Question

I only need help with section g). In Parts IV, V, and VI of this case study, you were asked to apply concepts we have

I only need help with section g).

In Parts IV, V, and VI of this case study, you were asked to apply concepts we have discussed in previous chapters related to the sales and collection cycle to the acquisition and cash disbursement cycle. Parts IV, V, and VI dealt with obtaining an understanding of internal control and assessing control risk for transactions affecting accounts payable of Pinnacle Manufacturing. In Part VII, you will design substantive analytical procedures and design and perform tests of details of balances for accounts payable.

Assume that your understanding of internal controls over acquisitions and cash disbursements and the related tests of controls and substantive tests of transactions support an assessment of a low control risk. The listing of the 519 accounts making up the accounts payable balance of $12,969,686 at December 31, 2016, is available online.

Required

-

List those relationships, ratios, and trends that you believe will provide useful information about the overall reasonableness of accounts payable. You should consider income statement accounts that affect accounts payable in selecting the analytical procedures.

-

Study Table 18-5 containing balance-related audit objectives and tests of details of balances for accounts payable to be sure you understand each procedure and its purpose. Prepare an audit program for accounts payable in a performance format, using the audit procedures in Table 18-5. The format of the audit program should be similar to Table 16-5. Be sure to include a sample size for each procedure.

-

Assume for requirement b. that (1) assessed control risk had been high rather than low for each transaction-related audit objective, (2) inherent risk was high for each balance-related audit objective, and (3) analytical procedures indicated a high potential for misstatement. What would the effect have been on the audit procedures and sample sizes for requirement b.?

-

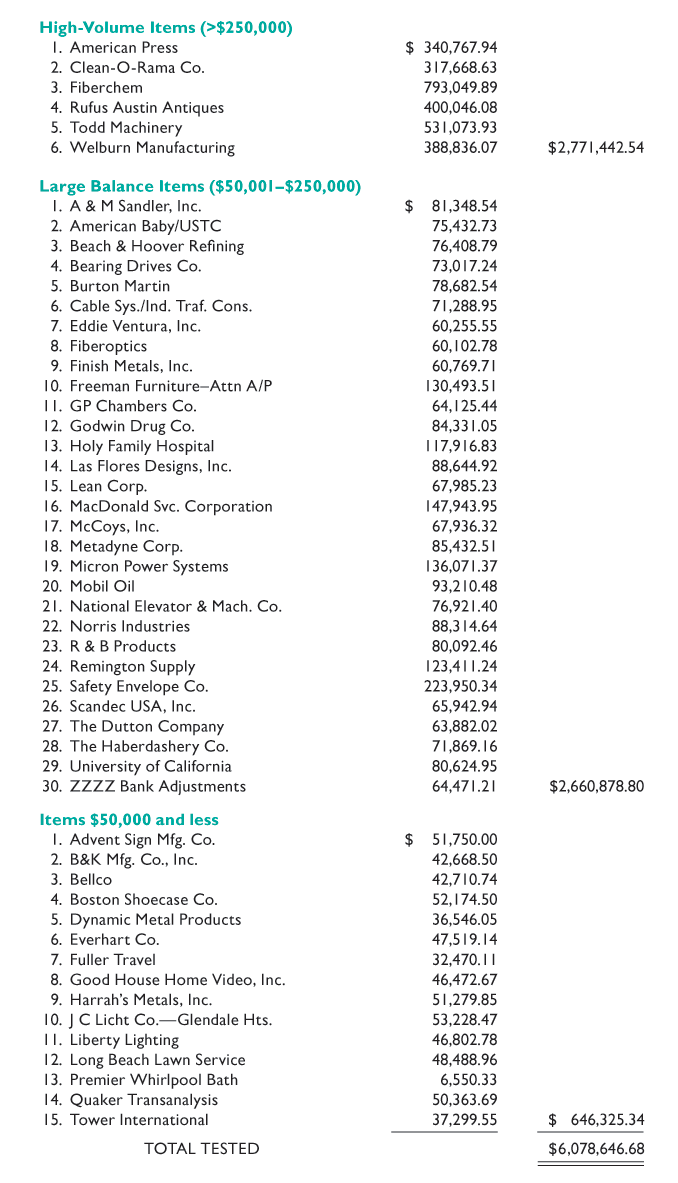

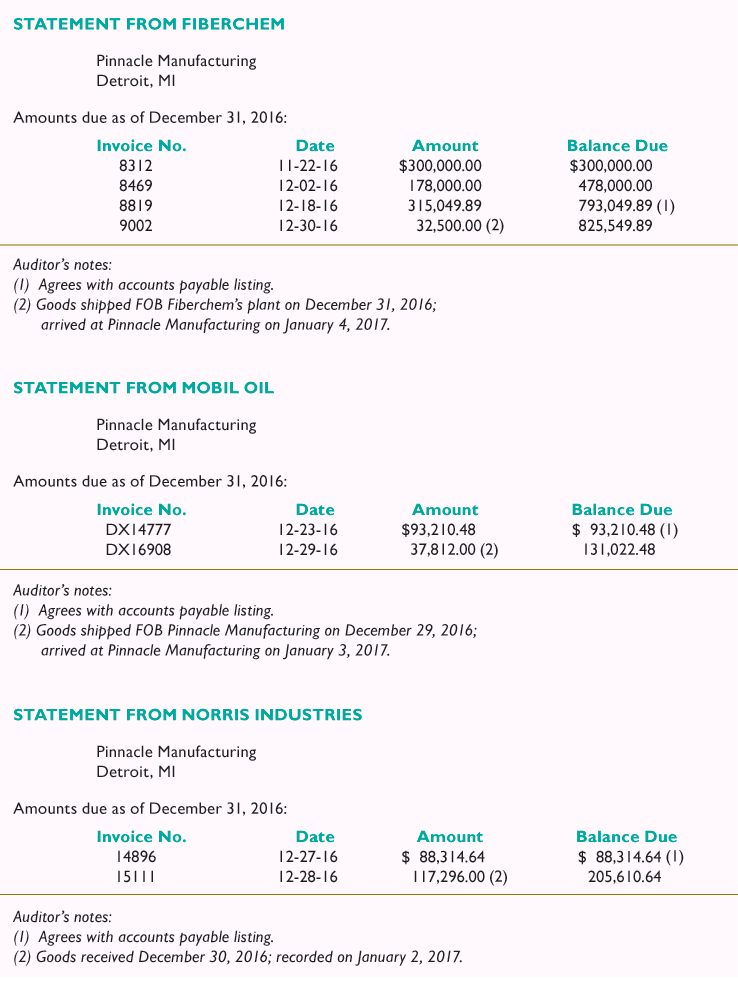

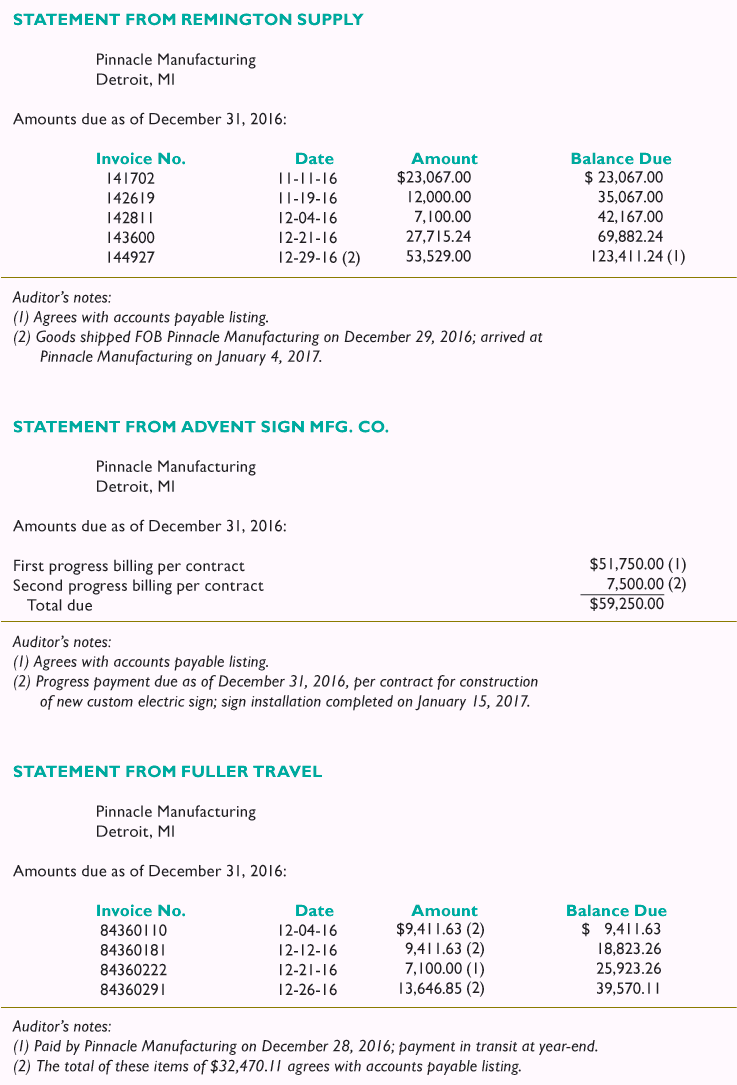

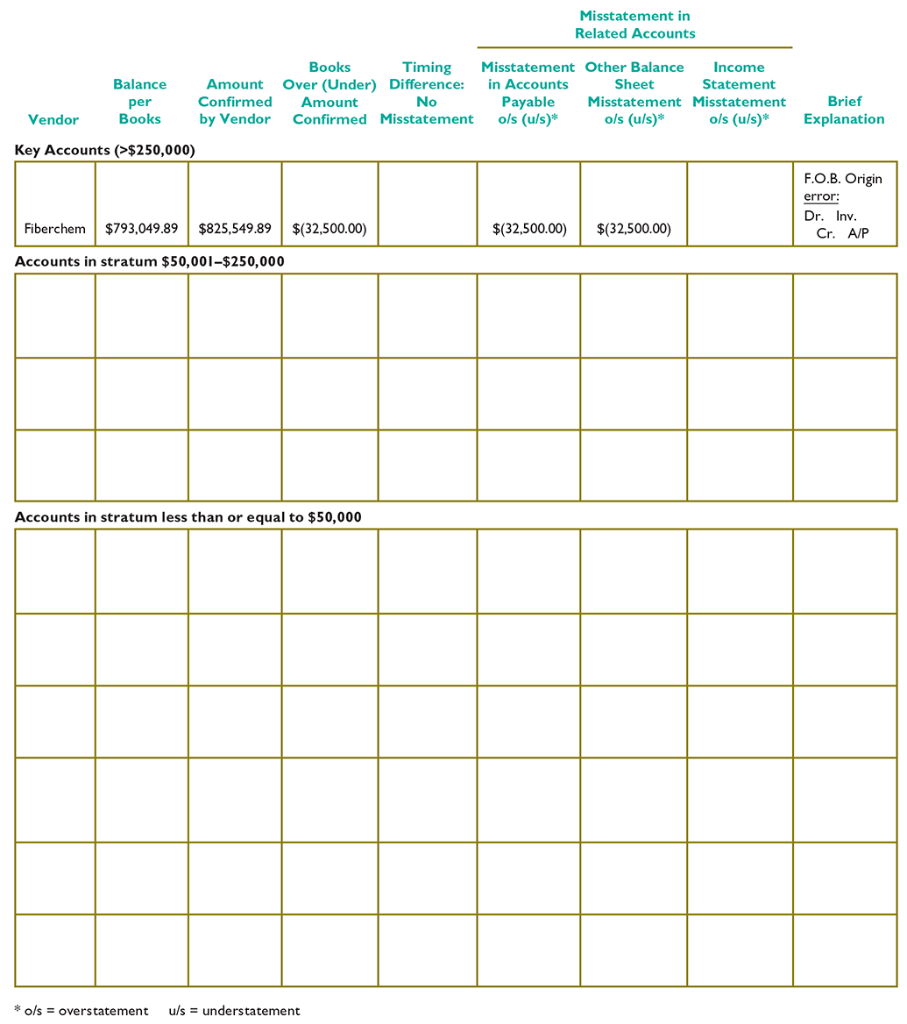

Confirmation requests were sent to a stratified sample of 51 vendors listed in Figure 16-8 Confirmation responses from 45 vendors were returned indicating no difference between the vendors and the companys records. Figure 16-9 presents the six replies that indicate a difference between the vendors balance and the companys records. The auditors follow-up findings are indicated on each reply. Prepare an audit schedule similar to the one illustrated in Figure 16-10 to determine the misstatements, if any, for each difference. The audit schedule format shown in Figure 16-10 is available online. The exception for Fiberchem is analyzed as an illustration. Assume that Pinnacle Manufacturing took a complete physical inventory at December 31, 2016, and the auditor concluded that recorded inventory reflects all inventory on hand at the balance sheet date. Include the balances confirmed without exception as one amount on the schedule for each stratum, and total the schedule columns.

-

Estimate the total misstatement in the income statement, not just the misstatements in the sample, based on the income statement misstatements you identified in requirement d. The total misstatement should include a projected misstatement and an estimated allowance for sampling risk. Note that the misstatements should be projected separately for each stratum. You will need to determine the size of each stratum using the accounts payable listing. Use your judgment to estimate sampling risk, considering the size of the population and the amounts tested.

-

Estimate the total misstatement in accounts payable in the same way you did for the income statement in requirement e. Hint: A misstatement caused by the failure to record an FOB origin purchase is an understatement of accounts payable and inventory and has no effect on income.

Figure 16-8

Pinnacle Manufacturing Sample of Accounts Payable Selected for ConfirmationDecember 31, 2016

Figure 16-9

Replies to Requests for Information

g) What is your conclusion about the fairness of the recorded balance in accounts payable for Pinnacle Manufacturing as it affects the income statement and balance sheet? How does this affect your assessment of control risk as being low for all transaction-related audit objectives? Assume you decided that performance materiality for accounts payable as it affects the income statement is $250,000.

Figure 16-10

Pinnacle Manufacturing Analysis of Trade Accounts PayableDecember 31, 2016

High-Volume Items (>$250,000) 1. American Press 2. Clean-O-Rama Co. 3. Fiberchem 4. Rufus Austin Antiques 5. Todd Machinery 6. Welburn Manufacturing $ 340,767.94 317,668.63 793,049.89 400,046.08 531,073.93 388,836.07 $2,771,442.54 $ Large Balance Items ($50,001-$250,000) 1. A & M Sandler, Inc. 2. American Baby/USTC 3. Beach & Hoover Refining 4. Bearing Drives Co. 5. Burton Martin 6. Cable Sys./Ind. Traf. Cons. 7. Eddie Ventura, Inc. 8. Fiberoptics 9. Finish Metals, Inc. 10. Freeman Furniture-Attn A/P II. GP Chambers Co. 12. Godwin Drug Co. 13. Holy Family Hospital 14. Las Flores Designs, Inc. 15. Lean Corp. 16. MacDonald Svc. Corporation 17. McCoys, Inc. 18. Metadyne Corp. 19. Micron Power Systems 20. Mobil Oil 21. National Elevator & Mach. Co. 22. Norris Industries 23. R & B Products 24. Remington Supply 25. Safety Envelope Co. 26. Scandec USA, Inc. 27. The Dutton Company 28. The Haberdashery Co. 29. University of California 30. ZZZZ Bank Adjustments 81,348.54 75,432.73 76,408.79 73,017.24 78,682.54 71,288.95 60,255.55 60,102.78 60,769.71 130,493.51 64,125.44 84,331.05 117,916.83 88,644.92 67,985.23 147,943.95 67,936.32 85,432.51 136,071.37 93,2 10.48 76,921.40 88,314.64 80,092.46 123,411.24 223,950.34 65,942.94 63,882.02 71,869.16 80,624.95 64,471.21 $2,660,878.80 $ Items $50,000 and less 1. Advent Sign Mfg.Co. 2. B&K Mfg.Co., Inc. 3. Bellco 4. Boston Shoecase Co. 5. Dynamic Metal Products 6. Everhart Co. 7. Fuller Travel 8. Good House Home Video, Inc. 9. Harrah's Metals, Inc. 10. JC Licht Co.-Glendale Hts. II. Liberty Lighting 12. Long Beach Lawn Service 13. Premier Whirlpool Bath 14. Quaker Transanalysis 15. Tower International TOTAL TESTED 51,750.00 42,668.50 42,710.74 52,174.50 36,546.05 47,519.14 32,470.11 46,472.67 51,279.85 53,228.47 46,802.78 48,488.96 6,550.33 50,363.69 37,299.55 $ 646,325.34 $6,078,646.68 STATEMENT FROM FIBERCHEM Pinnacle Manufacturing Detroit, MI Amounts due as of December 31, 2016: Invoice No. Date 8312 11-22-16 8469 12-02-16 8819 12-18-16 9002 12-30-16 Amount $300,000.00 178,000.00 315,049.89 32,500.00 (2) Balance Due $300,000.00 478,000.00 793,049.89 (1) 825,549.89 Auditor's notes: (0) Agrees with accounts payable listing. (2) Goods shipped FOB Fiberchem's plant on December 31, 2016; arrived at Pinnacle Manufacturing on January 4, 2017. STATEMENT FROM MOBIL OIL Pinnacle Manufacturing Detroit, MI Amounts due as of December 31, 2016: Invoice No. Date DX14777 12-23-16 DX16908 12-29-16 Amount $93,210.48 37,812.00 (2) Balance Due $ 93,2 10.48 (0) 131,022.48 Auditor's notes: (1) Agrees with accounts payable listing. (2) Goods shipped FOB Pinnacle Manufacturing on December 29, 2016; arrived at Pinnacle Manufacturing on January 3, 2017. STATEMENT FROM NORRIS INDUSTRIES Pinnacle Manufacturing Detroit, MI Amounts due as of December 31, 2016: Invoice No. Date 14896 12-27-16 15111 12-28-16 Amount $ 88,314.64 117,296.00 (2) Balance Due $ 88,314.64 (1) 205,610.64 Auditor's notes: () Agrees with accounts payable listing. (2) Goods received December 30, 2016; recorded on January 2, 2017 STATEMENT FROM REMINGTON SUPPLY Pinnacle Manufacturing Detroit, MI Amounts due as of December 31, 2016: Invoice No. 141702 142619 142811 143600 144927 Date 11-11-16 11-19-16 12-04-16 12-21-16 12-29-16 (2) Amount $23,067.00 12,000.00 7,100.00 27,715.24 53,529.00 Balance Due $ 23,067.00 35,067.00 42,167.00 69,882.24 123,411.24 (1) Auditor's notes: (1) Agrees with accounts payable listing. (2) Goods shipped FOB Pinnacle Manufacturing on December 29, 2016; arrived at Pinnacle Manufacturing on January 4, 2017. STATEMENT FROM ADVENT SIGN MFG. CO. Pinnacle Manufacturing Detroit, MI Amounts due as of December 31, 2016: First progress billing per contract Second progress billing per contract Total due $51,750.00 (0) 7,500.00 (2) $59,250.00 Auditor's notes: (1) Agrees with accounts payable listing. (2) Progress payment due as of December 31, 2016, per contract for construction of new custom electric sign; sign installation completed on January 15, 2017. STATEMENT FROM FULLER TRAVEL Pinnacle Manufacturing Detroit, MI Amounts due as of December 31, 2016: Invoice No. 84360110 84360181 84360222 84360291 Date 12-04-16 12-12-16 12-21-16 12-26-16 Amount $9,411.63 (2) 9,411.63 (2) 7,100.00 (0) 13,646.85 (2) Balance Due $ 9,411.63 18,823.26 25,923.26 39,570.11 Auditor's notes: (1) Paid by Pinnacle Manufacturing on December 28, 2016; payment in transit at year-end. (2) The total of these items of $32,470.11 agrees with accounts payable listing. Misstatement in Related Accounts Balance per Books Books Timing Misstatement Other Balance Income Amount Over (Under) Difference: in Accounts Sheet Statement Confirmed Amount No Payable Misstatement Misstatement by Vendor Confirmed Misstatement ols (u/s)* ols (u/s)* ols (u/s)* Vendor Brief Explanation Key Accounts (>$250,000) F.O.B. Origin error: Dr. Inv. Cr. A/P Fiberchem $793,049.89 $825,549.89 $(32,500.00) $(32,500.00) $(32,500.00) Accounts in stratum $50,001-$250,000 Accounts in stratum less than or equal to $50,000 *ols = overstatement u/s = understatement

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting A Managerial Emphasis

Authors: Charles T. Horngren, George Foster, Srikant M. Datar, Howard D. Teall, Foster Horngren, Data Horngren

3rd Canadian Edition

0130355801, 978-0130355805