I was doing great until I hit this question. Please advise

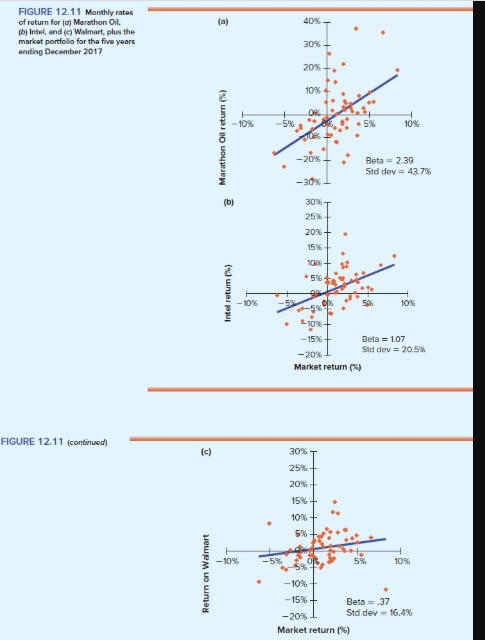

Figure 12.11 shows plots of monthly rates of return on three stocks versus the stock market index. The beta and standard deviation of each stock is given beside its plot. Required: a. Which stock is safest for a diversified investor? b. Which stock is safest for an undiversified investor who puts all her funds in one of these stocks? c. Consider a portfolio with equal investments in each stock. What would this portfolio's beta have been? d. Consider a well-diversified portfolio made up of stocks with the same beta as Intel. What are the beta and standard deviation of this portfolio's return? The standard deviation of the market portfolio's return is 20%. e. What is the expected rate of return on each stock? Use the capital asset pricing model with a market risk premium of 8%. The risk- free rate of interest is 4%. Complete this question by entering your answers in the tabs below. Req A and B Reg C Reg D Reg E Consider a portfolio with equal investments in each stock. What would this portfolio's beta have been? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Beta (a) 40% FIGURE 12.11 Monthly rates of return for (a) Marathon Oil, b) Intel, and (c) Walmart, plus the market portfolio for the five years ending December 2017 30% 20% 10% -10% -5% .. 5% 10% Marathon Oil return (%) 086 -20% Beta - 2.39 Std dey 43.7% -30% (b) 30T 25% 20% + 15% 100+ . 5% Intel retum (%) -10% 9 10% -5% 210% -15% Beta = 1.07 Std dev = 20.5% -20% Market return) FIGURE 12.11 continued) (c) 30% 25% 20% 15% 10% 5% -10% 5% 10% Return on Walmart -10% -15% Beta = .37 -20% Std dev 16.4% Market return (%) Figure 12.11 shows plots of monthly rates of return on three stocks versus the stock market index. The beta and standard deviation of each stock is given beside its plot. Required: a. Which stock is safest for a diversified investor? b. Which stock is safest for an undiversified investor who puts all her funds in one of these stocks? c. Consider a portfolio with equal investments in each stock. What would this portfolio's beta have been? d. Consider a well-diversified portfolio made up of stocks with the same beta as Intel. What are the beta and standard deviation of this portfolio's return? The standard deviation of the market portfolio's return is 20%. e. What is the expected rate of return on each stock? Use the capital asset pricing model with a market risk premium of 8%. The risk- free rate of interest is 4%. Complete this question by entering your answers in the tabs below. Req A and B Reg C Reg D Reg E Consider a portfolio with equal investments in each stock. What would this portfolio's beta have been? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Beta (a) 40% FIGURE 12.11 Monthly rates of return for (a) Marathon Oil, b) Intel, and (c) Walmart, plus the market portfolio for the five years ending December 2017 30% 20% 10% -10% -5% .. 5% 10% Marathon Oil return (%) 086 -20% Beta - 2.39 Std dey 43.7% -30% (b) 30T 25% 20% + 15% 100+ . 5% Intel retum (%) -10% 9 10% -5% 210% -15% Beta = 1.07 Std dev = 20.5% -20% Market return) FIGURE 12.11 continued) (c) 30% 25% 20% 15% 10% 5% -10% 5% 10% Return on Walmart -10% -15% Beta = .37 -20% Std dev 16.4% Market return (%)