Answered step by step

Verified Expert Solution

Question

1 Approved Answer

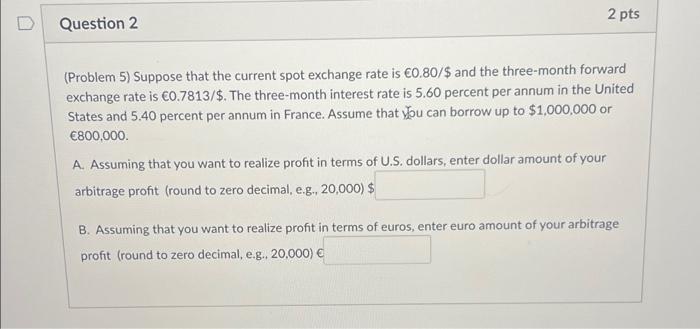

ill leave a like! D 2 pts Question 2 (Problem 5) Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange

ill leave a like!

D 2 pts Question 2 (Problem 5) Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is 5.60 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or 800,000 A. Assuming that you want to realize profit in terms of U.S. dollars, enter dollar amount of your arbitrage profit (round to zero decimal, e.g., 20,000) $ B. Assuming that you want to realize profit in terms of euros, enter euro amount of your arbitrage profit (round to zero decimal, e.g. 20,000) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The 3 Signal The Investing Technique That Will Change Your Life

Authors: Jason Kelly

1st Edition

0142180955, 978-0142180952