Question

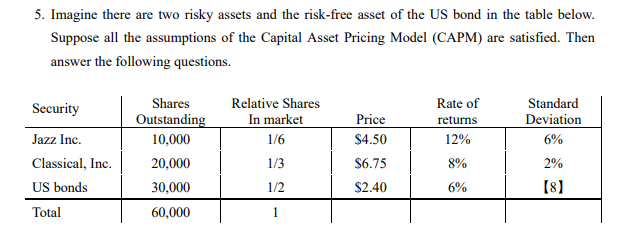

Imagine there are two risky assets and the risk-free asset of the US bond in the table below. Suppose all the assumptions of the Capital

Imagine there are two risky assets and the risk-free asset of the US bond in the table below. Suppose all the assumptions of the Capital Asset Pricing Model (CAPM) are satisfied. Then answer the following questions

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options On Futures Workbook Step By Step Exercises And Tests To Help You Master Options On Futures New Trading Strategies

Authors: John F. Summa ,Jonathan W. Lubow

1st Edition

0471436437, 978-0471436430