Question

In 2017, you purchased a 5-year 100 bp semi-annual coupon bond from AvalonBay Communities Inc at 101.4463 (YTM = 35.742 bp). At that time, you

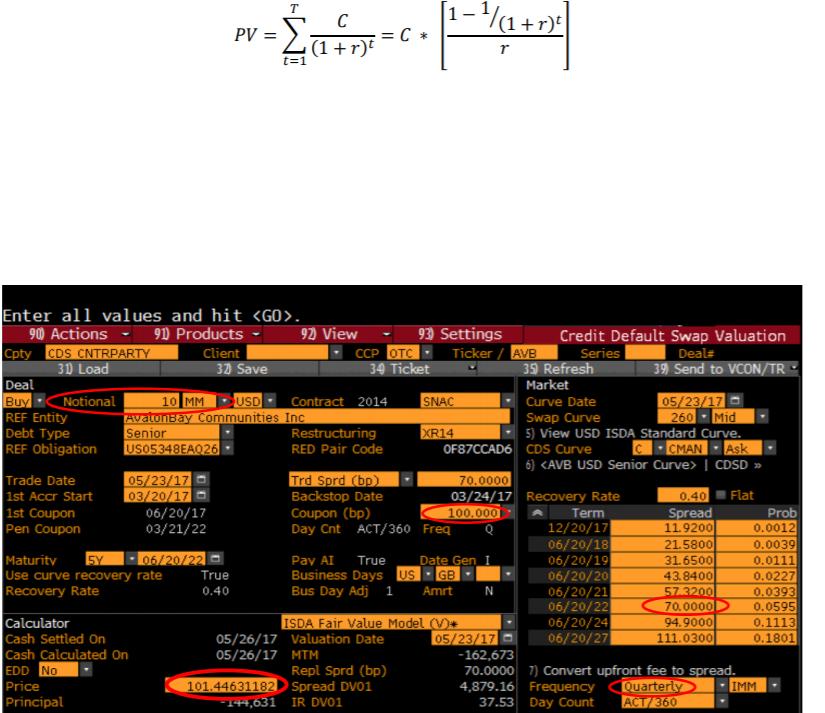

In 2017, you purchased a 5-year 100 bp semi-annual coupon bond from AvalonBay Communities Inc at 101.4463 (YTM = 35.742 bp). At that time, you also purchased CDS on the bond whose premium was 70 bp (APR) of the bond’s principal (quarterly settlement, annuity due). Calculate the market value of default risk on AvalonBay’s bond when you purchased the CDS. It is the amount of money the market is willing to pay to remove any default risk. (Assume that there is no default in your calculation. Use the YTM as your discount rate. You may use the following annuity formula)

[1-1+r)* C PV = C * (1 +r)* t=1 Enter all values and hit . 90 Actions - 90 Products - 92) View Cpty CDS CNTRPARTY 30 Load Client 32 Save 34 Ticket 93 Settings Ticker / AVB Series 39 Refresh Market Credit Default Swap Valuation Deals 39 Send to VCON/TR Deal Buy Notional REF Entity Debt Type REF Obligation 05/23/17 260 Mid 5) View USD ISDA Standard Curve. 10 MM USD Contract 2014 SNAC Curve Date AvatonBay Communities Inc Senior US05348EAQ26 Swap Curve XR14 Restructuring RED Pair Code 1CMAN Ask 6) | CDSD OF87CCAD6 CDS Curve Trade Date Trd Sprd (bp) Backstop Date 05/23/17 03/20/17 06/20/17 03/21/22 70.0000 03/24/17 Recovery Rate 100.000 0.40 Flat Spread 11.9200 21.5800 31.6500 43.8400 57.3200 70.0000 1st Accr Start 1st Coupon Pen Coupon Coupon (bp) Day Cnt ACT/360 Freq Term 12/20/17 Prob 0.0012 0.0039 0.0111 0.0227 0.0393 0.0595 0.1113 0.1801 06/20/18 Maturity Use curve recovery rate Recovery Rate 06/20/22 - True SY Date Gen Pav AI Business Days us - GB Bus Day Adj 1 True 06/20/19 06/20/20 06/20/21 06/20/22 06/20/24 06/20/27 0.40 Amrt N Calculator ISDA Fair Value Model (V)+ 94.9000 Cash Settled On Cash Calculated On EDD No Price Principal 05/23/17 -162,673 70.0000 7) Convert upfront fee to spread. 05/26/17 Valuation Date 05/26/17 MTM 111.0300 Repl Sprd (bp) 101.44631182 Spread DV01 4,631 Quarterly ACT/360 IMM 4,879.16 Frequency 37.53 Day Count IR DV01

Step by Step Solution

3.47 Rating (167 Votes )

There are 3 Steps involved in it

Step: 1

Solution The market value of default ris...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance A Focused Approach

Authors: Michael C. Ehrhardt, Eugene F. Brigham

4th Edition

1439078084, 978-1439078082