Question

I realize this is a comprehensive problem but I am stuck on a few portions. :( PARTNERSHIP TAX RETURN PROBLEM 2 Required: Using the information

I realize this is a comprehensive problem but I am stuck on a few portions. :(

I realize this is a comprehensive problem but I am stuck on a few portions. :(

PARTNERSHIP TAX RETURN PROBLEM 2

Required:

Using the information provided below, complete Arlington Building Supply's (ABS) 2015 Form 1065 and Schedule D. Also complete Jerry Johnson and Steve Stillwell's Schedule K-1.

Form 4562 for depreciation is not required. Use the amount of tax depreciation and 179 expense provided in the income statement and the information in #4 below to complete the appropriate lines on the first page and on Schedule K of Form 1065.

Page C-21

Form 4797 for the sale of trade or business property is not required. Use the amount of gain and loss from the sale of the truck and forklifts in the income statement and the information provided in #4 and #5 below to complete the appropriate lines on the first page and on Schedule K of Form 1065.

If any information is missing, use reasonable assumptions to fill in any gaps.

The forms, schedules, and instructions can be found at the IRS Web site (www.irs.gov). The instructions can be helpful in completing the forms.

Facts:

On January 1, 2005, two enterprising men in the community, Jerry Johnson and Steve Swiss Stillwell, anticipated a boom in the local construction industry. They decided to sell their small businesses and pool their resources as general partners in establishing a retail outlet for lumber and other building materials, including a complete line of specialty hardware for prefab tree-houses. Their general partnership was officially formed under the name of Arlington Building Supply and soon became a thriving business.

ABS is located at 2174 Progress Ave., Arlington, Illinois 64888.

ABS's Employer Identification Number is 91-3697984.

ABS's business activity is retail construction. Its business activity code is 444190.

Both general partners are active in the management of ABS.

Jerry Johnson's Social Security number is 500-23-4976. His address is 31 W. Oak Drive, Arlington, Illinois 64888.

Steve Stillwell's Social Security number is 374-68-3842. His address is 947 E. Linder Street, Arlington, Illinois 64888.

ABS uses the accrual method of accounting and has a calendar year-end.

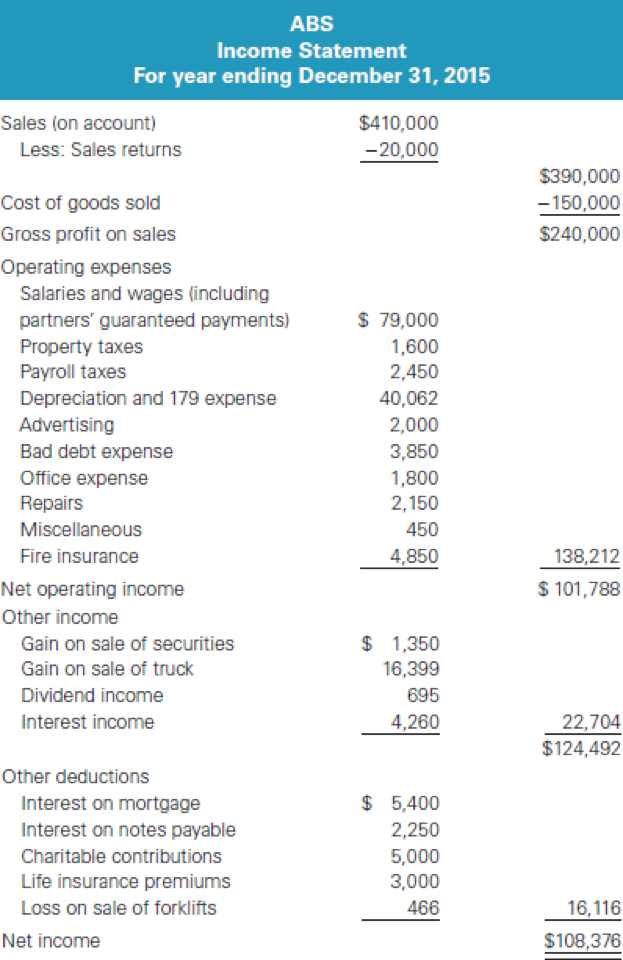

The following is ABS's 2015 income statement: ABOVE

Page C-22

Notes:

The partnership maintains its books according to the 704(b) regulations. Under this method of accounting, all book and tax numbers are the same except for life insurance premiums and tax-exempt interest.

The partners' percentage ownership of original contributed capital is 30 percent for Johnson and 70 percent for Stillwell. They agree that profits and losses will be shared according to this same ratio. Any additional capital contributions and withdrawals must be made in these same ratios.

For their services to the company, the partners will receive the following annual guaranteed payments:

| Johnson | $28,000 |

| Stillwell | $21,000 |

Johnson is expected to devote all his time to the business, while Stillwell will devote approximately 75 percent of his.

Two forklifts were sold in September 2015. The old lifts were purchased new four years ago. Two new forklifts were purchased on September 1, 2015, for $32,000 and the partnership intends to immediately expense them under 179 (see depreciation and 179 expense in the income statement above).

The truck sold this year was purchased several years ago. $16,099 of the total gain from the sale of the truck should be recaptured as ordinary income under IRC 1245.

The partnership uses currently allowable tax depreciation methods for both regular tax and book purposes and has adopted a policy of electing not to claim bonus depreciation. Assume alternative minimum tax depreciation equals regular tax depreciation.

The partners decided to invest in a small tract of land with the intention of selling it about a year later at a substantial profit. On January 1, 2015, they executed a $50,000 note with the bank to obtain the $70,000 cash purchase price. Interest on the note is payable yearly, and the principal is due in 18 months. The first interest payment of $2,250 was made on December 30, 2015 (see interest on notes payable in income statement above).

The note payable to the bank as well as the accounts payable are treated by the partnership as recourse debt. Assume the total recourse debt is allocated $28,776 to Jerry and $70,224 to Steve.

Some years after the partnership was formed, a mortgage of $112,500 was obtained on the land and warehouse from Commerce State Bank. Principal payments of $4,500 must be paid each December 31, along with 8 percent interest on the outstanding balance (see interest on mortgage in income statement above). The holder of the note agreed therein to look only to the land and warehouse for his security in the event of default. Because this mortgage is nonrecourse debt, it should be allocated among the partners according to their profit sharing ratios.

Page C-23

The partnership values its inventory at lower of cost or market and uses the FIFO inventory method. Assume the rules of 263A do not apply to ABS.

During the year, the partnership bought 300 shares of ABC, Ltd., for $6,100 on February 8, 2015. All the shares were sold for $6,650 on April 2, 2015. ABS received a Form 1099-B indicating that the basis of the ABC shares was reported to the IRS.

Two hundred shares of XYZ Corporation were sold for $10,600 on September 13, 2015. The stock was purchased on December 1, 2009, and is not eligible for the 28 percent capital gains rate. ABS received a Form 1099-B indicating that the basis of the XYZ shares was $9,800.

The following dividends were received:

| XYZ (qualified) | $400 |

| ABC, Ltd. (not qualified) | 295 |

| Total | $695 |

The partnership received interest income from the following sources:

| Interest on Illinois municipal bonds | $3,200 |

| Interest on savings | 560 |

| Interest on accounts receivable | 500 |

| Total | $4,260 |

The partnership donated $5,000 cash to the Red Cross.

Life insurance policies on the lives of Johnson and Stillwell were purchased in the prior year. The partnership will pay all the premiums and is the beneficiary of the policy. The premiums for the current year were $3,000 (see income statement above), and no cash surrender value exists for the first or second year of the policy.

The partners withdrew the following cash amounts from the partnership during the year (in addition to their guaranteed payments):

| Johnson | $20,000 |

| Stillwell | 35,000 |

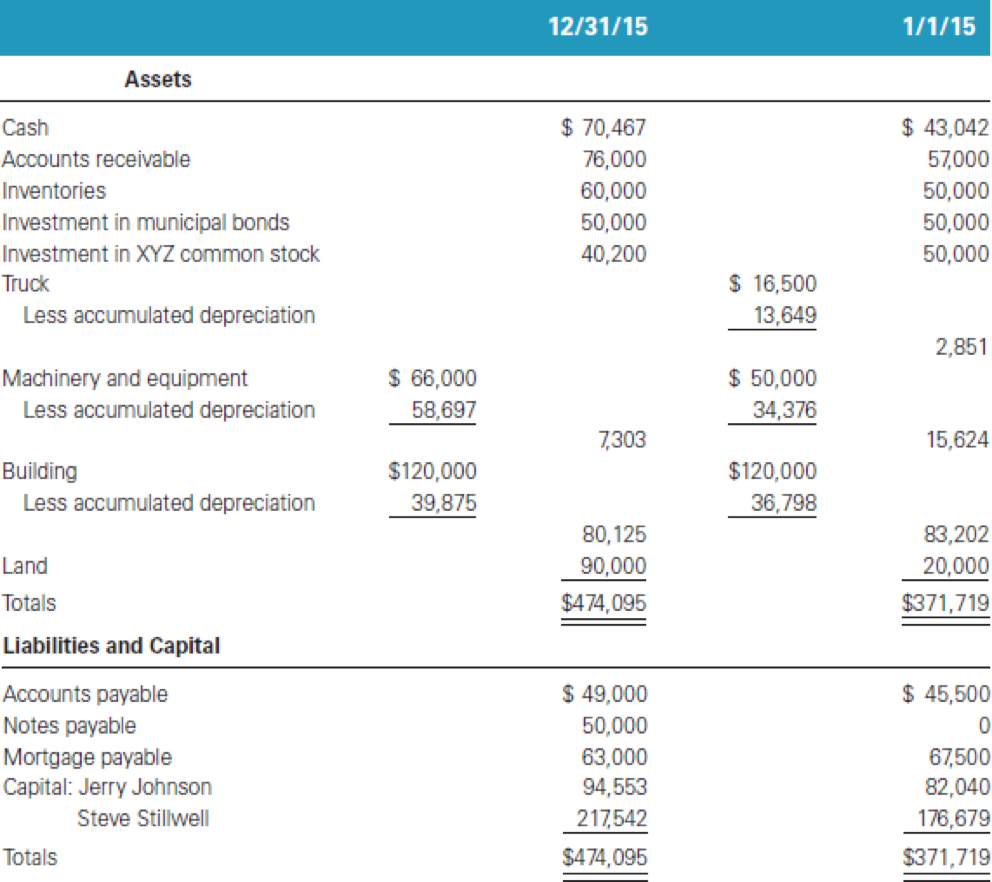

The following are ABS's balance sheets as of January 1, 2015, and December 31, 2015. ABOVE

ABS Income Statement For year ending December 31, 2015 $410,000 Sales (on account) 20,000 Less: Sales returns Cost of goods sold Gross profit on sales Operating expenses Salaries and wages (including 79,000 partners' guaranteed payments) Property taxes 1.600 Payroll taxes 2.450 Depreciation and 179 expense 40.062 2,000 Advertising 3,850 Bad debt expense 1.800 Office expense Repairs 2.150 Miscellaneous 450 Fire insurance 4,850 Net operating income Other income 1.350 Gain on sale of securities Gain on sale of truck 16.399 Dividend income 695 Interest income 4.260 Other deductions 5.400 Interest on mortgage Interest on notes payable 2.250 Charitable contributions 5.000 3,000 Life insurance premiums Loss on sale of forklifts 466 Net income $390,000 150,000 $240,000 138,212 101,788 22,704 $124,492 16.116 $108,376 ABS Income Statement For year ending December 31, 2015 $410,000 Sales (on account) 20,000 Less: Sales returns Cost of goods sold Gross profit on sales Operating expenses Salaries and wages (including 79,000 partners' guaranteed payments) Property taxes 1.600 Payroll taxes 2.450 Depreciation and 179 expense 40.062 2,000 Advertising 3,850 Bad debt expense 1.800 Office expense Repairs 2.150 Miscellaneous 450 Fire insurance 4,850 Net operating income Other income 1.350 Gain on sale of securities Gain on sale of truck 16.399 Dividend income 695 Interest income 4.260 Other deductions 5.400 Interest on mortgage Interest on notes payable 2.250 Charitable contributions 5.000 3,000 Life insurance premiums Loss on sale of forklifts 466 Net income $390,000 150,000 $240,000 138,212 101,788 22,704 $124,492 16.116 $108,376Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mcgraw Hills Homework Manager Access Code To Accompany Introduction To Managerial Accounting

Authors: Peter Brewer, Ray Garrison, Eric Noreen

3rd Edition

0073264938, 978-0073264936