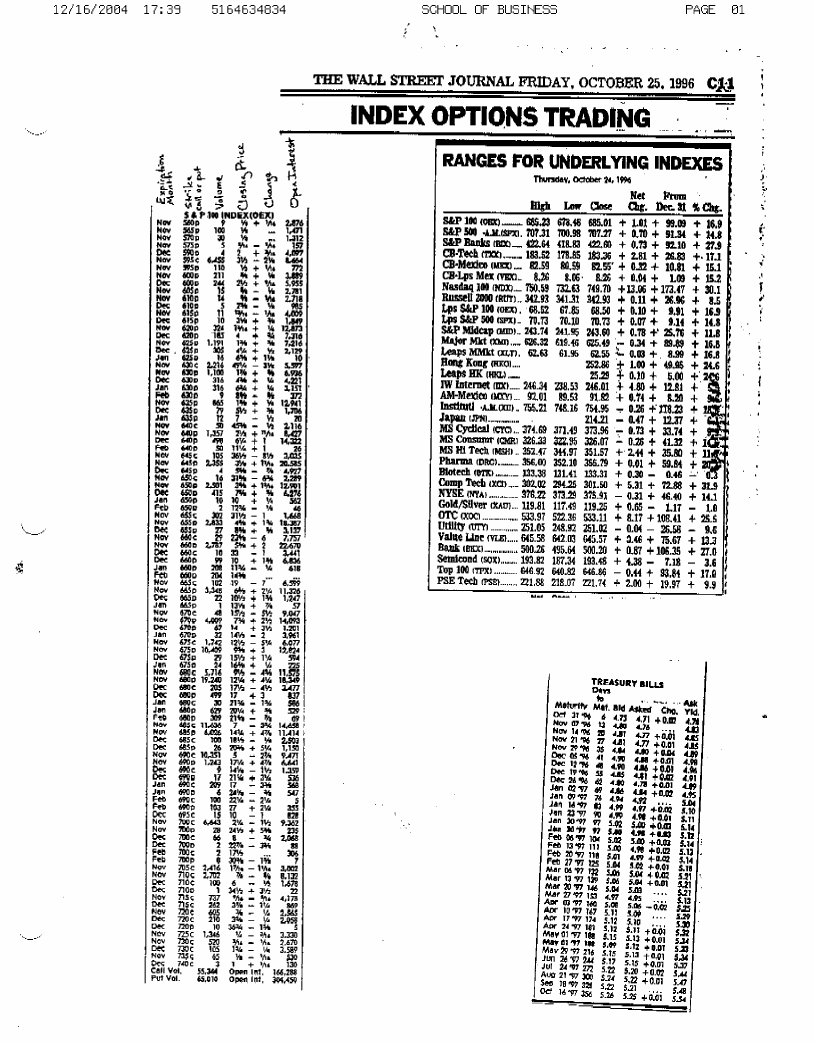

Question

(i) Using the information from the Friday, October 26, 1996 Wall Street Journal, calculate the implied volatility from the S&P 100 index (put only). In

(i) Using the information from the Friday, October 26, 1996 Wall Street Journal, calculate

the implied volatility from the S&P 100 index (put only). In particular, calculate for all

strike/exercise prices between 660 and 680 for options expiring in December and January

only. Note that by design index options expire on the 3rd Friday of each month so

calculate the time to maturity accordingly (assume 365 day year). In addition, use the

risk-free rate (T-Bills) closest to expiration date of the option. Remember that the RF rate

is quoted in annualized terms.

! 2

Graph the implied volatility against the strike price on a separate graph for December and

January.

Is the volatility constant?

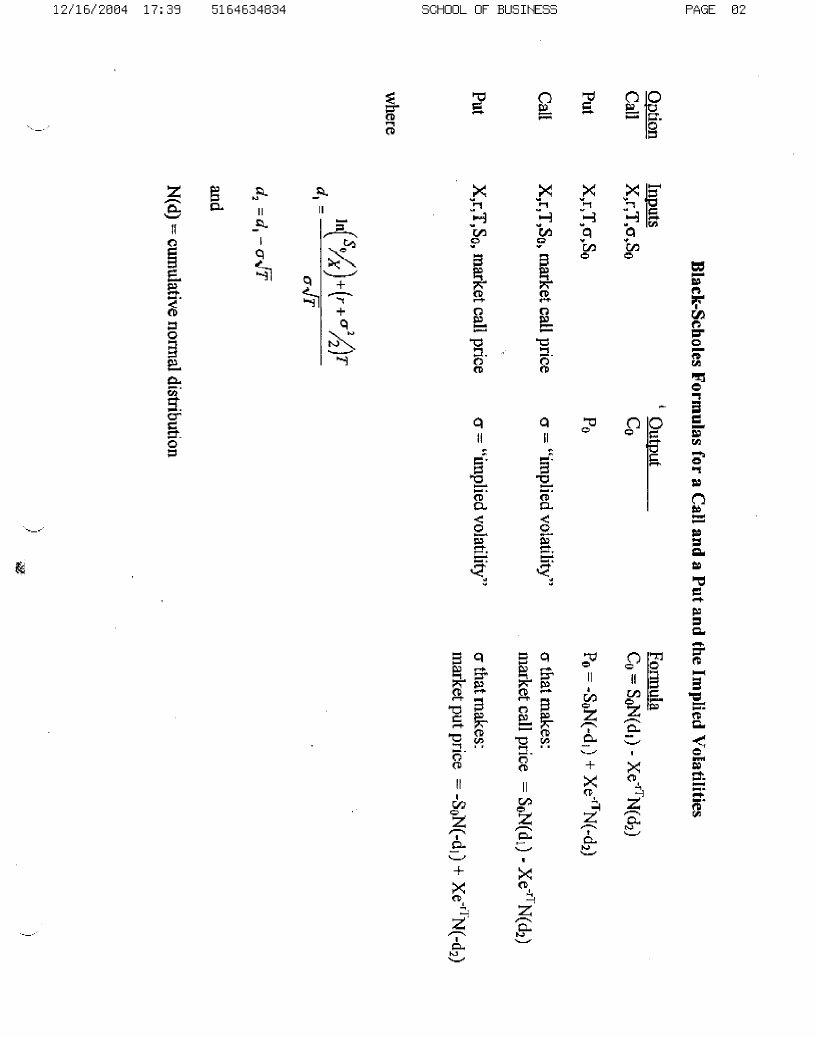

To solve for the implied volatility you may use trial and error by equating the theoretical

price from B-S (which you must compute) to the actual market (closing price) by trial

and error, i.e. varying , but I recommend using either the Solver or Goal Seek function

in Excel.

(ii) Use the above data to estimate delta. Create graph in excel.

(iii) Use the above data to estimate gamma. Create graph in excel.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Home Energy Audit Your Guide To Understanding And Reducing Your Home Energy Costs

Authors: Richard Montgomery

1st Edition

0471864668, 978-0471864660