Question

If the yield curve instantaneously makes a parallel shift down of 1.0%, which statement about the bonds sensitivity to the change in interest rates (i.e.

If the yield curve instantaneously makes a parallel shift down of 1.0%, which statement about the bonds sensitivity to the change in interest rates (i.e. duration) is most accurate?

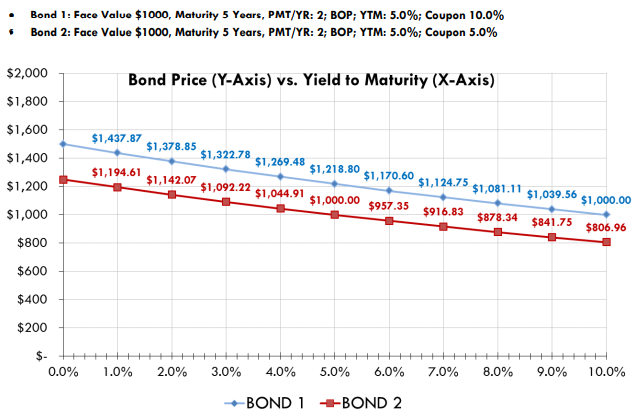

A) Bond 1 has the greatest sensitivity to the change in interest rates because it increases in value by $50.68

B) Bond 2 has the greatest sensitivity to the change in interest rates because it increases in value by 4.5%

C) Bond 1 has the greatest sensitivity to the change in interest rates because it decreases in value by 4.2%

D) Bond 1 has the greatest sensitivity to the change in interest rates because it decreases in value by $48.20

E) Bond 2 has the greatest sensitivity to the change in interest rates because it decreases in value by 4.5%

Bond 1: Face Value $1000. Maturity 5 Years, PMT/YR: 2; BOP: YTM: 5.0%; Coupon 10.0% Bond 2: Face Value $1000, Maturity 5 Years, PMT/YR: 2; BOP: YTM: 5.0%; Coupon 5.0% $2,000 $1,800 $1,600 $1,400 Bond Price (Y-Axis) vs. Yield to Maturity (X-Axis) $1,437.87 $1,378.85 $1,32278 1,269.48 78 s1.269.48 $1,218.80 $1,170.60 s1,12475 $1,0111 $1,039.56 $1,00o.00 $1,142.07 $1,092.22 $1,044.91 $1,000.00 $957.35 $916.83 $878.34 $84175 $806.96 $1.1 $1,200 $ $1,000 $800 $600 $400 $200 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% BOND 1BOND 2Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Computational Techniques In Economics And Finance

Authors: Constantin Zopounidis

1st Edition

1613245580, 978-1613245583