest. The bonds are measured at amortized cost. Requirement: Provide the entry to recognize the bonds.Investments in Debt Securities 555 On Jan. 1, 20x1, Coal Plant Co. purchased P4,000,000, 12% bonds for P4,166,027. The bonds mature in four equal annual installments, plus interest on the outstanding principal balance, every Dec. 31. The bonds are measured at amortized cost. The effective interest rate is 10%. Requirements: a. Provide the journal entries. b. Determine the current and noncurrent portions of the investment on Dec. 31, 20x1. 5. On Jan. 1, 20x1, Steamed Rooster Co. acquired P100,000 face value, 10% bonds for P94,738. The bonds, together with accrued interests, are due on Dec. 31, 20x3. The bonds are measured at amortized cost. The effective interest rate is 12%. Requirements: a. How much are the carrying amounts of the interest receivable on Dec. 31, 20x1 and Dec. 20x2, respectively? b. How much are the carrying amounts of the investment on Dec. 31, 20x1 and Dec. 20x2, respectively? c. Prepare all the journal entries. 6. On Jan. 1, 20x1, White Co. acquired P1,000,000 face amount, 10% bonds of Beans Co. for P907,135. The bonds mature on Dec. 31, 20x3 and pay annual interest every Dec. 31. The effective interest rate is 14%. The bonds are to be held under a "hold to collect and sell" business model. Information on fair values is as follows: December 31, 20x1.. ...98 December 31, 20x2. White Co. sold all the bonds on Jan. 1, 20x3 at 101. Requirement: Prepare all the journal entries.ACTIVITY 2 556 Chapter 10 PROBLEM 4: MULTIPLE CHOICE - COMPUTATIONAL 1. On July 1, 2003, York Co. purchased, as investment measured at amortized cost, P1,000,000 of Park, Inc.'s 8% bonds for P946,000, including accrued interest of P40,000. The bonds were purchased to yield 10% interest. The bonds mature on January 1, 2010, and pay interest annually on January 1. York uses the effective interest method of amortization. In its December 31, 2003 balance sheet, what amount should York report as investment in bonds? a. 911,300 b. 916,600 c. 953,300 d. 960,600 (AICPA) Use the following information for the next three questions: On Jan. 1, 20x1, Koong Co. acquired 100, P5,000 face amount, 10%, 3-year 'term' bonds of King Co. for P428,567. Koong incurred transaction costs of P25,000 on the acquisition. The effective interest rate adjusted for the transaction costs is 14%. The bonds were quoted at 102 on Dec. 31, 20x2. 2. How much are the interest income in 20x2 and the carrying amount of the bonds on Dec. 31, 20x2 if the bonds are held under a "hold to collect" business model? a. 65,389; 482,455 c. 55,276; 472,834 b. 65,389; 510,000 d. 50,000; 453,567 3. How much are the interest income in 20x2 and the carrying amount of the bonds on Dec. 31, 20x2 if the bonds are held under a "hold to collect and sell" business model? a. 65,389; 482,455 c. 50,000; 428,567 b. 65,389; 510,000 d. 50,000; 510,000 4. What amount of gain (loss) is recognized if the bonds were sold on Jan. 3, 20x3 at 102, transaction costs of P15,000 were incurred on the sale, and the bonds were classified as: Amortized cost FVOCI Amortized cost c. 12,545 FVOCI a. 12,545 (15,000) 0Ivestments in Debt Securities 557 b. 12,545 12,545 d. 16,315 (15,000) 5. On July 1, 2003, East Co. purchased, as a long-term investment, P500,000 face amount, 8% bonds of Rand Corp. for p461,500 to yield 10% per year. The bonds pay interest semiannually on January 1 and July 1. In its December 31, 2003 balance sheet, East should report interest receivable of a. 18,460 b. 20,000 (AICPA) c. 23,075 d. 25,000 6. Cap Corp. reported accrued investment interest receivable of P38,000 and P46,500 at January 1 and December 31, 2003, respectively. During 2003, cash collections from the investments included the following: Capital gains distributions 145,000 Interest 152,000 What amount should Cap report as interest revenue from investments for 2003? a. 160,500 b. 153,500 c. 152,000 d. 143,500 (AICPA) ."A capital gains distribution is a payment by a mutual fund or an exchange-traded fund (ETF) of a portion of the proceeds from the fund's sales of stocks and other assets. It is the investor's share of the proceeds from the fund's transactions. " (www.investopedia.com) " Hint T-account Use the following information for the next four questions: On Jan. 1, 20x1, Red Co. acquires P500,000 face amount, 10%, bonds of Ball Co. for P487,656. Red Co. incurred transaction costs equal to 5% of the face amount of the bonds. The bonds mature on Dec. 31, 20x3 and pay annual interest every Dec. 31. The bonds were quoted at 102 and 104 on Dec. 31, 20x1 and Dec. 31, 20x2, respectively. 7. What is the effective interest rate on the bonds and how much is the difference between the interest received and the interest income recognized in 20x2? a. 9%; 3,861 c. 14%; 5,389558 Chapter 10 b. 11%; 6,392 d. 9%; 4,208 8. How much is the unamortized bond discount or premium on Dec. 31, 20x2 if the bonds were measured at amortized cost? a. 4,587 discount c. 8,795 premium b. 5,129 discount d. 4,587 premium 9. What amounts of fair value gain (loss) is recognized in other comprehensive income (OCI) and in equity in 20x2 if the bonds were measured at FVOCI? OCI Equity OCI Equity a. 15,413 14,208 c. 14,208 15,413 b. 17,899 32,410 d. 1,205 15,413 10. How much is the gain (loss) if half of the bonds were sold on July 1, 20x3 at 103, transaction costs of P7,000 were incurred on the sale, and the bonds were measured at amortized cost? a. (13,147) b. (78,123) C. (25,647) d. (6,541) 11. On Jan. 1, 20x1, Forgiven Co. acquires 1,000, P5,000 face value, 10%, 5-year 'term' bonds for P4,639,522. The bonds are measured at fair value through other comprehensive income. The bonds are quoted at 98 on Dec. 31, 20x1. How much is the interest income and the fair value gain (loss) in 20x1? a. 556,743; 203,735 b. 296,298; (13,772) c. 556,743; 260,478 d. 412,516; 21,354 12. On August 1, 20x1, Lunch Co. acquired P1,000,000, 12% bonds dated January 1, 20x1 at 98 including interest. The bonds mature on December 31, 20x3 but pays semiannual interest every January 1 and July 1. The bonds are measured at investment? amortized cost. How much is the initial measurement of the a. 1,000,000 b. 980,000 c. 970,000 d. 910,000