Answered step by step

Verified Expert Solution

Question

1 Approved Answer

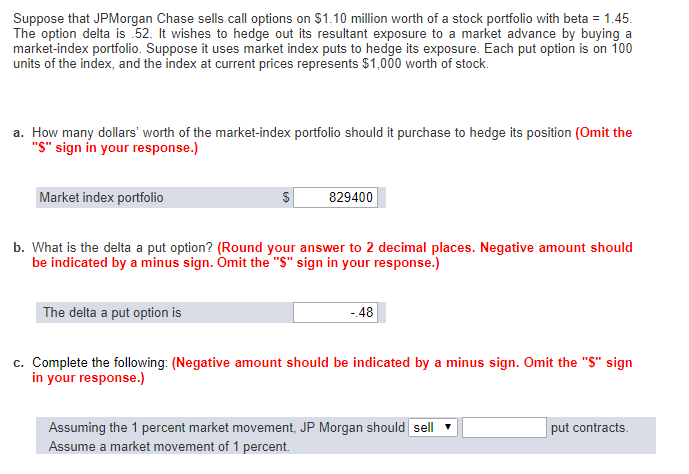

I was able to get parts a and b. Cannot figure out part c. Please advise (This is all the information given in the problem,

I was able to get parts a and b. Cannot figure out part c. Please advise (This is all the information given in the problem, the last chegg helper said there wasnt enough info, but there is)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis For Financial Management

Authors: Robert C. Higgins

10th International Edition

007108648X, 9780071086486