I need this question anwsered

This is question one it is referring to. I dont need this one to be solved though

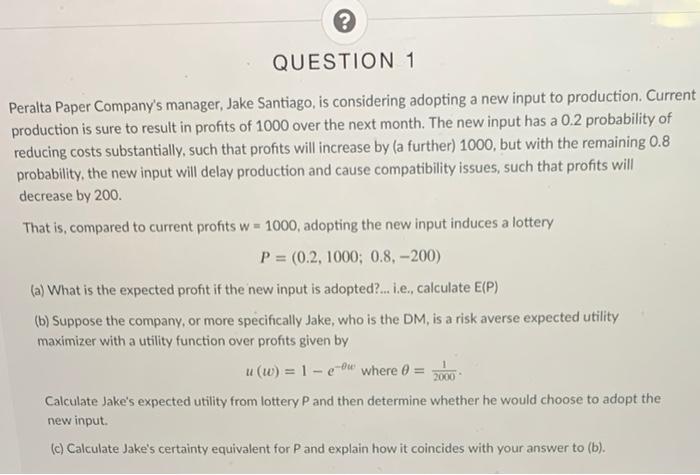

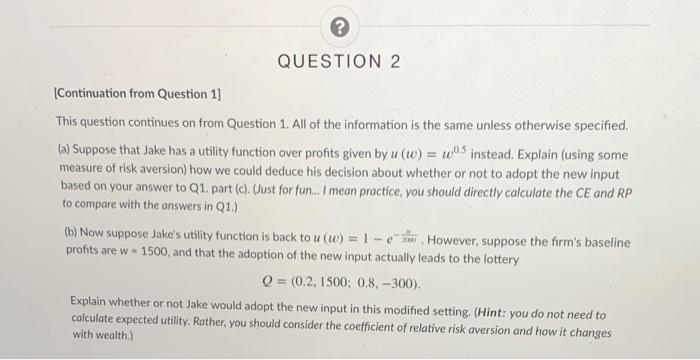

QUESTION 2 (Continuation from Question 1] This question continues on from Question 1. All of the information is the same unless otherwise specified. (a) Suppose that Jake has a utility function over profits given by u (w) = w instead. Explain (using some measure of risk aversion) how we could deduce his decision about whether or not to adopt the new input based on your answer to Q1. part (c). Uust for fun... I mean practice, you should directly calculate the CE and RP to compare with the answers in Q1.) (1) Now suppose Jake's utility function is back to u (w) = 1 - e . However, suppose the firm's baseline profits are w - 1500, and that the adoption of the new input actually leads to the lottery Q = (0.2, 1500; 0.8, -300). Explain whether or not Jake would adopt the new input in this modified setting. (Hint: you do not need to calculate expected utility. Rather, you should consider the coefficient of relative risk aversion and how it changes with wealth.) QUESTION 1 Peralta Paper Company's manager, Jake Santiago, is considering adopting a new input to production. Current production is sure to result in profits of 1000 over the next month. The new input has a 0.2 probability of reducing costs substantially, such that profits will increase by (a further) 1000, but with the remaining 0.8 probability, the new input will delay production and cause compatibility issues, such that profits will decrease by 200 That is compared to current profits w = 1000, adopting the new input induces a lottery P = (0.2, 1000; 0.8. -200) (a) What is the expected profit if the new input is adopted?... i.e., calculate E(P) (b) Suppose the company, or more specifically Jake, who is the DM, is a risk averse expected utility maximizer with a utility function over profits given by u(w) = 1 - e-ow where 0 Calculate Jake's expected utility from lottery P and then determine whether he would choose to adopt the new input. (c) Calculate Jake's certainty equivalent for P and explain how it coincides with your answer to (b). QUESTION 2 (Continuation from Question 1] This question continues on from Question 1. All of the information is the same unless otherwise specified. (a) Suppose that Jake has a utility function over profits given by u (w) = w instead. Explain (using some measure of risk aversion) how we could deduce his decision about whether or not to adopt the new input based on your answer to Q1. part (c). Uust for fun... I mean practice, you should directly calculate the CE and RP to compare with the answers in Q1.) (1) Now suppose Jake's utility function is back to u (w) = 1 - e . However, suppose the firm's baseline profits are w - 1500, and that the adoption of the new input actually leads to the lottery Q = (0.2, 1500; 0.8, -300). Explain whether or not Jake would adopt the new input in this modified setting. (Hint: you do not need to calculate expected utility. Rather, you should consider the coefficient of relative risk aversion and how it changes with wealth.) QUESTION 1 Peralta Paper Company's manager, Jake Santiago, is considering adopting a new input to production. Current production is sure to result in profits of 1000 over the next month. The new input has a 0.2 probability of reducing costs substantially, such that profits will increase by (a further) 1000, but with the remaining 0.8 probability, the new input will delay production and cause compatibility issues, such that profits will decrease by 200 That is compared to current profits w = 1000, adopting the new input induces a lottery P = (0.2, 1000; 0.8. -200) (a) What is the expected profit if the new input is adopted?... i.e., calculate E(P) (b) Suppose the company, or more specifically Jake, who is the DM, is a risk averse expected utility maximizer with a utility function over profits given by u(w) = 1 - e-ow where 0 Calculate Jake's expected utility from lottery P and then determine whether he would choose to adopt the new input. (c) Calculate Jake's certainty equivalent for P and explain how it coincides with your answer to (b)