Answered step by step

Verified Expert Solution

Question

1 Approved Answer

If the risk-free rate is 1.5%, calculate the Sharpe ratios of these three (3) assets. Do you think the allocation of this investor's portfolio is

If the risk-free rate is 1.5%, calculate the Sharpe ratios of these three (3) assets. Do you think the allocation of this investor's portfolio is optimal? If yes, why? If no, how would you recommend to change and why?

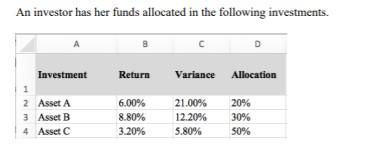

An investor has her funds allocated in the following investments. Investment 1 2 Asset A 3 Asset B 4 Asset C Return Variance Allocation 6.00% 8.80% 3.20% 21.00% 12.20% 5.80% 20% 30% 50%

Step by Step Solution

★★★★★

3.40 Rating (166 Votes )

There are 3 Steps involved in it

Step: 1

SOLUTION To calculate the Sharpe ratios we first need to calculate the expected returns of each asse...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Corporate Finance

Authors: Berk, DeMarzo, Harford

2nd edition

132148234, 978-0132148238