Answered step by step

Verified Expert Solution

Question

1 Approved Answer

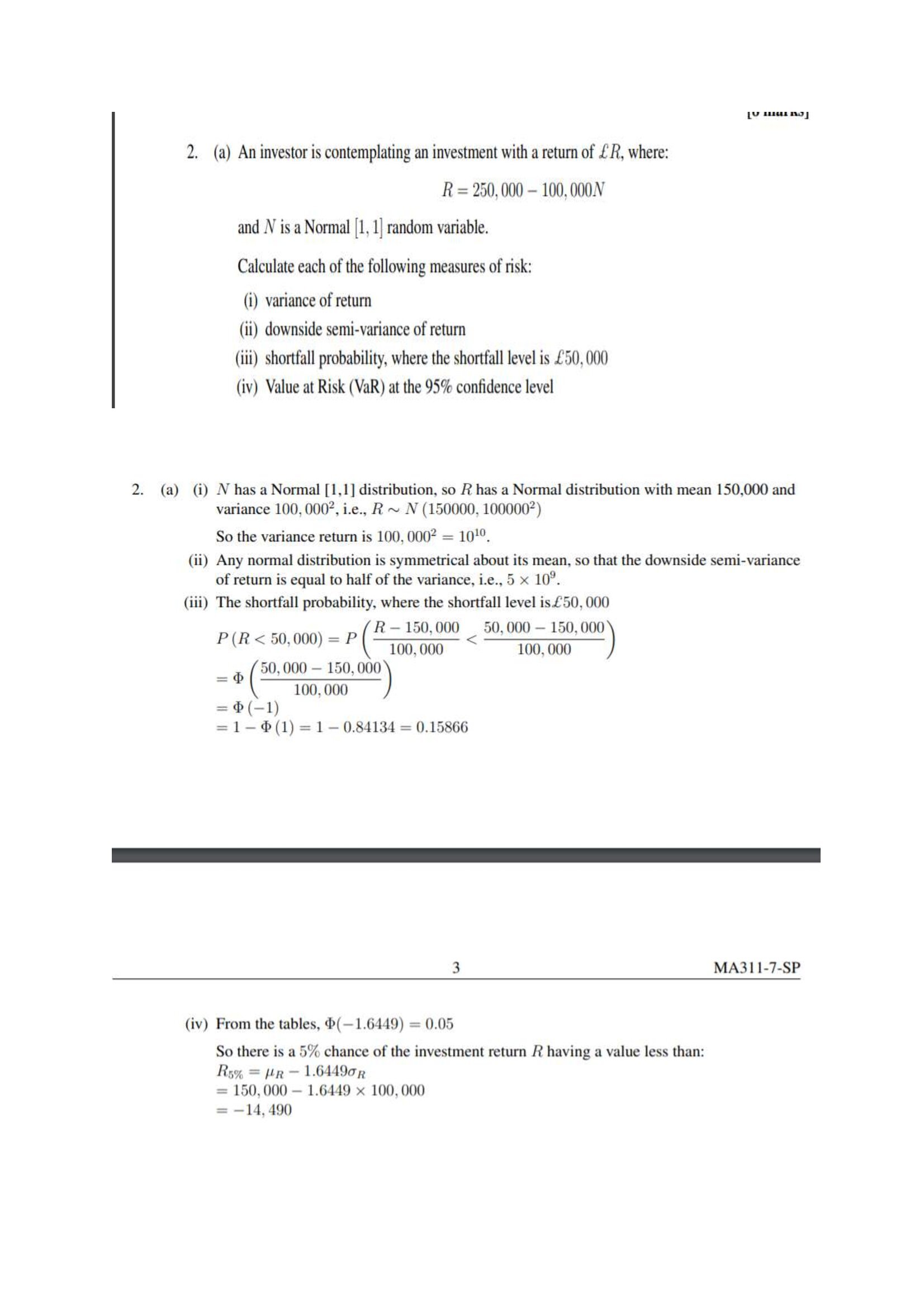

I would like to understand how can I get the solution below? How they decided mean =150000 and variance =100000^2? l mu] 2. (a) An

I would like to understand how can I get the solution below?

How they decided mean =150000 and variance =100000^2?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus Early Transcendentals, Multivariable

Authors: Michael Sullivan, Kathleen Miranda

2nd Edition

131924288X, 9781319242886