Answered step by step

Verified Expert Solution

Question

1 Approved Answer

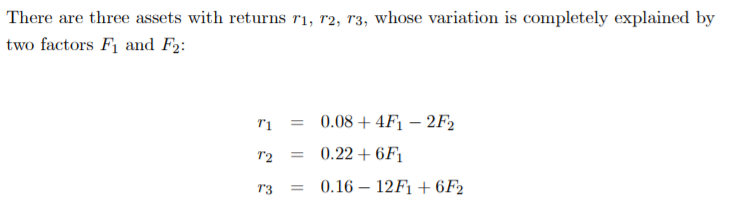

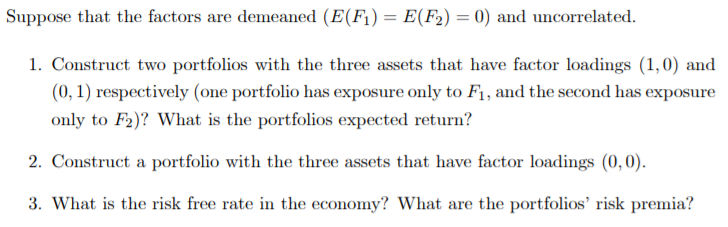

I'm confused on this problem There are three meets with returns 1'1, 1'2, 1'3, Whom variation is completely explained by two factors F1 and F3:

I'm confused on this problem

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Lectures On Urban Economics

Authors: Jan K Brueckner

1st Edition

0262300311, 9780262300315