Answered step by step

Verified Expert Solution

Question

1 Approved Answer

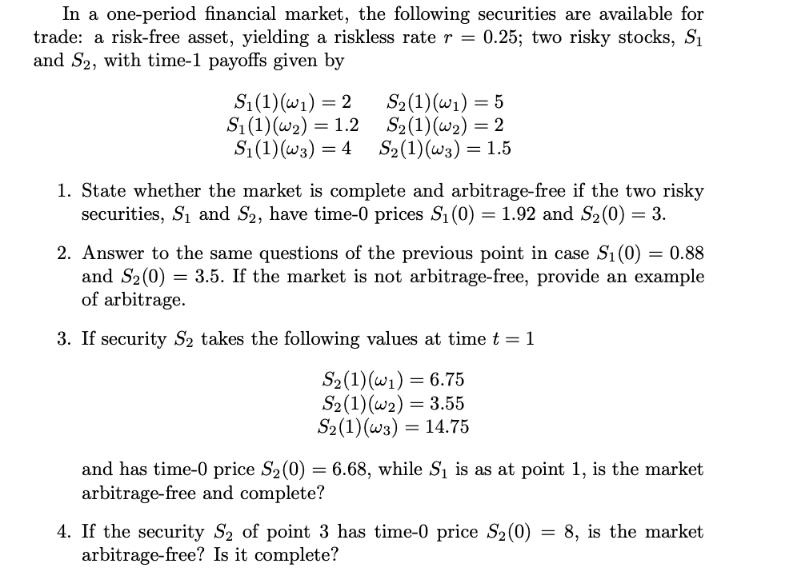

In a one-period financial market, the following securities are available for trade: a risk-free asset, yielding a riskless rate r = 0.25; two risky

In a one-period financial market, the following securities are available for trade: a risk-free asset, yielding a riskless rate r = 0.25; two risky stocks, S and S2, with time-1 payoffs given by S(1)(w) = 2 S (1) (w) 1.2 S (1) (W3) = 4 = S (1) (w1) = 5 S (1) () = 2 S(1)(W3) = 1.5 1. State whether the market is complete and arbitrage-free if the two risky securities, S and S2, have time-0 prices S (0) = 1.92 and S (0) = 3. 2. Answer to the same questions of the previous point in case S (0) = 0.88 and S (0) 3.5. If the market is not arbitrage-free, provide an example of arbitrage. 3. If security S takes the following values at time t = 1 S2 (1)(w1) = 6.75 S2 (1) (w2) 3.55 S2(1)(w3) 14.75 = = and has time-0 price S (0) = 6.68, while S is as at point 1, is the market arbitrage-free and complete? 4. If the security S of point 3 has time-0 price S (0) = 8, is the market arbitrage-free? Is it complete?

Step by Step Solution

★★★★★

3.43 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER 1 The market is complete and arbitragefree Given the payoffs of S1 and S2 under w1 w2 w3 as w...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516