Answered step by step

Verified Expert Solution

Question

1 Approved Answer

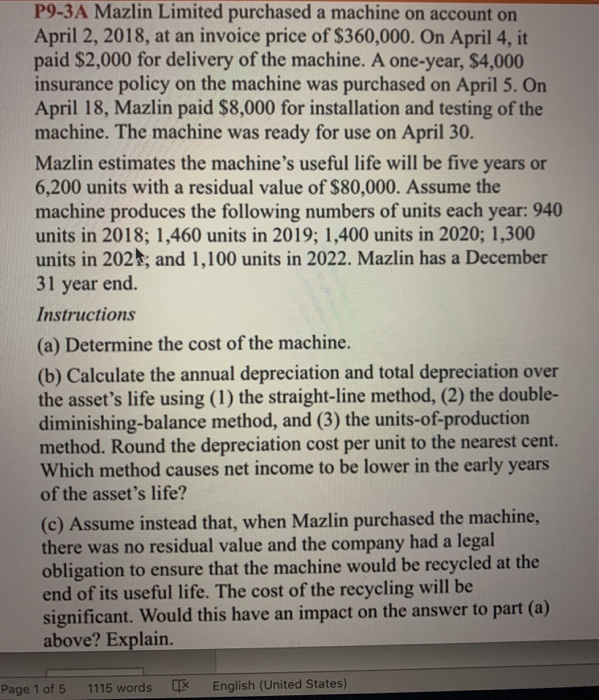

i think it's ok. i needed to understand which i did. thank you anyway. P9-3A Mazlin Limited purchased a machine on account on April 2,

i think it's ok. i needed to understand which i did. thank you anyway.

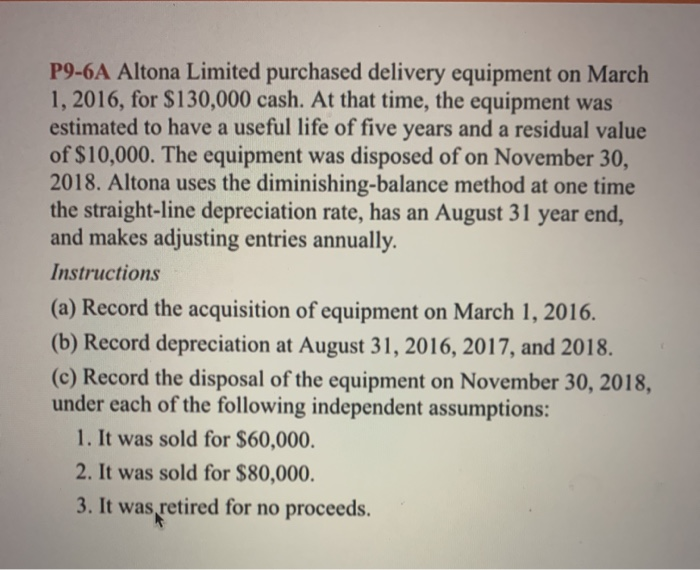

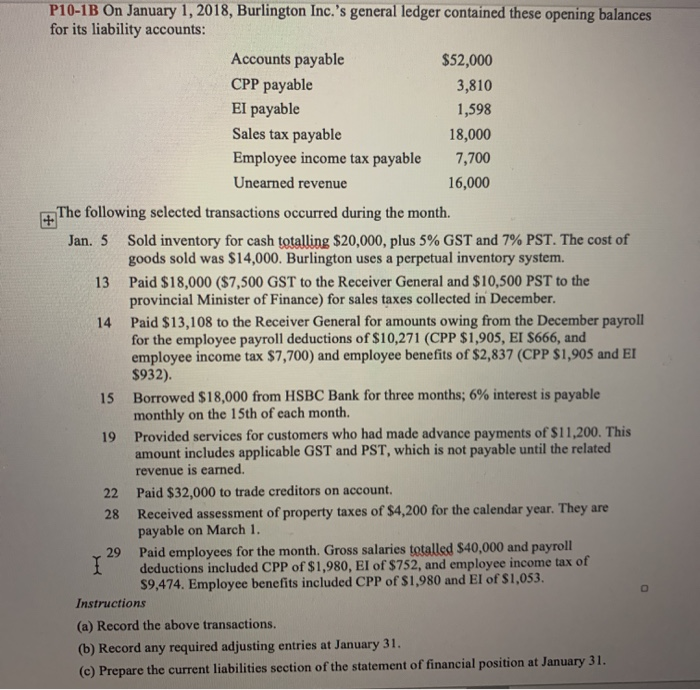

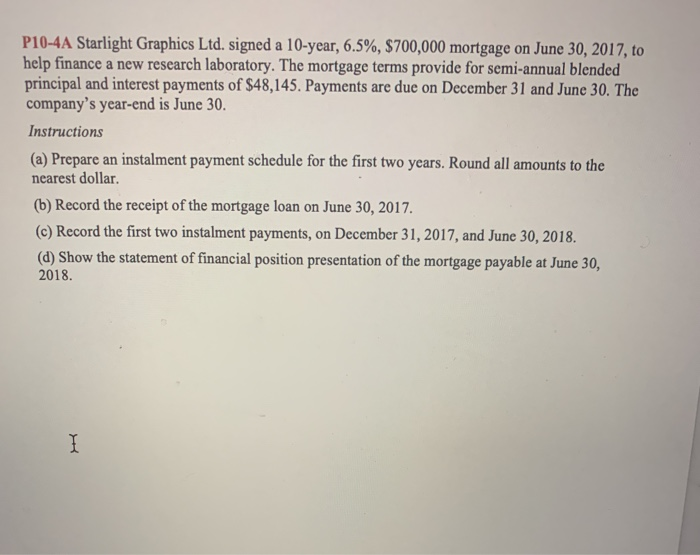

P9-3A Mazlin Limited purchased a machine on account on April 2, 2018, at an invoice price of $360,000. On April 4, it paid $2,000 for delivery of the machine. A one-year, $4,000 insurance policy on the machine was purchased on April 5. On April 18, Mazlin paid $8,000 for installation and testing of the machine. The machine was ready for use on April 30. Mazlin estimates the machine 's useful life will be five years or 6,200 units witha residual value of $80,000. Assume the machine produces the following numbers of units each year: 940 units in 2018; 1,460 units in 2019; 1,400 units in 2020; 1,300 units in 202; and 1,100 units in 2022. Mazlin has a December 31 year end. Instructions (a) Determine the cost of the machine. (b) Calculate the annual depreciation and total depreciation over the asset's life using (1) the straight-line method, (2) the double- diminishing-balance method, and (3) the units-of-production method. Round the depreciation cost per unit to the nearest cent. Which method causes net income to be lower in the early years of the asset's life? (c) Assume instead that, when Mazlin purchased the machine, there was no residual value and the company had a legal obligation to ensure that the machine would be recycled at the end of its useful life. The cost of the recycling will be significant. Would this have an impact on the answer to part (a) above? Explain. English (United States) Page 1 of 5 1115 words P9-6A Altona Limited purchased delivery equipment on March 1, 2016, for $130,000 cash. At that time, the equipment was estimated to have a useful life of five years and a residual value of $10,000. The equipment was disposed of on November 30, 2018. Altona uses the diminishing-balance method at one time the straight-line depreciation rate, has an August 31 year end, and makes adjusting entries annually. Instructions (a) Record the acquisition of equipment on March 1, 2016. (b) Record depreciation at August 31, 2016, 2017, and 2018. (c) Record the disposal of the equipment on November 30, 2018 under each of the following independent assumptions: 1. It was sold for $60,000 2. It was sold for $80,000 3. It was retired for no proceeds P10-1B On January 1, 2018, Burlington Inc.'s general ledger contained these opening balances for its liability accounts: Accounts payable $52,000 CPP payable 3,810 El payable 1,598 Sales tax payable 18,000 Employee income tax payable 7,700 Unearned revenue 16,000 The following selected transactions occurred during the month. Sold inventory for cash totalling $20,000, plus 5% GST and 7% PST . The cost of goods sold was $14,000. Burlington uses a perpetual inventory system. Jan. 5 Paid $18,000 ($7,500 GST to the Receiver General and $10,500 PST to the provincial Minister of Finance) for sales taxes collected in December. Paid $13,108 to the Receiver General for amounts owing from the December payroll for the employee payroll deductions of $10,271 (CPP $1,905, EI $666, and employee income tax $7,700) and employee benefits of $2,837 (CPP $1,905 and El $932). 15 13 14 Borrowed $18,000 from HSBC Bank for three months; 6 % interest is payable monthly on the 15th of each month. Provided services for customers who had made advance payments of $11,200. This amount includes applicable GST and PST, which is not payable until the related 19 revenue is earned. Paid $32,000 to trade creditors on account. 22 Received assessment of property taxes of $4,200 for the calendar year. They are payable on March 1. 28 Paid employees for the month. Gross salaries totalled $40,000 and payroll I deductions included CPP of $1,980, EI of $752, and employee income tax of $9,474. Employee benefits included CPP of $1,980 and El of $1,053 Instructions (a) Record the above transactions. (b) Record any required adjusting entries at January 31. (c) Prepare the current liabilities section of the statement of financial position at January 31. 29 P10-4A Starlight Graphics Ltd. signed a 10-year, 6.5%, $700,000 mortgage on June 30, 2017, to help finance a new research laboratory. The mortgage terms provide for semi-annual blended principal and interest payments of $48,145. Payments are due on December 31 and June 30. The company's year-end is June 30. Instructions (a) Prepare an instalment payment schedule for the first two years. Round all amounts to the nearest dollar. (b) Record the receipt of the mortgage loan on June 30, 2017 (c) Record the first two instalment payments, on December 31, 2017, and June 30, 2018 (d) Show the statement of financial position presentation of the mortgage payable at June 30, 2018 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting And Reporting A Global Perspective

Authors: Herv Stolowy, Yuan Ding

5th Edition

1473740207, 978-1473740204