Answered step by step

Verified Expert Solution

Question

1 Approved Answer

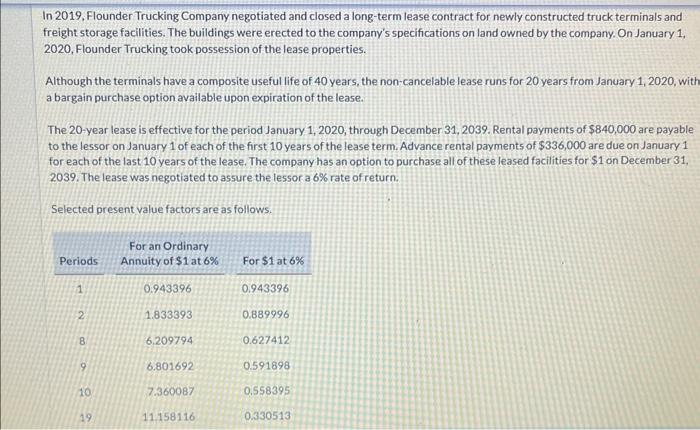

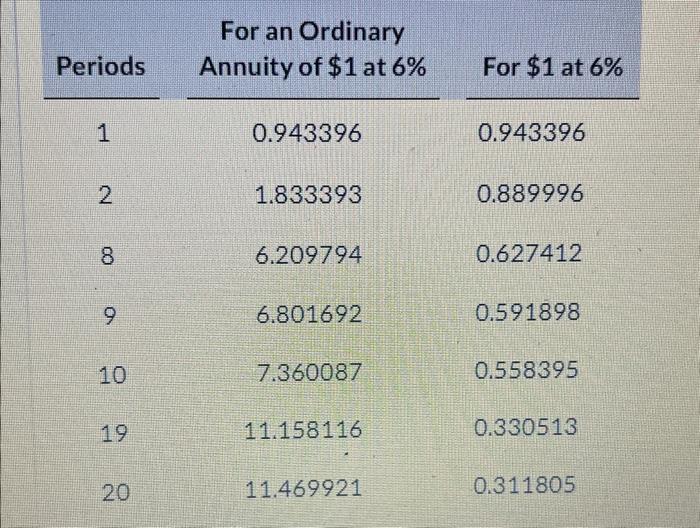

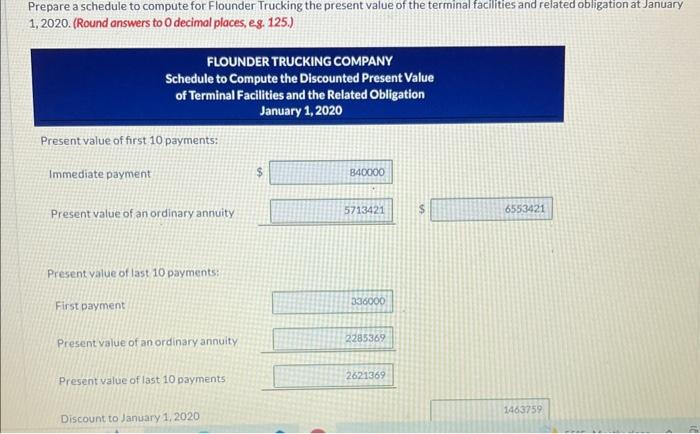

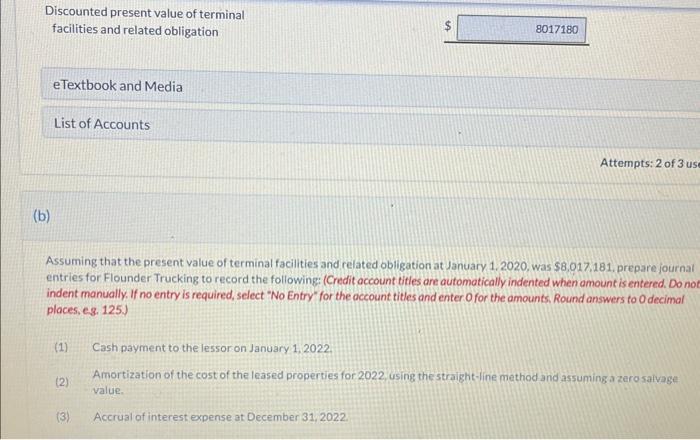

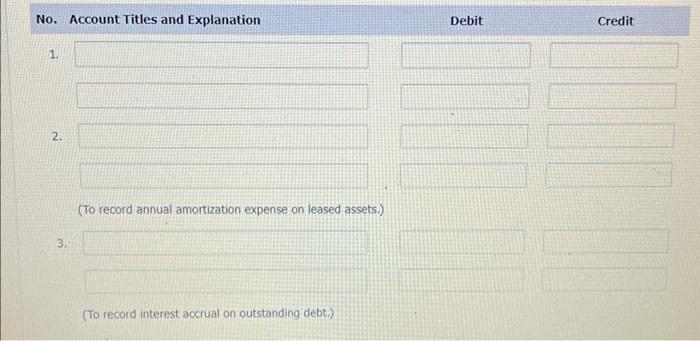

In 2019, Flounder Trucking Company negotiated and closed a long-term lease contract for newly constructed truck terminals and freight storage facilities. The buildings were erected

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Facilities Managers Reference Management Planning Building Audits Estimating

Authors: Harvey H. Kaiser

1st Edition

0876291426, 978-0876291429