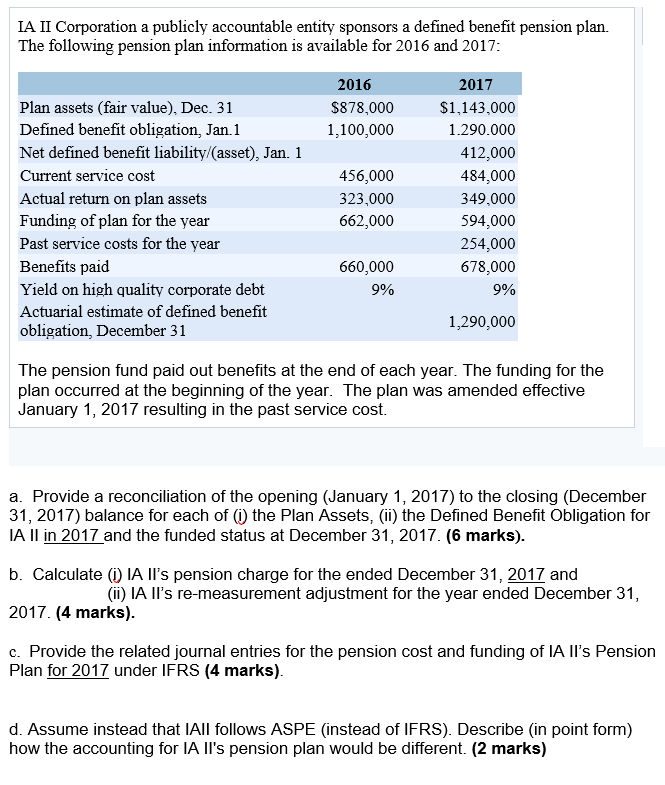

IA II Corporation a publicly accountable entity sponsors a defined benefit pension plan. The following pension plan information is available for 2016 and 2017: 2016 $878,000 1,100,000 Plan assets (fair value), Dec. 31 Defined benefit obligation, Jan. 1 Net defined benefit liability/asset), Jan. 1 Current service cost Actual return on plan assets Funding of plan for the year Past service costs for the year Benefits paid Yield on high quality corporate debt Actuarial estimate of defined benefit obligation, December 31 456,000 323,000 662,000 2017 $1,143,000 1.290.000 412,000 484,000 349,000 594,000 254,000 678,000 9% 660,000 9% 1,290,000 The pension fund paid out benefits at the end of each year. The funding for the plan occurred at the beginning of the year. The plan was amended effective January 1, 2017 resulting in the past service cost. a. Provide a reconciliation of the opening (January 1, 2017) to the closing (December 31, 2017) balance for each of the Plan Assets, (ii) the Defined Benefit Obligation for IA II in 2017 and the funded status at December 31, 2017. (6 marks). b. Calculate (1) IA II's pension charge for the ended December 31, 2017 and (ii) IA Il's re-measurement adjustment for the year ended December 31, 2017. (4 marks). c. Provide the related journal entries for the pension cost and funding of IA II's Pension Plan for 2017 under IFRS (4 marks). d. Assume instead that IAll follows ASPE (instead of IFRS). Describe (in point form) how the accounting for IA Il's pension plan would be different. (2 marks) IA II Corporation a publicly accountable entity sponsors a defined benefit pension plan. The following pension plan information is available for 2016 and 2017: 2016 $878,000 1,100,000 Plan assets (fair value), Dec. 31 Defined benefit obligation, Jan. 1 Net defined benefit liability/asset), Jan. 1 Current service cost Actual return on plan assets Funding of plan for the year Past service costs for the year Benefits paid Yield on high quality corporate debt Actuarial estimate of defined benefit obligation, December 31 456,000 323,000 662,000 2017 $1,143,000 1.290.000 412,000 484,000 349,000 594,000 254,000 678,000 9% 660,000 9% 1,290,000 The pension fund paid out benefits at the end of each year. The funding for the plan occurred at the beginning of the year. The plan was amended effective January 1, 2017 resulting in the past service cost. a. Provide a reconciliation of the opening (January 1, 2017) to the closing (December 31, 2017) balance for each of the Plan Assets, (ii) the Defined Benefit Obligation for IA II in 2017 and the funded status at December 31, 2017. (6 marks). b. Calculate (1) IA II's pension charge for the ended December 31, 2017 and (ii) IA Il's re-measurement adjustment for the year ended December 31, 2017. (4 marks). c. Provide the related journal entries for the pension cost and funding of IA II's Pension Plan for 2017 under IFRS (4 marks). d. Assume instead that IAll follows ASPE (instead of IFRS). Describe (in point form) how the accounting for IA Il's pension plan would be different. (2 marks)