Answered step by step

Verified Expert Solution

Question

1 Approved Answer

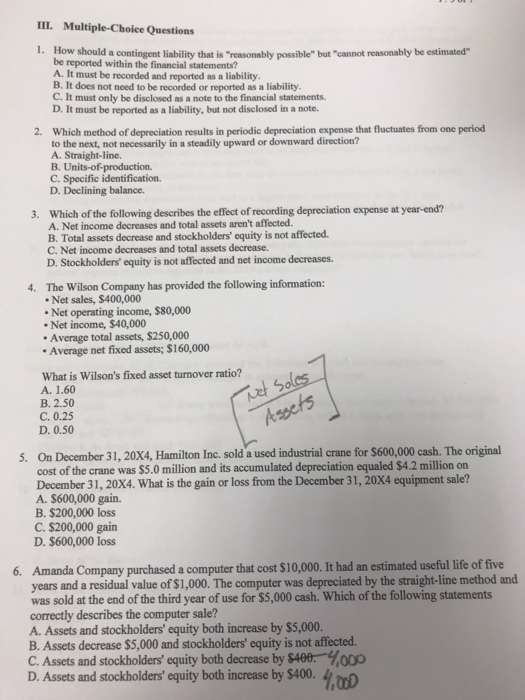

III. Multiple-Choice Questions 1. How should a contingent liability that is reasonably possible but cannot reasonably be estimated be reported within the financial statements? A.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Eco Management And Auditing A Practical Guide To EC Regulations

Authors: Joseph Tanega

1st Edition

1859070094, 978-1859070093